The Upply x Ti x IRU European road freight rates index shows that the Q4 spot rate index was down 14.8 points year over year. However, the quarter-over-quarter fall in the contractual rates index was limited to 0.9 points, due to high costs and, in particular, the toll increases in Q4 2023.

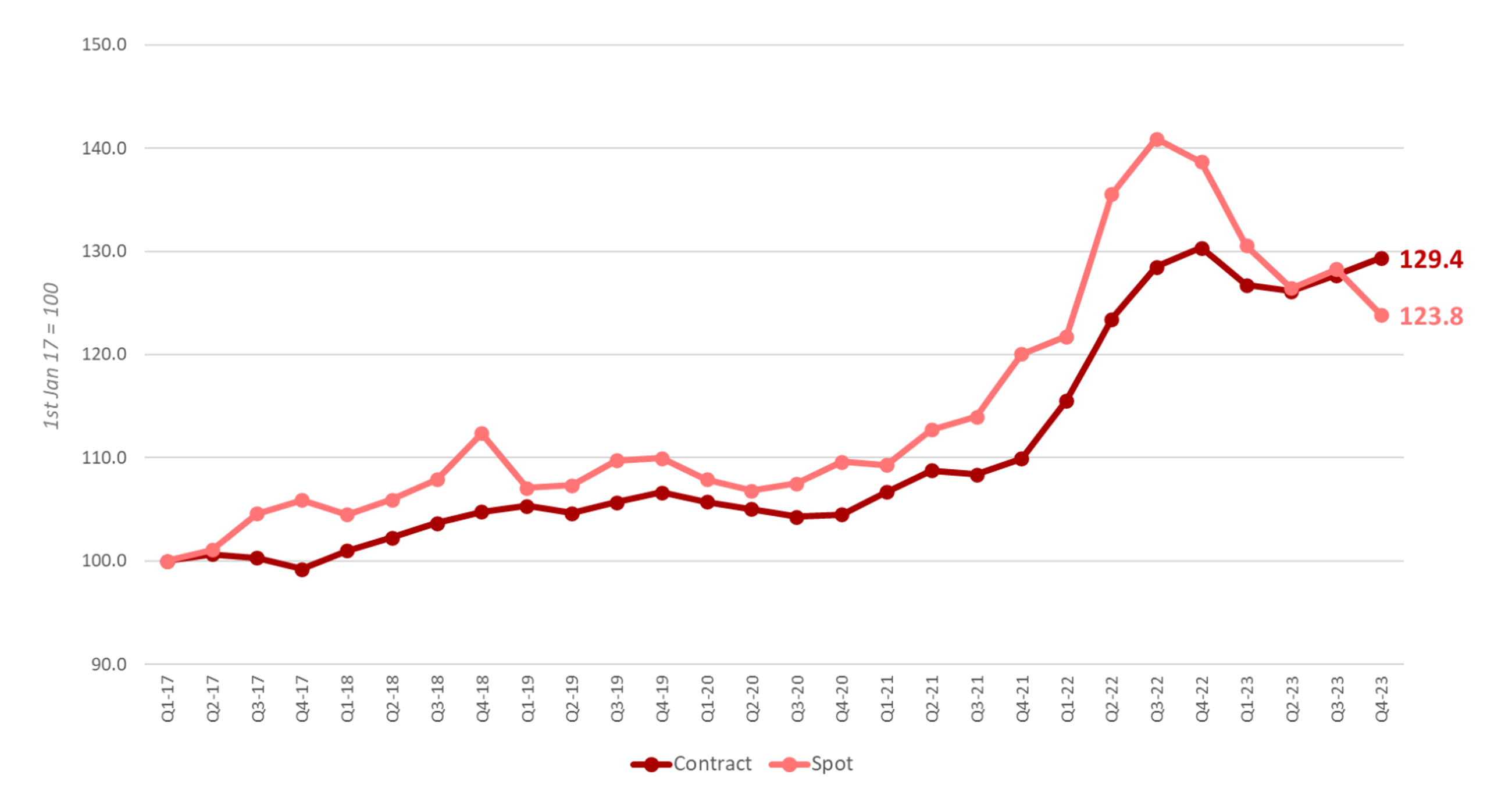

The spot index fell 4.5 points quarter over quarter (Q-o-Q) to 123.8 points. It is now down 14.8 points year over year (Y-o-Y). The contract index rose for the second consecutive quarter, up 1.7 points Q-o-Q to 129.4. The Y-o-Y fall was just 0.9 points.

- The Q4 2023 European Road Freight Spot Rate Benchmark Index stood at 123.8, 4.5 points lower than in Q3 2023 and 14.8 points down Y-o-Y.

- The Q4 2023 European Road Freight Contract Rate Benchmark Index stood at 129.4, 1.7 points higher than in Q3 2023 and 0.9 points lower than in Q4 2022.

- Toll price increases in Germany last December helped drive an 8.3-point increase in the German domestic rates index.

- In Germany, IRU estimates that the additional cost of tolls will be EUR 6,700 per truck per year, whereas the cost of the new tolls introduced will be EUR 730 per truck per year in Austria.

- Low demand is likely to keep freight rates subdued in 2024. However, the new tolls being introduced on top of the high cost base will keep upward pressure on rates in the first half of the year. This is likely to sustain contract rates and limit further falls in spot rate growth.

Weak and falling demand for road freight across Europe has pulled down spot rates, while contract rates remained elevated due to cost pressure. The spot index now sits 5.5 points below the contract index, meaning that spot rates are now closer to their base level than contract rates. A combination of spot falls driven by declining industrial demand, in addition to contract rises caused by new emission tolls and general cost growth, resulted in contract prices climbing above spot rates from German cities to Paris, Birmingham, Milan, Lille, Madrid, Rotterdam, and Antwerp.

Since rates spiked in the first half of 2022, plummeting consumption triggered by soaring prices has been the primary catalyst for consistent spot rate falls. However, in a new climate of diminished inflation, consumption has now settled at lower levels, resulting in lower road freight volumes.

Thomas Larrieu, Upply’s Chief Executive Officer, comments: “At the start of 2024, shippers now have access to spot rates that are lower than contractual rates. This year, road transport operators will have to cope with a fall in European demand, which has already been underway for several months, and with the unpredictability of their costs. Now is the time to accelerate the adoption of digital tools, which provide visibility and enable revenue optimisation.”

Costs have increased across the board over the previous three years. Labour (+28.2%), maintenance and repair (+20.4%), tyres (+21.6%), spare parts (+13.5%), and insurance (+8.7%) have all increased considerably and contributed to a particularly bloated cost base. This is the result of inflation passing through the system, adding upward pressure to rates and preventing rate falls.

Germany’s new emission-based tolls came into effect on 1 December 2023, effectively increasing tolls for heavy-goods vehicles on German roads by around 80%. According to GVN, the Lower Saxony Carrier Association, this increase will result in an additional EUR 300,000 monthly expense for some of its members. This is measurable in Germany’s domestic road freight rate index, which showed that rates were up by 8.3 points in December.

IRU estimates that the new tolls introduce an additional EUR 6,700 annual cost per truck in Germany. This assumes that German trucks perform 60% of national road freight operations on a tolled road network, knowing that 55% of freight volumes are transported by articulated vehicles with more than five axles and compliant with EURO VI standards, and that these vehicles represent 30% of the German fleet. Whereas the new tolls in Austria, introduced on 1 January 2024, are set to increase annual costs per truck by EUR 730.

Vincent Erard, IRU’s Senior Director for Strategy and Development, adds: “The European road transport sector is facing falling industrial demand, which is pulling down spot rates. But contract rates remain high due to cost pressure driven by new CO2 toll taxes and general cost increases. Transport companies are adapting to operational, financial and environmental challenges to meet future transport demand. Their efforts need to be backed by financial support for the green transition, the deployment of charging and refuelling infrastructure, more safe and secure parking areas, improved working conditions for drivers, and a comprehensive digitalisation of transport documents. We can also expect growing demand for drivers in the coming years, with an estimated 745,000 unfilled truck driver positions by 2028, and thus potentially higher driver costs. The indispensable contribution of the road transport industry to the entire economy and society should not be underestimated.”

Michael Clover, Ti’s Head of Commercial Development, says: “Road freight cost pressure just keep on coming as fuel and labour cost increases are now added to new tolls coming into force across Europe. As the data for Germany shows, we can expect these new tolls to lead to real increases in transactional road freight rates as they are implemented in different countries over the course of 2024, setting a new price baseline.”

Industrial output contraction and falling new orders look set to take over the deflationary mantle from a now-settled consumer demand. This is likely to produce further rate falls, especially in the spot market. However, the extension of the new emissions-based toll system to other European countries is set to further inflate an already elevated road freight cost base. This could put upward pressure on contract rates while limiting price falls and squeezing margins in the spot market.