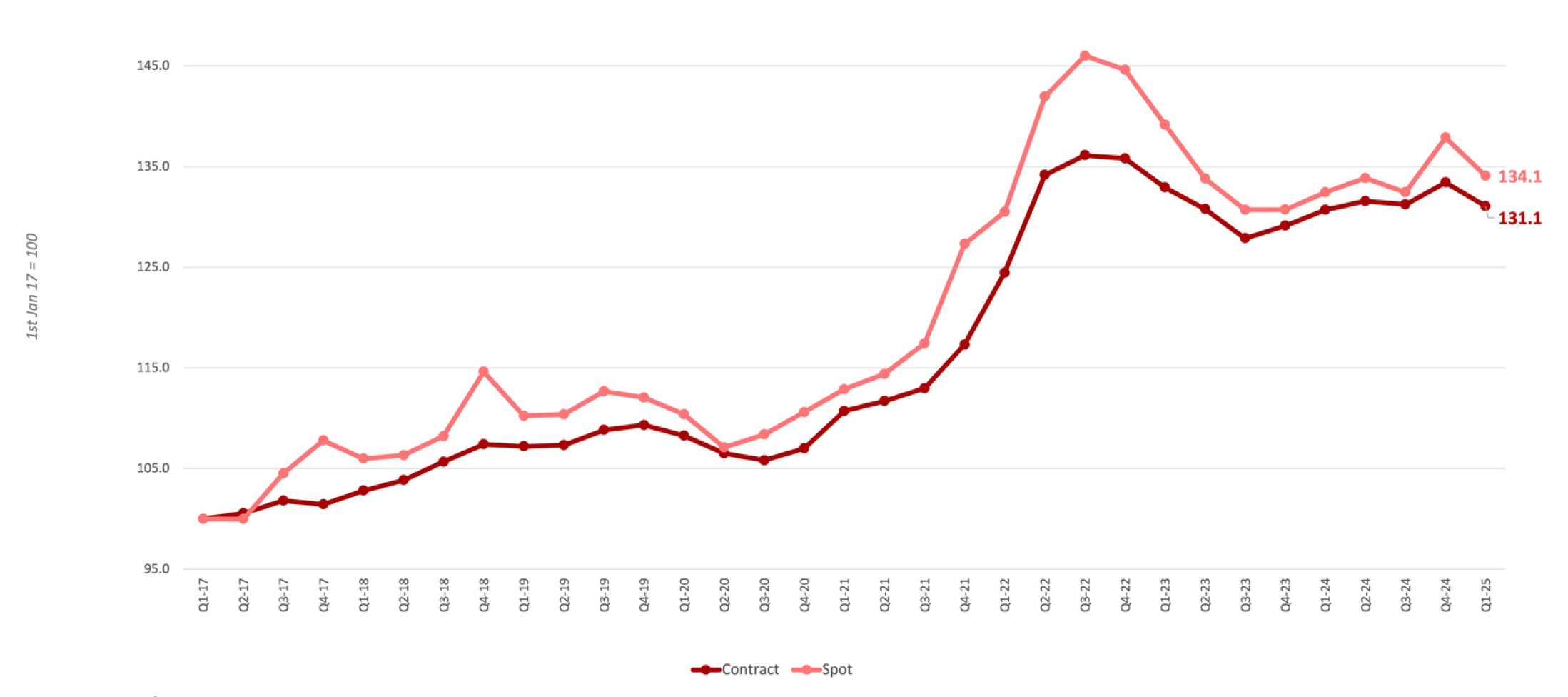

The Upply x Ti x IRU European road freight rates index shows that Q1 2025 contract rates fell by 2.3 points quarter on quarter (q-o-q). Spot rates declined more sharply, 3.8 points q-o-q. However, the spot index was up by 1.6 points, and the contract index rose by 0.4 points, year on year (y-o-y).

- The Q1 2025 European Road Freight Contract Rate Benchmark Index fell to 131.1, 2.3 points lower than in Q4 2024 but 0.4 points higher than in Q1 2024.

- The Q1 2025 European Road Freight Spot Rate Benchmark Index fell to 134.1 points, 3.8 points lower than in Q4 2024, but up 1.6 points y-o-y.

- According to IRU’s 2024 driver shortage survey, there are 426,000 unfilled truck driver positions across Europe.

- Q1 2025 diesel prices rose by 4.8% compared to Q4 2024, though prices have fallen in recent weeks.

- The outlook for rates across Europe has cooled, as demand weakens, fuel prices fall, and labour cost growth slows.

The end-of-year peak period has been followed by a return to low European demand. The start of 2025 has kept down freight rates as consumer demand remains subdued, costs have slowed their growth, and industry sentiment has been dampened as the world engages in a trade war, which brings constant uncertainty and reduced international demand for European manufacturers. The result is reduced demand pressure on all sides, leading to rate falls in both spot and contract markets.

Consumer spending in Europe has remained stagnant, increasing only 0.6% q-o-q, according to Eurostat, with 61% of households maintaining similar income, saving and spending levels compared to the previous quarter, according to a McKinsey consumer survey. A consistent number of consumers (74%) reported trading down, mainly by buying less or buying from cheaper retailers. Apparel topped the list of categories consumers were willing to spend on. At the start of 2025, spending patterns followed usual seasonal trends, slowing down after their peak in Q4, which put downward pressure on freight rates, particularly spot rates.

Geopolitical changes and global economic instability have renewed focus on strengthening local and regional economies. This has led to initiatives such as "Buy European", which encourages the support of European goods and businesses. As a result, there is potential for increased demand for dedicated contracts, with a preference for long-term agreements rather than fluctuating spot rates in the medium to long term.

Ti Head of Commercial Development Michael Clover said, “European demand was already quite weak and the uncertainty from tariffs has led many to expect lower road freight volumes. We do expect lower volumes to reduce pressure on road freight rates through 2025. And as cost growth has also slowed, we expect to see fairly stable rates for the rest of the year.”

New capacity entering the market has been constrained. Heavy goods vehicle registrations fell by 16% between Q1 2024 and Q1 2025, and by 7% q-o-q. Notably, battery-electric truck registrations grew by 51% y-o-y to reach a 3.5% market share. The driver shortage crisis persists, with 426,000 unfilled truck driver jobs in Europe, according to IRU’s 2024 global truck driver shortage report.

In terms of the underlying cost drivers, diesel prices have increased by 4.8% q-o-q, but have been decreasing lately as the trade situation brings uncertainty to businesses, slowing down global demand for oil.

The latest data on driver wages across Europe suggests that wages are still rising. For example, driver wages increased by 5.1% y-o-y for Spanish drivers conducting international operations, according to the Spanish Ministry of Transport. In Italy, new agreements have led to wage increases of more than EUR 500 per month since the beginning of 2025 to notably cover the time spent waiting at loading and unloading sites. These rises follow 4% y-o-y labour cost increases across the EU in Q4 2024.

IRU Senior Director of Strategy and Development Vincent Erard added, “Road transport stands at a critical inflection point – where resilience, sustainability and competitiveness must converge. Despite economic headwinds and global trade uncertainty, Europe’s transport sector has the potential to power a new cycle of regional growth. Policymakers and industry must now co-create the conditions that enable long-term investment, digital transformation and decarbonisation – especially for the SMEs that form the backbone of our supply chains.”

In the short term, the broader picture of a potential EU recovery is being held back by ongoing tariff uncertainties and policy disruptions, which continue to weigh on trade flows and the momentum of freight rates.

In the medium term, the outlook is more positive. Real GDP is projected to strengthen, driven by growth in consumption, improved investment, and recovering foreign demand. Economic activity in the euro area is expected to expand by 0.2% across the first three quarters of 2025. Household spending is forecast to have increased by 1.4% in March y-o-y, and annual private consumption growth is projected to improve from 0.9% in 2023–2024 to 1.3% over 2025–2027. These trends point to gradually improving demand conditions, which could support a rebound in freight volumes and rate stability in the medium term.

However, the uncertainty that tariffs create will have different consequences in the short term. Businesses will increasingly blend contracts for baseline capacity, using spot rates for flexibility. As a result, the uncertainty could dampen the impact of rising demand on the contract market and amplify pressure on the spot market.

Upply Chief Executive Officer Thomas Larrieu commented, “The European road transport market is once again going through a complex phase, as major uncertainties in global trade are likely to weaken the still fragile economic recovery. At the same time, this may also lead to an acceleration of nearshoring, which could stimulate demand for road transport. The current balance of power remains fairly favourable to shippers, but it is wise to secure long-term capacity based on balanced partnerships with carriers."