As of 20 March 2026, attacks on critical energy hubs have pushed global oil and fuel prices higher. Here is the latest overview for the road transport sector.

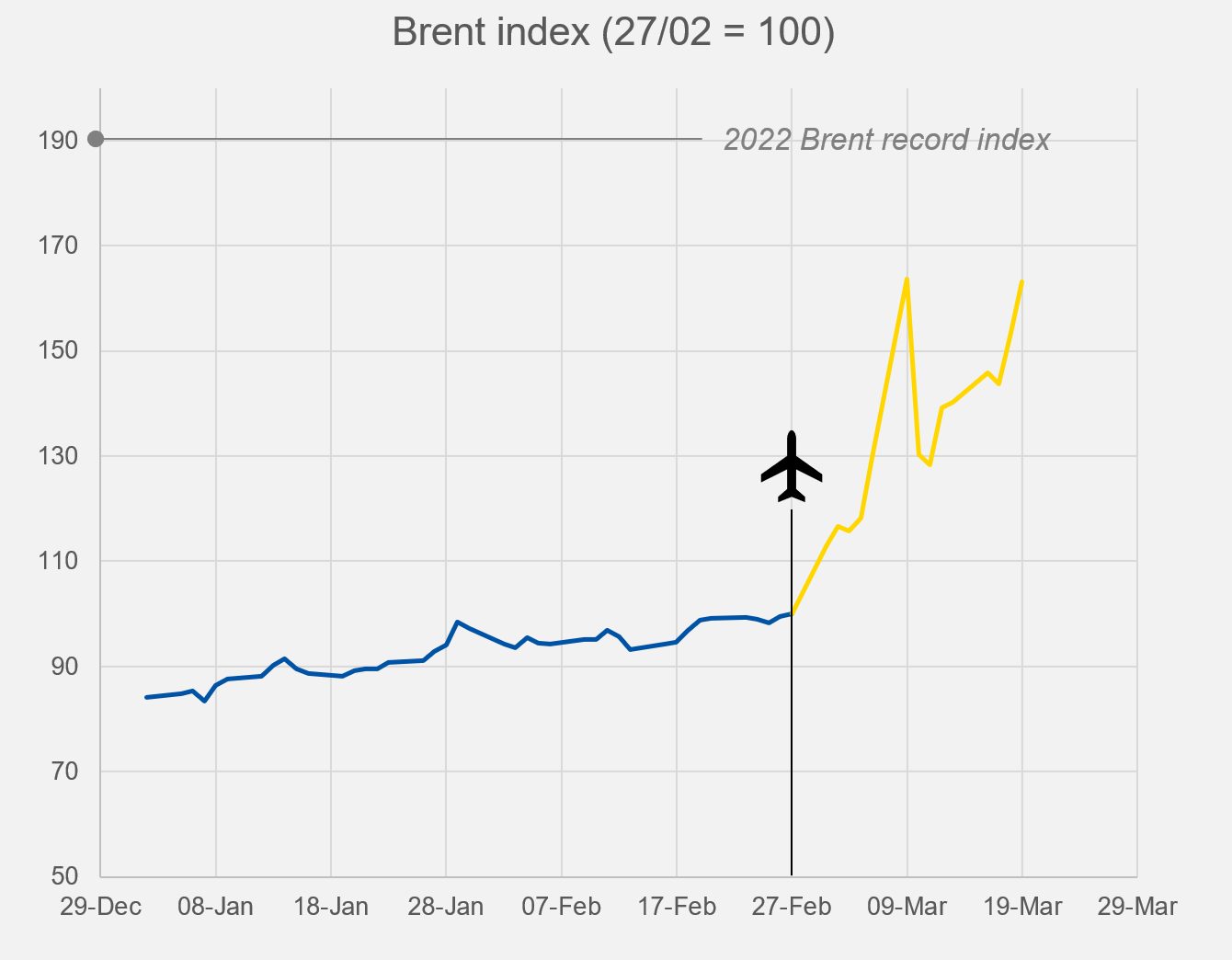

This week saw less volatility in Brent, which is nonetheless slowly reaching record highs, staying above USD 100 since Monday 16 March.

As a result, prices at the pump continue to increase everywhere, raising questions about supply for Asian countries. Governments are starting to take action, though impacts for operators remain limited.

Our weekly analysis first looks at average prices at the pump, before turning to wholesale energy dynamics, including Brent and LNG trends.

Pump prices

United States: The US has experienced the largest increase, with diesel prices rising by 33% since the beginning of the war. WTI, used as a reference for the region, is no longer aligned with Brent this week, but prices are similar to 2022 levels.

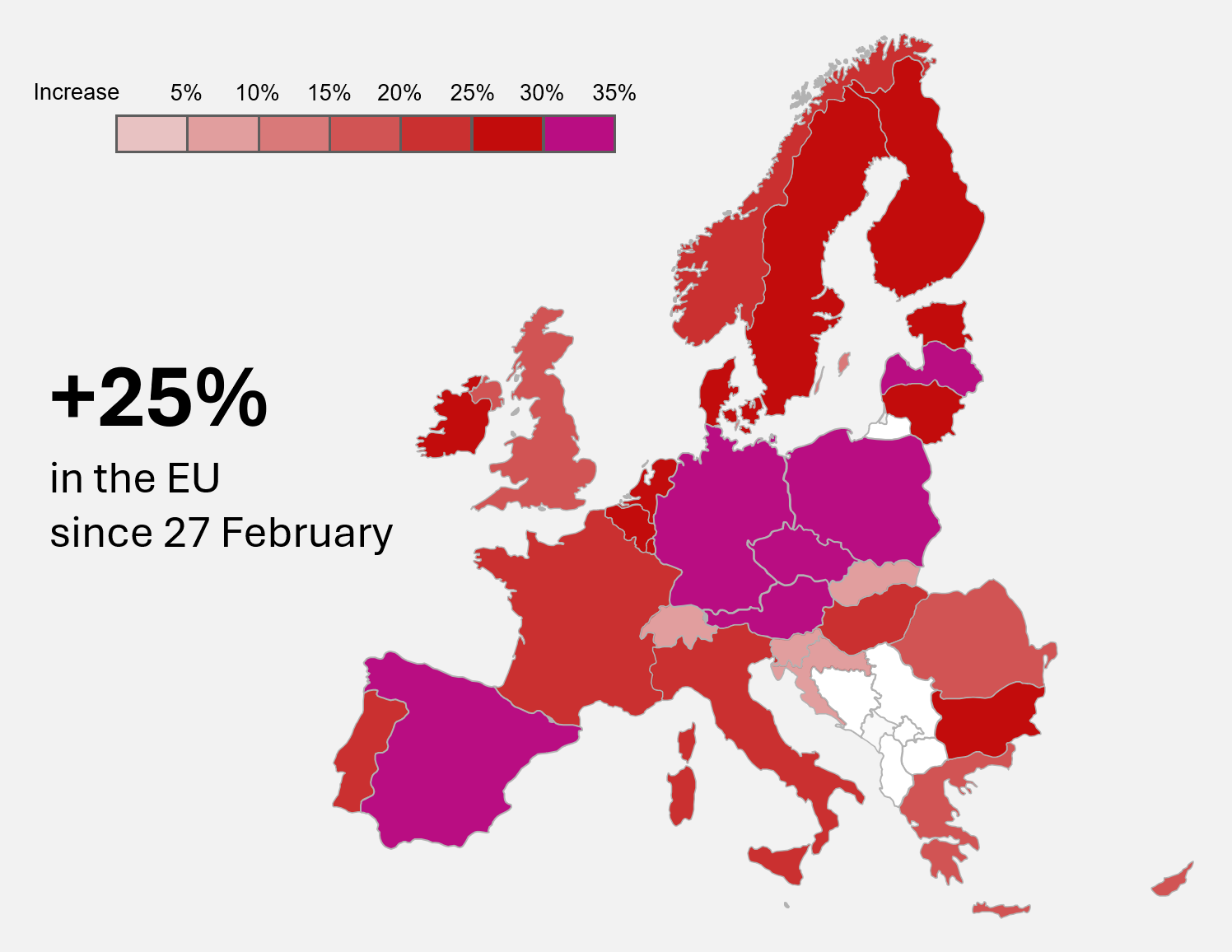

EU: The EU is seeing significant price hikes.

The weighted average (based on truck consumption) has surged by 25% since the war began, 5% more than the increase reported last week.

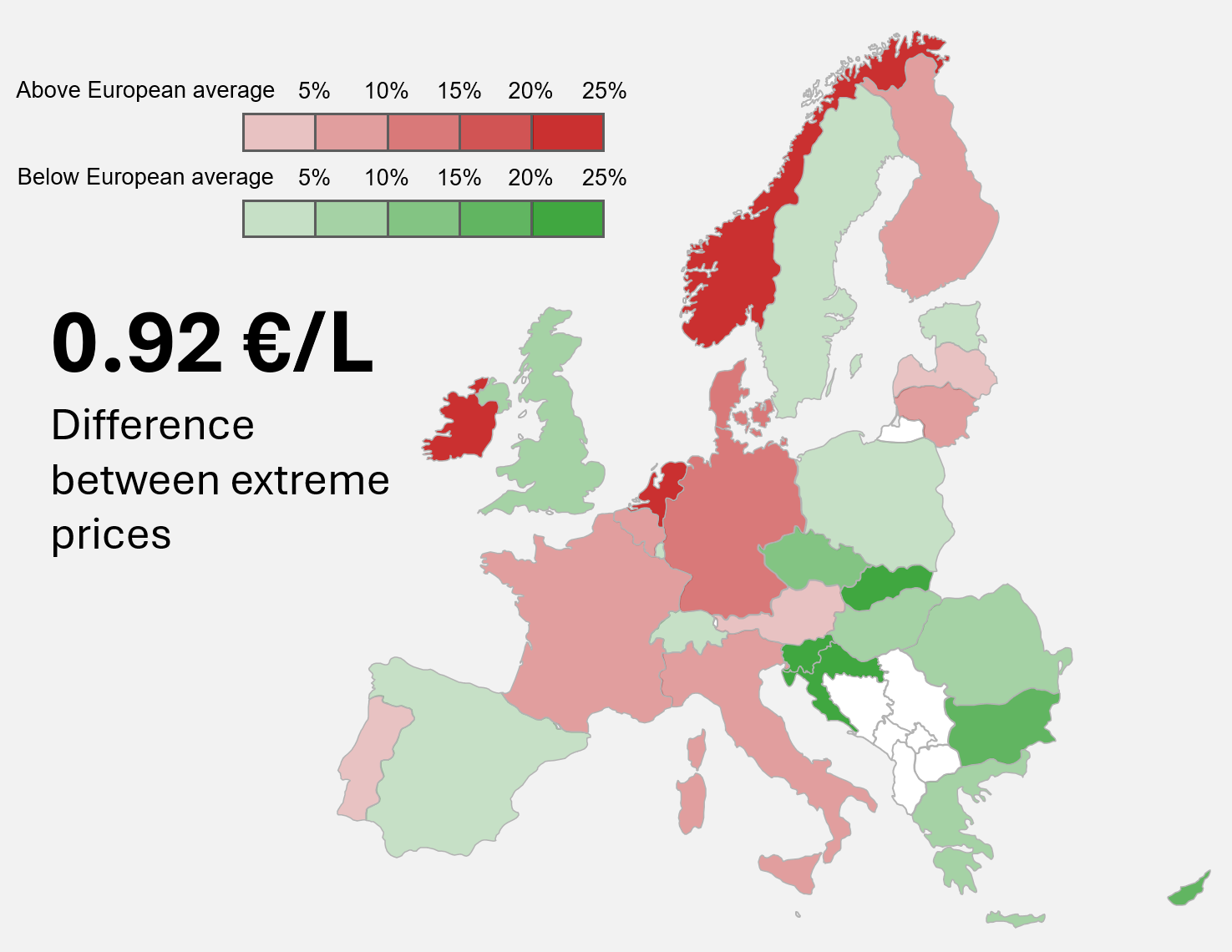

Diesel has reached EUR 2.1 per litre on average (taxes included), ranging from EUR 1.528 per litre in Slovenia up to EUR 2.452 per litre in Ireland.

The price of diesel has surged by 35% in Spain, the highest increase in the EU.

Nine countries have diesel prices above EUR 2 per litre: Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Lithuania, Luxembourg and the Netherlands. Price differences have led to fuel tourism, which has created queues and local shortages at borders, but no sustained shortage is currently foreseen.

Norway, Switzerland & UK: In the UK, diesel prices at the pump are up 17%, 4% more than last week.

In Switzerland, they increased by 12%.

In Norway, by 23%.

Brazil, China & India: Brazil saw diesel prices rise by 12% this week, bringing the total increase to 13% since the war began.

China and India prices are up by less, at 11% and 5% respectively, noting that both countries have more interventionist government price control polices permanently in place.

The EU, US and UK should be protected from any durable diesel shortages in the medium term, as they are less dependent on Middle East crude oil. However, China and India are more exposed.

China is actively trying to limit domestic pump price spikes:

- Authorities have asked major refineries to suspend diesel and gasoline exports to keep more fuel for the domestic market

- The government adjusts retail fuel prices in China based on international crude movements, rather than purely market pricing

This means that price increases at the pump happen gradually, rather than continuously like in Europe.

Brent

Brent has gone from roughly USD 73 a barrel on 27 February to USD 120 on 9 March and USD 119 on 19 March, an increase of around 65%. Brent has remained above USD 100 since Monday 16 March, slowly climbing as the war intensifies.

This week saw less volatility in Brent, but prices remain sensitive to developments in the conflict.

Some tankers have been able to cross the Strait of Hormuz, mainly bound for South Asia, while others have been attacked and heavily damaged.

Recent attacks on GCC crude oil and gas installations and Iranian military assets on Kharg Island have pushed Brent higher.

So far, the release of 400 million barrels from worldwide stockpiles (out of 1,800 million barrels available) has contained the rise, but it has not been enough to deliver a sustained price decline. Discussions are underway to establish military protection for tankers crossing the Strait of Hormuz, but implementation will be challenging, and questions remain over insurance premiums.

Even if the war ends relatively soon, a return to normality will take weeks, and questions remain about sites that have reduced output, as shutting down and restarting can jeopardise efficiency.

The risk of inflation will grow if the war continues for several months and Brent exceeds USD 150, putting the world in a situation close to the 1973 oil crisis, according to Nobel Prize winning economist Philippe Aghion. The European Central Bank anticipates inflation rising from 1.9% to 2.6% in 2026 for the eurozone, and from 2.0% to 2.7% in the US, according to the Federal Reserve.

Government actions

Some countries have already taken steps to reduce fuel consumption and limit cost increases.

In Pakistan, schools are closed and government offices operate four days a week. South Korea has announced it will cap pump prices for the first time in nearly 30 years.

Some European countries have implemented minor temporary measures to mitigate fuel prices, but overall EU coordination remains lacking.

Hungary, Italy and Slovenia, for example, have temporarily reduced excise duties.

Others, such as Croatia and Slovakia, have put temporary price controls or caps in place.

Portugal has reduced excise duty on diesel, but with no effect for operators as the partial excise refund was reduced accordingly.

Other governments have formed task forces to monitor the situation.

Italian authorities are planning to invest EUR 100 million to support operators in 2026.

Some countries, such as Austria, are discussing mitigation plans, but nothing has been officially signed yet.

In countries with a fuel price index for transport operators, such as France, authorities are trying to minimise publication delays to avoid cash flow losses for operators.

Natural gas

To date, CNG and LNG prices for trucks and buses in the EU have been less affected than diesel, despite higher natural gas prices.

However, high natural gas prices are jeopardising future road freight volumes, as European industries rely on it to power factories.

Moreover, AdBlue is made from natural gas, and its price has been climbing since the beginning of the conflict. AdBlue prices in Germany have risen by 17% since 27 February.

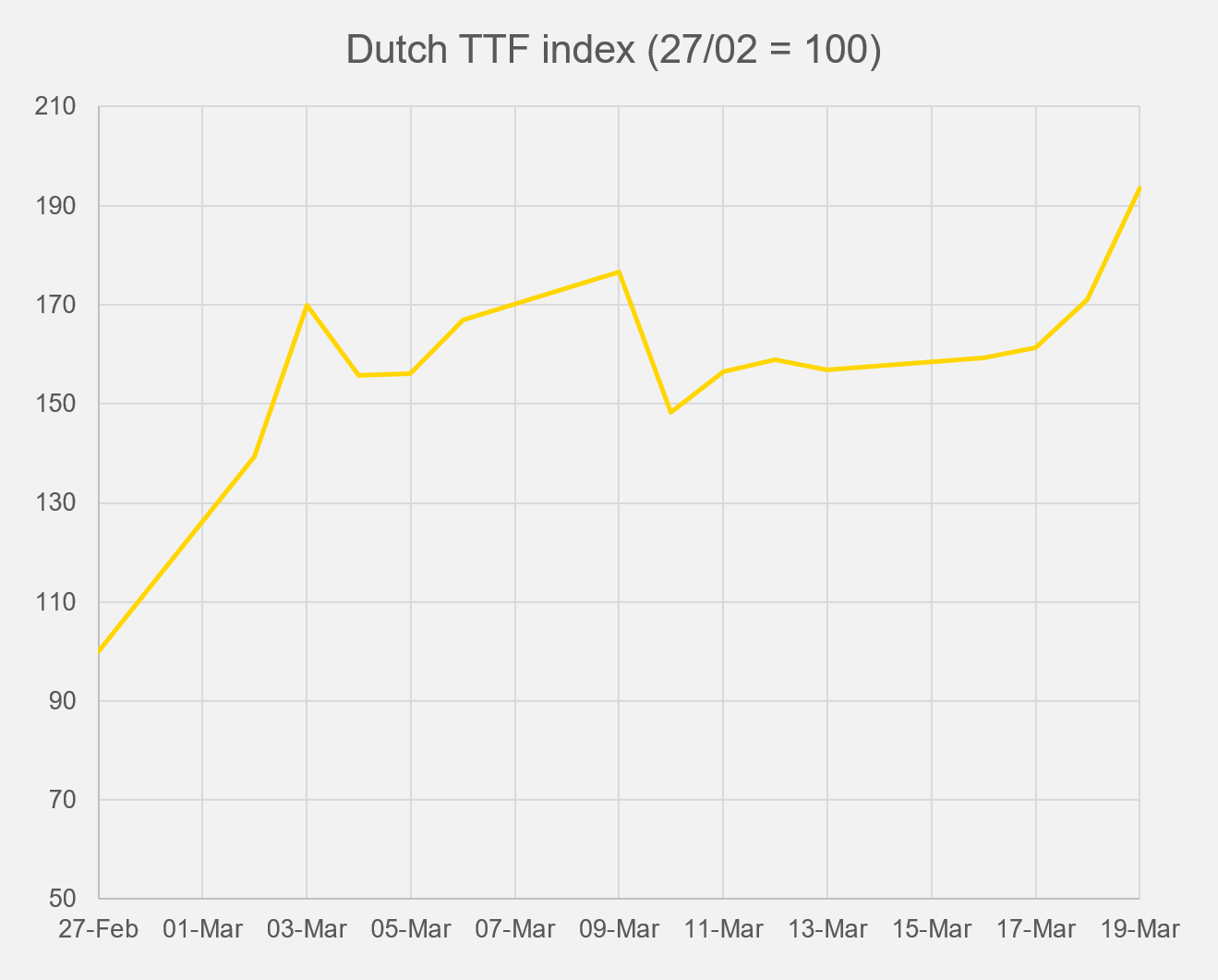

Dutch TTF gas prices, Europe’s benchmark gas hub, have been strongly affected, mainly due to LNG supply risks, shipping chokepoints, and storage dynamics.

This week, attacks on gas production sites in Qatar and Iran sent TTF prices soaring, exceeding EUR 60 per MWh for the first time since the beginning of 2023.

Stockpiles are lower than usual in the EU, averaging 29%.

The Netherlands stands at 7% (2% less than last week) and Germany at 22%, with both countries at their lowest levels on record.

A similar trend is seen in Spain, although stock levels are higher at 56%.

France is also below its usual level, though not at a record low, at 22%.

After winter, stockpiles will need to be replenished, potentially at higher prices, which could impact economic output and, in turn, freight activity.

Pakistan and India, which rely heavily on natural gas from the Middle East, have put restrictions in place, while seeking other supply sources.

Under the Natural Gas Supply Regulation Order 2026, issued under the Essential Commodities Act, India has introduced emergency rules to prioritise gas for households and other critical uses, while managing LNG shortfalls linked to Strait of Hormuz disruptions.

City gas distributors and industrial suppliers have also asked industrial and commercial users to limit consumption to around 40% of contracted volumes, with higher prices applied above that threshold, effectively rationing gas for energy-intensive industries.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.