As of 3 July 2026, crude relief has arrived before pump relief. Brent reached USD 72.49 a barrel on 3 July, putting it 0.7% below the 27 February baseline. But the EU weighted diesel average rose to EUR 1.766 per litre, 8.1% above the baseline, as Germany and Spain let key fuel-tax relief lapse on 30 June. US diesel is still USD 1.282 per litre, 25.5% above the baseline. Here is the latest overview for the road transport sector.

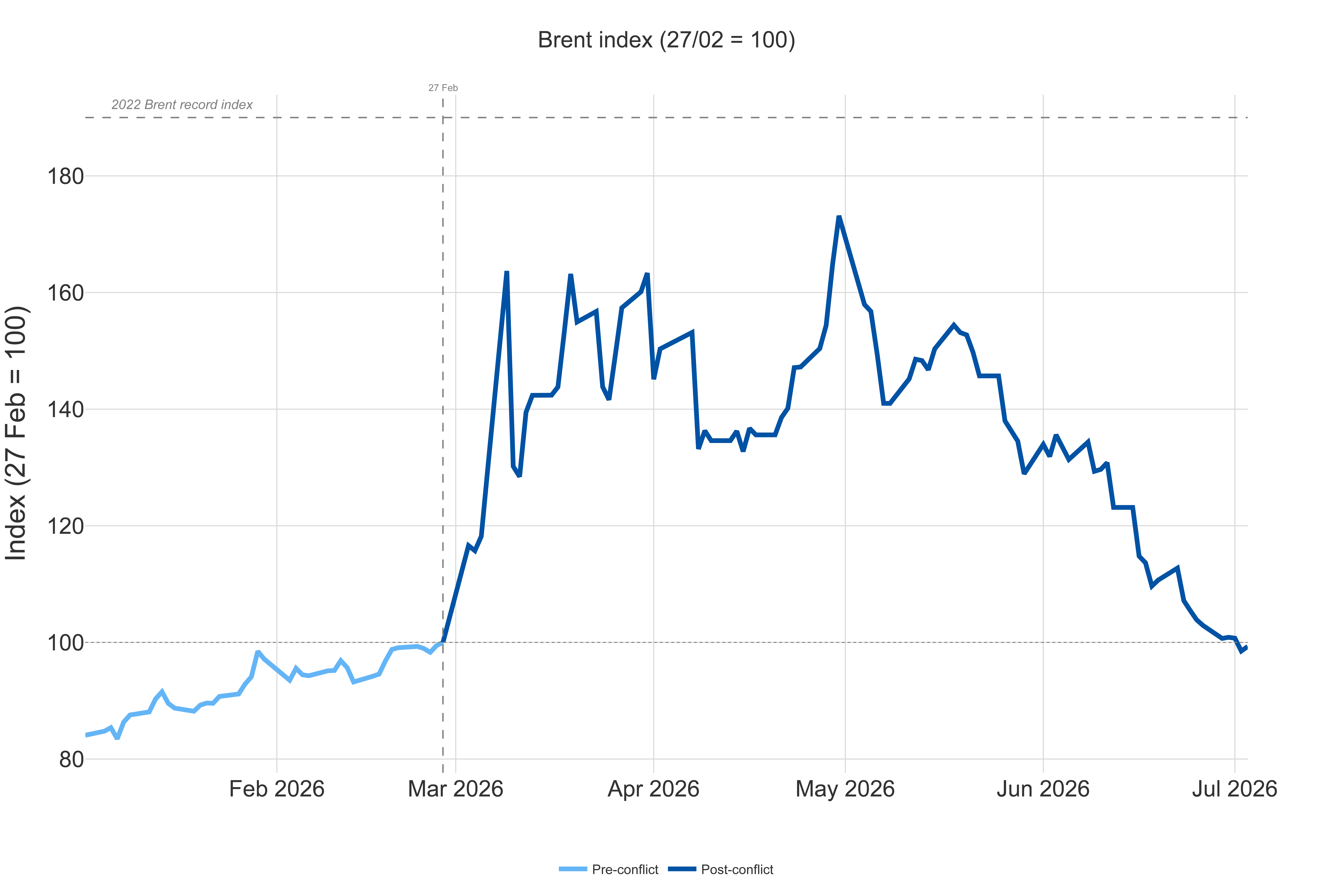

Brent is now below its pre-war level for the first time. It reached USD 72.49 a barrel on 3 July, down 3.5% on the week and below the USD 73.0 baseline of 27 February.

West Texas Intermediate (WTI) reached USD 69.11 a barrel, still 1.9% above its baseline, leaving a Brent-WTI spread of about USD 3.4.

The broader Goldman Sachs Commodity Index stands at 617.12, well below the spring peak.

The market is pricing the de-escalation more quickly than the physical system can repair itself. The 17 June US-Iran MoU and the 22 June US Treasury waiver have made Iranian crude and petroleum flows legally easier until 21 August. That is why the war premium has drained from Brent. Yet the International Energy Agency's (IEA) June balance still points to a damaged supply base, depleted inventories and a market that has not rebuilt its buffers.

Banks are now more relaxed than the physical indicators. Goldman Sachs and J.P. Morgan both see room for cheaper crude if the political track holds, while the IEA still sees lost supply and thin stocks through the summer. This gap between financial calm and physical fragility is the main crude story for operators. OPEC+ will review output again on 6 July; the bigger date is 21 August, when the US waiver expires.

The weekly path shows how quickly sentiment has changed. Brent moved from USD 75.84 a barrel on 25 June to USD 75.13 on 26 June, USD 73.50 on 29 June and USD 73.53 on 1 July, before breaking below baseline at USD 71.92 on 2 July. The rebound to USD 72.49 on 3 July did not change the message: the benchmark is now trading in the post-deal range rather than the war-premium range.

That does not mean the risk has disappeared. The technical talks, the status of the Persian Gulf shipping corridor and the 21 August waiver expiry still matter for fuel buyers. A smooth extension would make the lower crude price more durable. A snap-back would rebuild the premium quickly, especially while inventories remain thin and the physical supply chain is still repairing damage from the spring disruption.

Prices at pumps

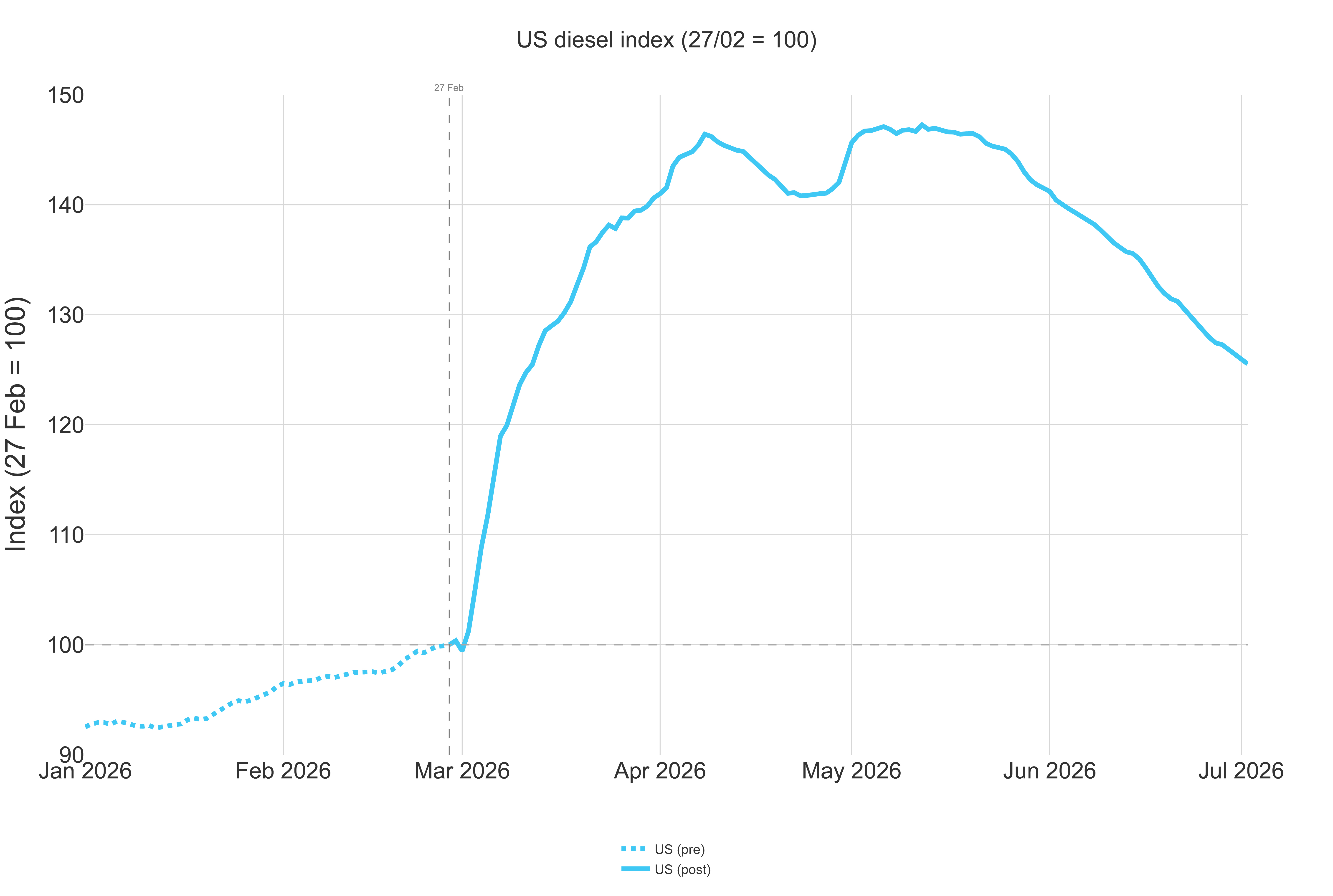

In the US, diesel stands at USD 1.282 per litre, 25.5% above the 27 February baseline. WTI has almost round-tripped to pre-war levels, but diesel has not. Refining losses, distillate margins and inventory rebuilding mean pump prices are lagging crude on the way down. Operators should therefore expect relief to arrive gradually rather than as a single weekly reset.

The US reading is important because there are few tax shields. It shows the market pass-through more directly: crude can normalise while diesel remains elevated because the product market is still tight. The same lag is visible in Europe, but there it is now mixed with a policy shock from expiring relief measures.

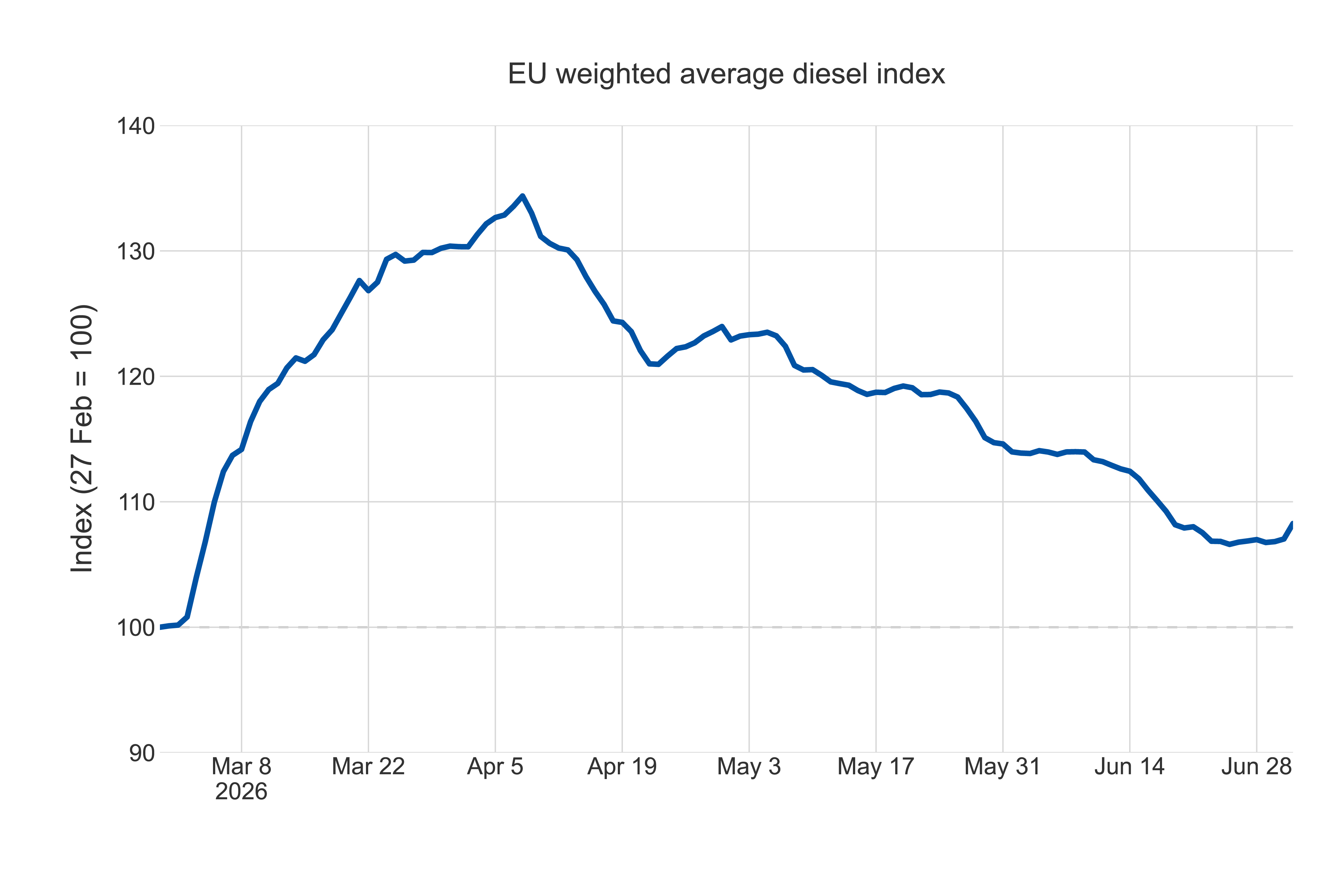

The EU is moving in the opposite direction. Diesel averages EUR 1.766 per litre, 8.1% above the baseline and 1.4% higher than last week, even as Brent fell 3.5%. The spread between the cheapest and most expensive EU markets remains EUR 0.90 per litre, keeping tank-location planning commercially relevant.

This is the main July change for EU operators. The data no longer describe a simple crude-to-pump easing story. They describe a timing mismatch: upstream costs are falling, but fiscal support is being withdrawn before the product market has fully normalised. That is why the EU average rose at the same time as Brent moved below its baseline.

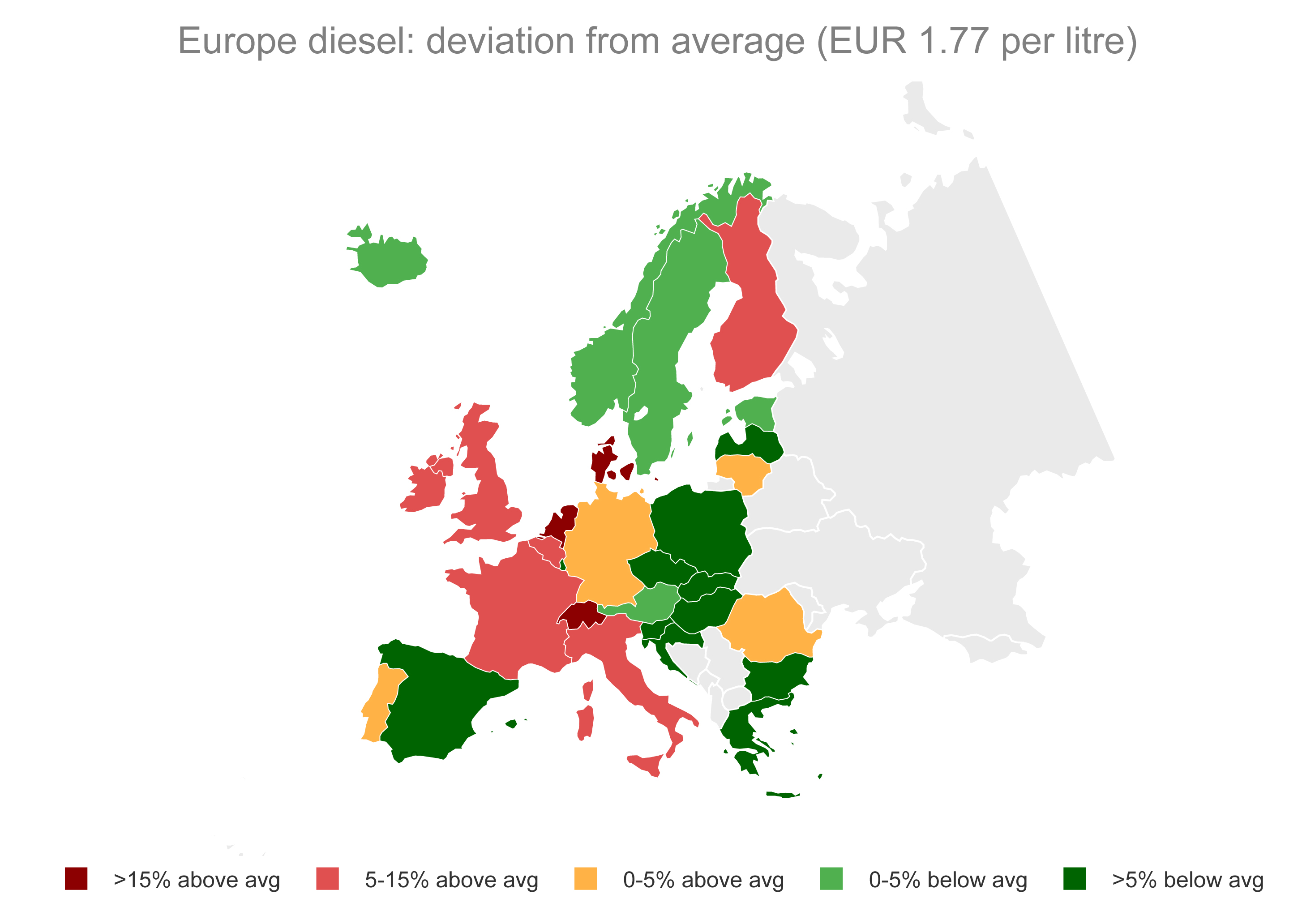

Diesel is most expensive in the Netherlands at EUR 2.114 per litre, Denmark at EUR 2.038, Finland at EUR 1.968, Belgium at EUR 1.894 and France at EUR 1.892. Finland has had the sharpest increase among the five highest-price markets, up 12.3% since the baseline, while Spain is still comparatively low but now exposed to the end of its relief package.

The lowest prices are in Malta at EUR 1.210, Czechia at EUR 1.461 and Spain at EUR 1.532.

In the UK, diesel costs GBP 1.65 per litre, 17% above the baseline.

In China, it stands at CNY 7.61 per litre, up 16%; India at INR 98.13, up 8%; Türkiye at TRY 66.14, up 7%; Brazil at BRL 6.75, up 12%; and Mexico at MXN 26.95, up 3%. These markets have eased from the spring peak but remain materially above pre-war levels, with local tax, currency and subsidy systems deciding how quickly cheaper crude reaches operators.

The local-currency reading matters here. China and Türkiye still show sizeable rises even after crude relief because domestic pricing formulas and currency moves blunt the headline Brent signal. India remains more insulated, while Brazil continues to rely on support measures and refinery pricing. For international operators, the pump-price map is therefore more useful than the crude chart when planning cash flow and fuel clauses.

National measures

For operators, the immediate risk has shifted from crude to the policy calendar.

Germany's EUR 0.14 per litre energy-tax cut expired on 30 June. Spain's diesel VAT reduction and EUR 0.20 per litre professional fuel card lapsed the same day. Italy's excise cut had already ended on 6 June, with the country pivoting to a diesel tax credit for operators.

The expiry cluster matters because it can erase crude relief at the pump. Where relief has ended, operators face a step-up of roughly EUR 0.14-0.20 per litre before any slower market pass-through is visible. That is why the EU weighted average rose this week even as Brent fell. The effect will be most visible on cross-border routes where operators can choose between high-price and low-price refuelling locations.

There are exceptions. Sweden added relief through an SEK 0.82 per litre energy-tax cut running to 30 September and a SEK 2.40 per litre CO2-tax cut from 1 July to 30 November. Norway has held road-use excise at zero since 1 April and added a NOK 1.33 per litre diesel cut from 1 May, with normal rates due back on 1 September. The Netherlands has extended its reduced excise to 1 January 2027 but has not deepened support, while Belgium and Finland have announced no new relief despite high pump prices.

The practical result is a wider planning gap between markets. Fleets with flexible refuelling can still use Czechia, Spain and other lower-price points to reduce exposure, but Spain's advantage should narrow as the 30 June expiry is reflected at forecourts. Fuel surcharge clauses also need close weekly monitoring: crude-linked formulas may understate the actual cost where tax relief has ended, while fixed-rate contracts may overstate relief where prices are still sticky.

Natural gas

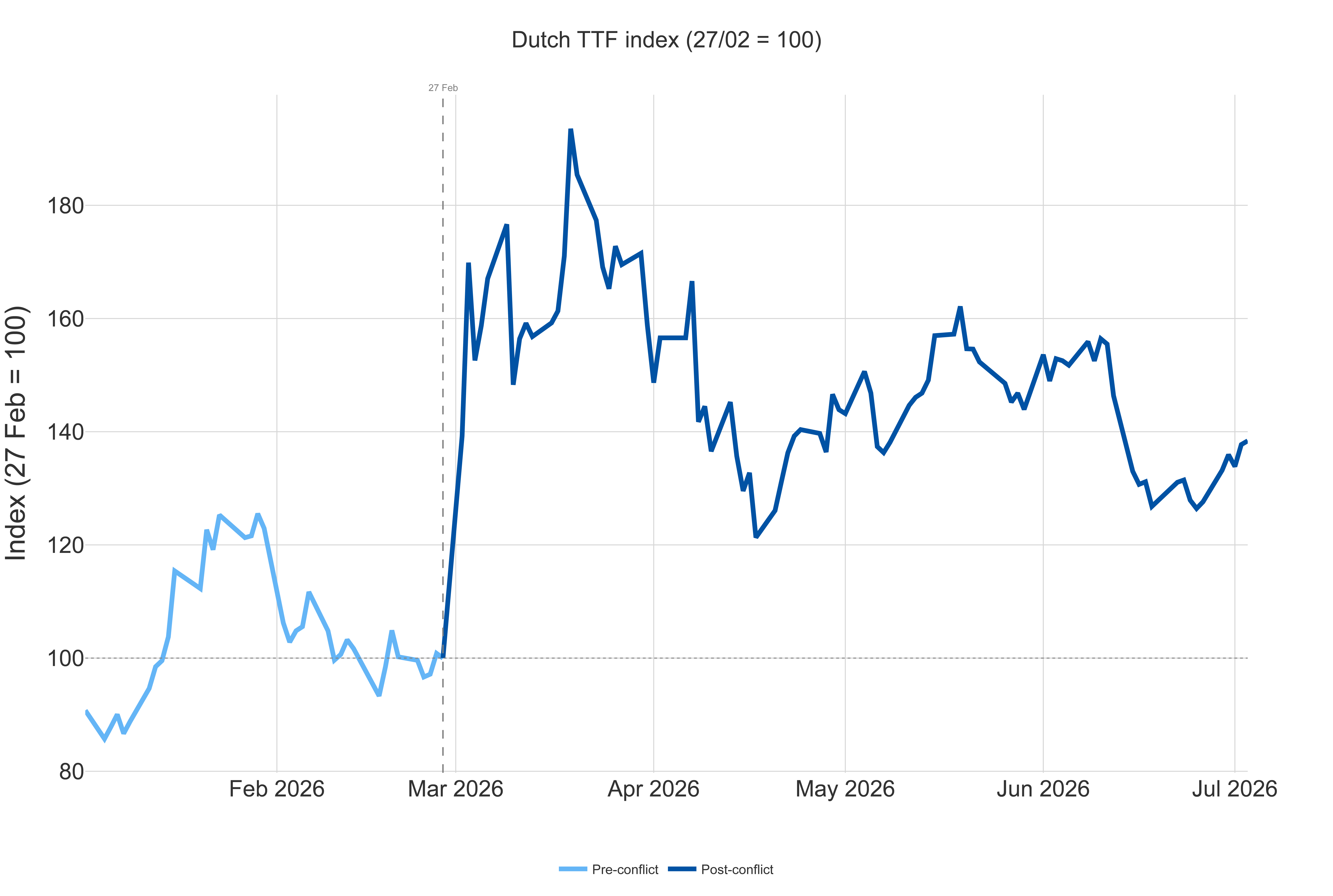

Gas is no longer following crude.

Dutch TTF reached EUR 44.22 per MWh on 3 July, up 8.4% on the week and 38.4% above the 27 February baseline. The weekly path is also different from Brent: TTF moved from EUR 40.40 per MWh on 25 June to EUR 44.01 on 2 July before reaching EUR 44.22 on 3 July.

The problem is structural. Lost Qatari LNG capacity and a smaller summer cargo pool keep Europe competing with Asia while storage still needs rebuilding.

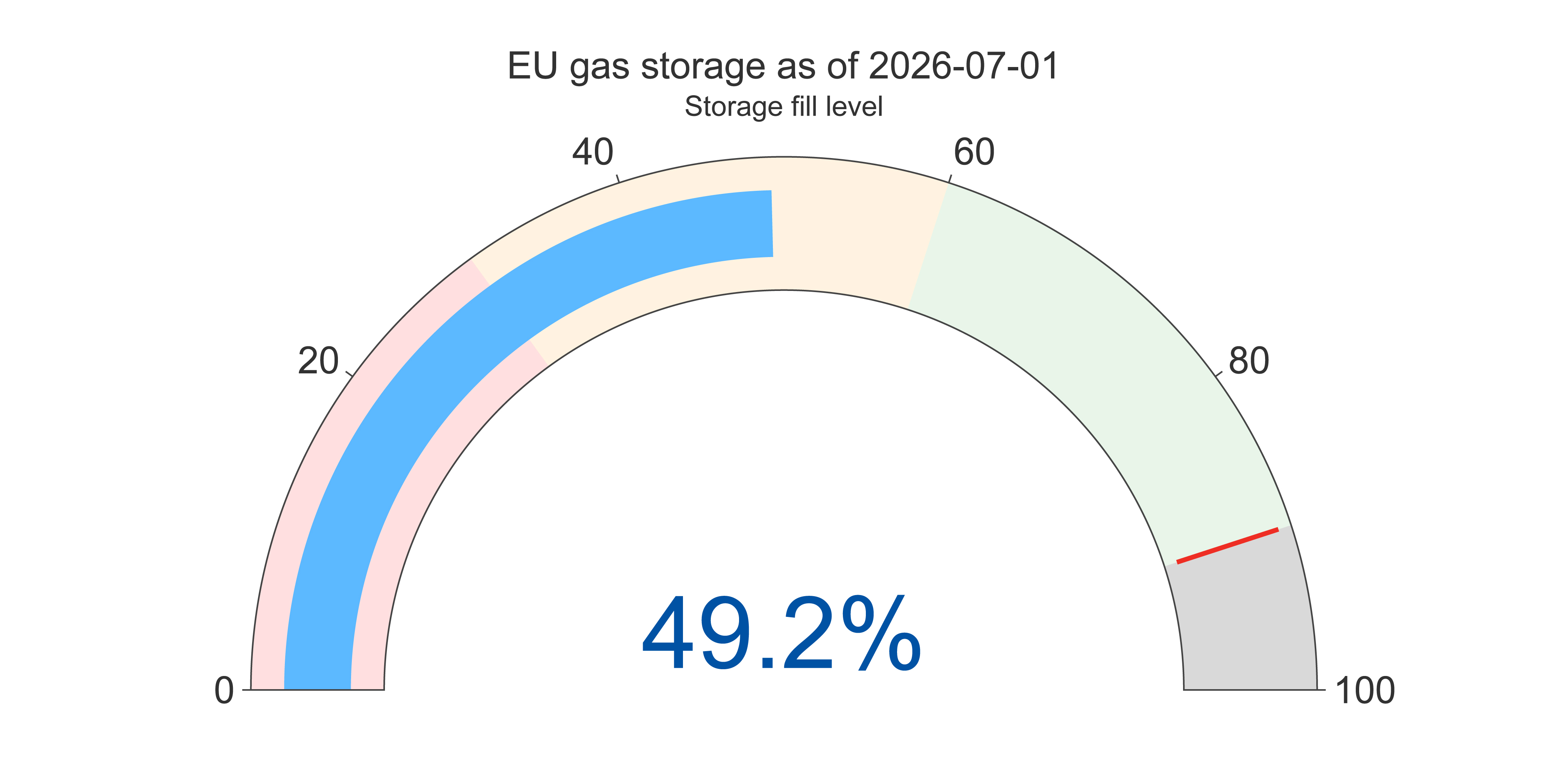

EU gas storage is 49.2% full, equivalent to about 59 days of average annual EU demand, up from 41.3% a month ago but still thin for this point in the injection season. Ireland is estimated at 29.5%, Latvia at 32.8%, Bulgaria at 36.1%, and Croatia and Sweden at 39.4%.

That makes gas the less forgiving part of the energy picture. A ceasefire can reopen routes and lower oil-risk premia, but it cannot quickly replace damaged liquefaction capacity or rebuild storage. Europe still needs summer injections, and Asian demand can limit the downside if cargoes remain scarce. For July procurement, gas should therefore be treated as a separate pressure line, not as a delayed version of the crude relief.

For road transport, gas lands twice: directly for LNG-powered fleets and indirectly through AdBlue. Industry-reported AdBlue prices remain around EUR 0.65-0.90 per litre in bulk and EUR 0.90-1.20 per litre at the pump, well above pre-crisis levels. Gas can account for up to 80% of variable urea production costs. The practical July message is therefore mixed: crude is finally helping, but national tax cliffs and gas-linked inputs are still blocking a clean fall in operating costs.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.

IRU members, strategic partners an Intelligence subscribers already have full access to the IRU fuel prices service.