At the time of IRU’s last fuel prices update, two weeks ago, road transport operators might have thought the worst was behind them. Today, volatility has returned in both crude supply and diesel price dynamics. Government support measures however are not keeping up.

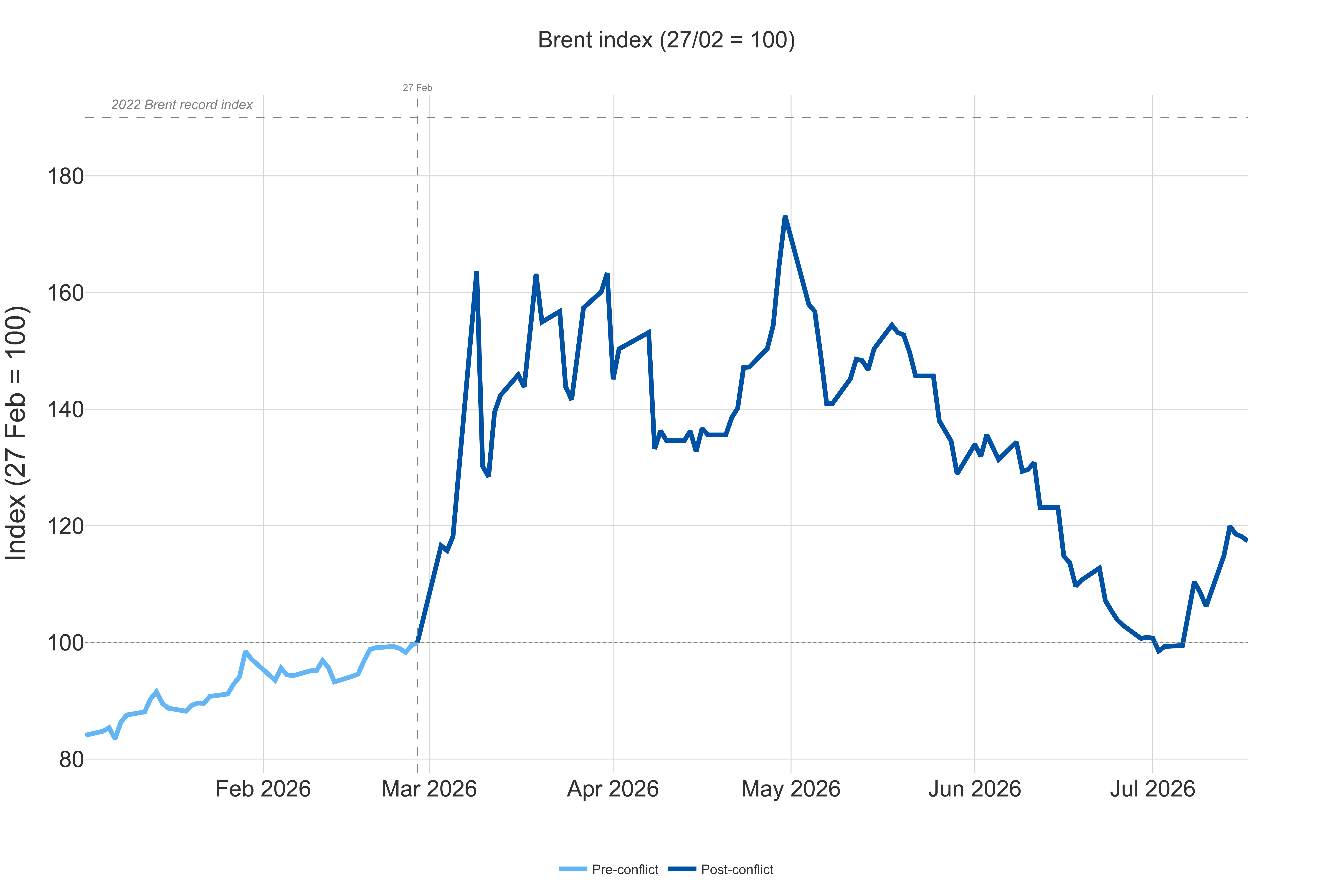

On 3 July, Brent crude was trading at USD 72.5 per barrel, below its late-February pre-war reference level. Since then, the situation has reversed sharply. Two separate developments have pushed crude oil prices back up: renewed disruption to oil tankers passing through the Strait of Hormuz, the narrow shipping route that carries a large share of the world's oil, and a halt to diesel exports from Russia.

With the expiration of most recent measures taken by national governments to mitigate high energy prices, diesel prices have soared. Here is the latest overview of the global energy situation for the road transport sector.

Crude landscape

By 17 July, Brent crude had climbed to USD 85.5 a barrel, up 18% in just two weeks, and 17% above the late-February baseline. West Texas Intermediate (WTI), the main US oil-price benchmark, rose in step, reaching USD 80.1, up 16% in two weeks.

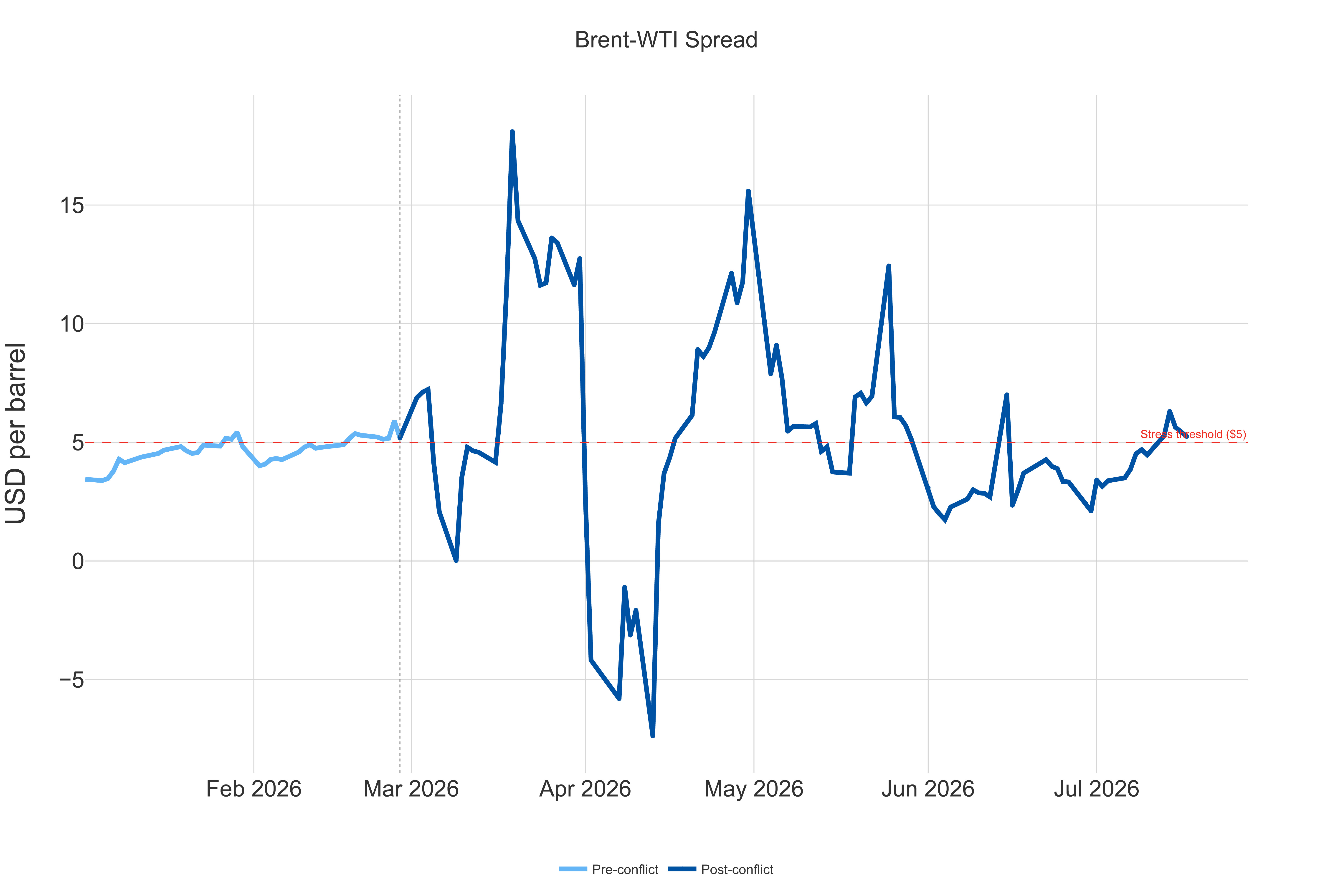

The gap between the two benchmarks, known as the Brent–WTI spread, also widened, from USD 3.4 to USD 5.4 a barrel. This spread usually stays narrow, since Brent and WTI compete in the same global market. When the gap widens, it is a sign that supply strains are concentrated in the Atlantic Basin or European markets, but not both. It signals a regional rather than a global problem.

The International Energy Agency (IEA) published its July Oil Market Report on 10 July. It describes the oil market as moving back into balance but warns that this improvement is fragile and depends on tanker traffic through the Strait of Hormuz continuing to recover, which has been in doubt since the start of this week.

By June, global oil demand was recovering from its May low of 97.9 million barrels a day (mb/d), itself down 5.3 mb/d compared with a year earlier. Even so, the IEA expects full-year demand for 2026 to average 103.5 mb/d, which would be about 1 mb/d lower than in 2025.

On the supply side, output rose 4.1 mb/d in June to 98.8 mb/d, as exports from Middle East producers around the Strait of Hormuz recovered to 16.1 mb/d – still roughly 8 mb/d below February levels. Putting demand and supply together, the IEA now expects the world to consume about 0.9 mb/d more oil than it will produce in 2026, a shortfall that can only be made up by drawing down stockpiles.

Global oil stocks tracked by the IEA did rise by 21 million barrels in June, the first monthly increase since February. But this doesn't mean that the supply squeeze is easing. The entire increase was oil sitting in tankers at sea (117 million barrels), rather than oil being delivered and stored on land. Stocks held on land fell by a further 96 million barrels, including 44 million barrels drawn from government emergency reserves, leaving stockpiles held by OECD governments at their lowest level since December 1990.

Crucially, the IEA points out that supplies of refined fuel products like diesel are recovering more slowly than crude oil itself. Shipments of refined products leaving the Gulf are still running at less than half their February pace, compared with nearly three-quarters for crude oil, and Russia's diesel exports have roughly halved since June. This combination is why the shortage is affecting diesel more seriously than on oil supply more broadly.

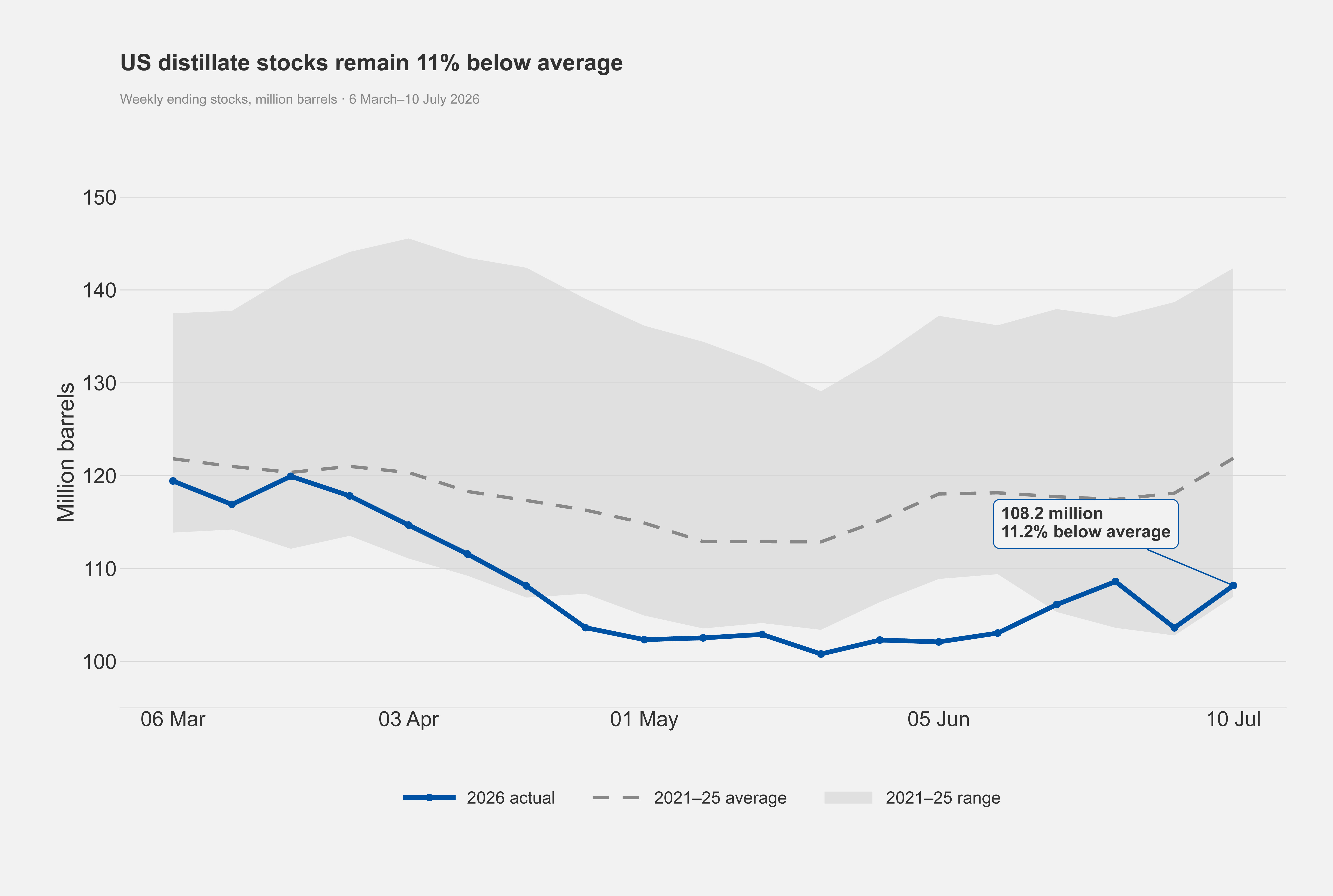

The latest US data show the same pattern. With American refineries running at 96.2% of capacity, stocks of diesel-type fuel (known as distillates) rose by 4.6 million barrels in the week to 10 July, continuing June's stronger-than-usual build (+6.3 mb). Even so, those stocks remain about 11% below their normal five-year average. Crude oil stocks, meanwhile, fell to 409.7 million barrels, 6% below average and the lowest level since September 2018.

In short, refiners around the world are drawing down their reserves of crude oil to rebuild a thin cushion of diesel supply. However, this could come under renewed pressure again in August.

OPEC published its own monthly report on 13 July. Its outlook points in the same direction as the IEA's, although differs in some details. OPEC cut its forecast for 2026 demand growth for the third month running, down 190,000 barrels a day, to a total increase of 780,000 barrels a day, bringing 2026 demand to 105.94 mb/d. China (down 110,000 barrels a day) and India (down 60,000 barrels a day) accounted for most of the downgrade. Even after that cut, OPEC's demand estimate for this year is still about 2.4 mb/d higher than the IEA's.

On the supply side, independent estimates put combined output from OPEC+ (OPEC member states together with allied producers such as Russia) at 36.28 mb/d in June, up by almost 3 mb/d on the month, but still around 6.5 mb/d below where it stood in late February. With supply growth from countries outside OPEC+ holding at around 640,000 barrels a day, OPEC's own numbers point to a sizeable shortfall this year if Gulf output stays constrained near current levels.

Whichever demand estimate turns out to be right, both OPEC and the IEA are describing the same basic picture for 2026: the world is using more oil than it's producing, and the difference is being made up by running down stockpiles.

Refining: Air to road

In the meantime, Europe's refiners are pivoting from jet fuel to diesel production. From March to June, refiners had been maximising jet fuel output, since the profit on jet fuel was higher than on other fuels. That pattern has now reversed, according to the industry pricing agency Argus. Refining "margins," sometimes called "cracks" or "crack spreads," measure the profit a refinery makes on a barrel of crude oil once it's turned into a specific fuel.

The margin on diesel is now close to USD 70 a barrel, comfortably above that for jet fuel which has fallen to about USD 60. Diesel is now priced above jet fuel for three consecutive weeks, the first time that's happened this year, and Argus's analysts expect that premium to hold over the coming months.

Two things could complicate this. Firstly, with Russian diesel off the market, Europe now has to compete with Türkiye, North Africa and Brazil, and for cargoes from the US to secure replacement diesel supply. Secondly, jet fuel stockpiles, already heavily depleted and not expected to rebuild before the new year, could be vulnerable if oil supply tightens again.

Price at the pumps

Behind the rise in crude oil prices, the real focus for road transport is diesel. Russia's total ban on diesel exports, in force since 8 July and due to run until 31 July, has added to two other pressures already in play: lower refinery output in the Middle East, and seasonal demand for fuel, which peaks over summer.

As a result, European refining margins for diesel have reached a three-month high, more than triple their long-run average. This is why diesel prices are rising considerably faster than the rise in crude oil alone would suggest, and two to five times faster than petrol prices in most European markets.

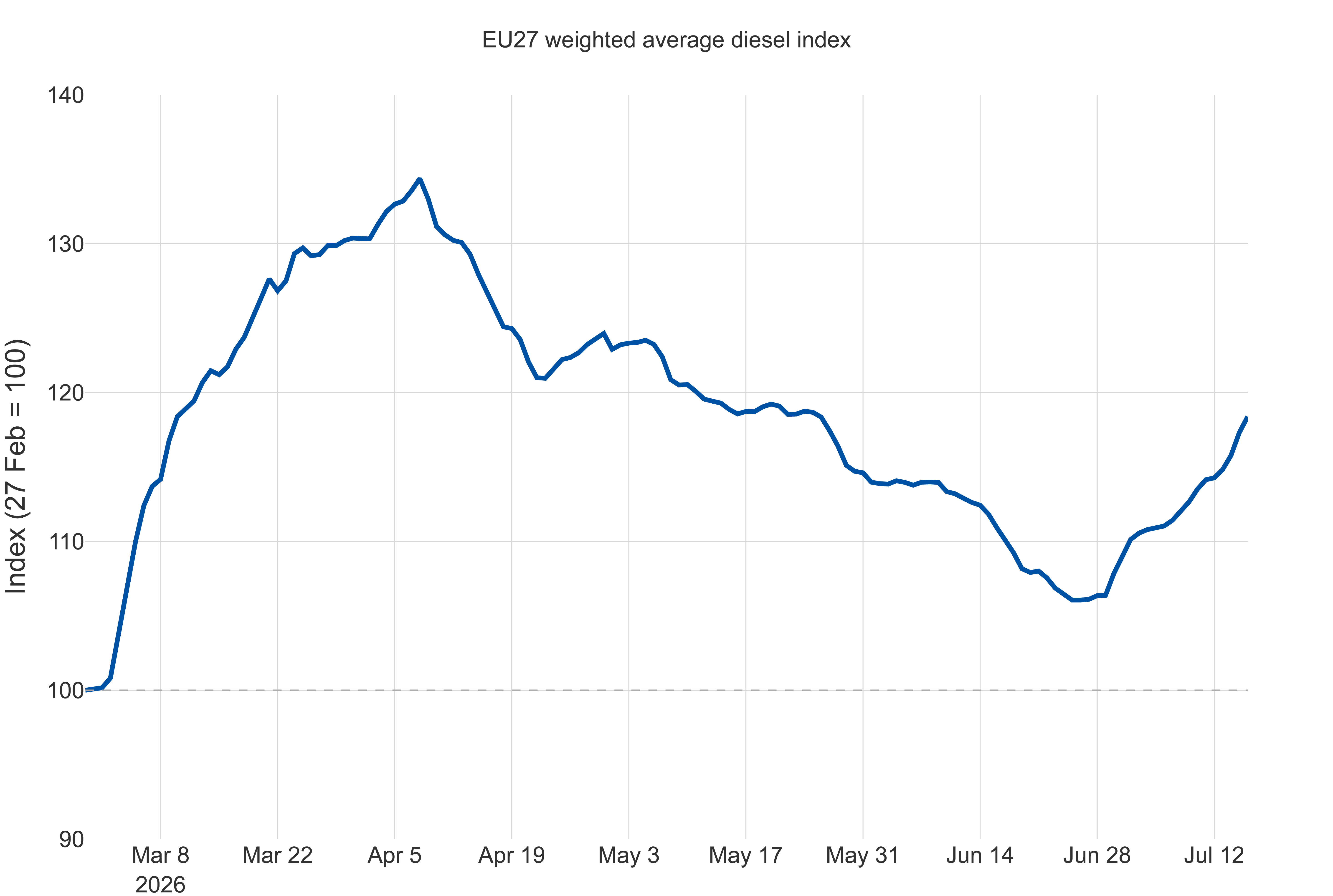

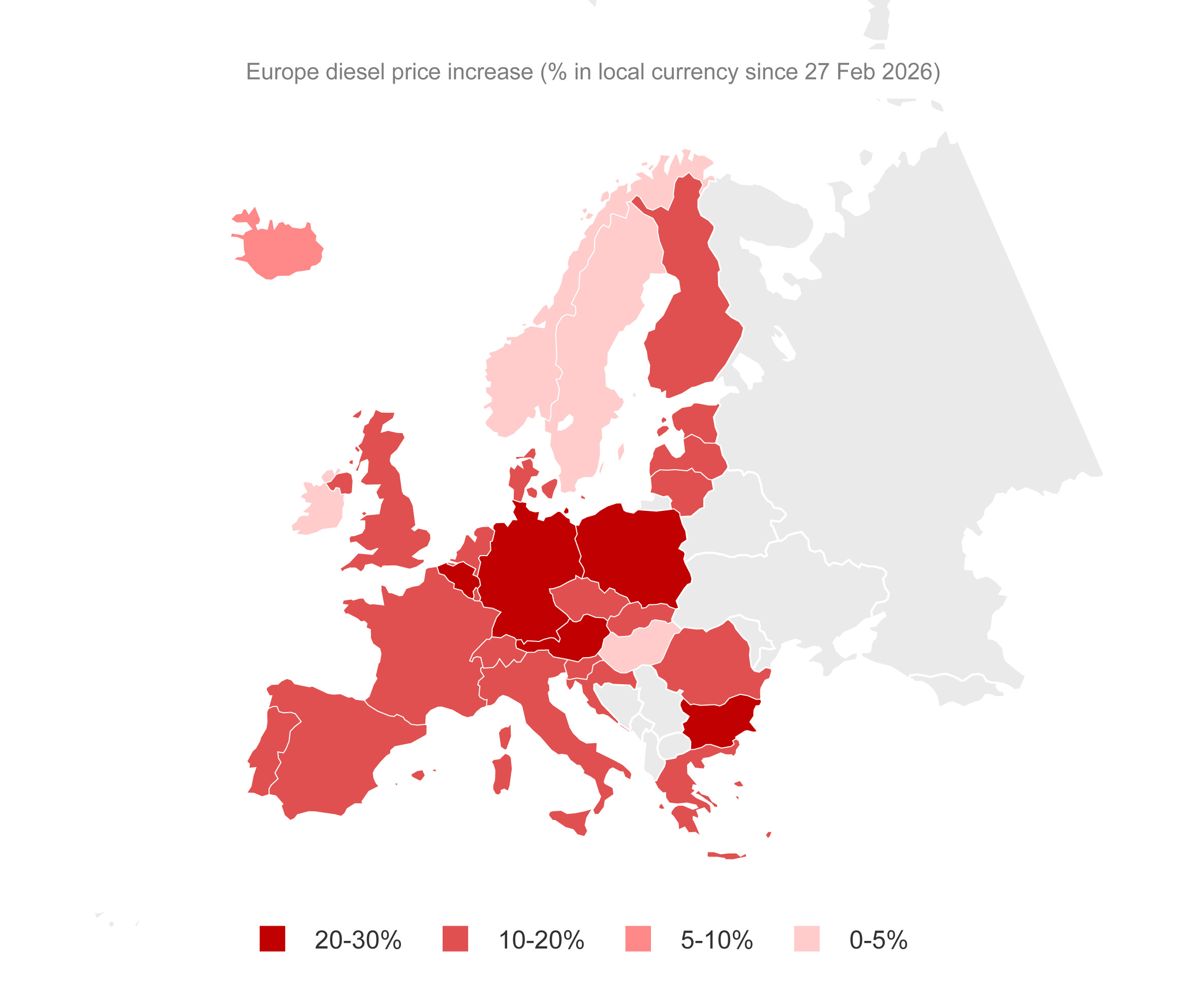

These cost increases have shown up quickly at European pumps. The average diesel price across the EU's 27 member states – weighted by how much fuel each country uses – reached EUR 1.929 per litre on 16 July. This is up from around EUR 1.80 two weeks earlier (a 7% rise), and 18% above the late-February pre-war baseline of EUR 1.634.

Eight of the 27 EU member states now have average diesel prices above EUR 2 per litre: Denmark (2.24), the Netherlands (2.24), Germany (2.18), Finland (2.07), Belgium (2.06), Italy (2.05), Ireland (2.02) and France (2.02). This is up from just two countries just two weeks ago. The sharpest two-week increases were in Austria (+10.5%), Germany (+10.2%), Denmark (+9.6%) and Luxembourg (+9.5%). Only three countries moved the other way: Sweden (−2.6%), and Cyprus and Romania (both −0.6%).

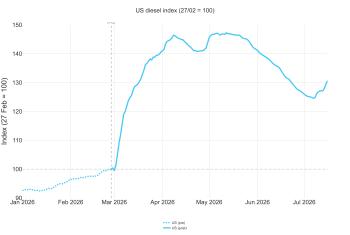

The pressure on prices isn't confined to Europe. In the US, retail diesel reached USD 1.334 per litre on 16 July, up 4.3% in two weeks and 31% since late February, the steepest cumulative rise of any major market.

Price rises have been smaller in China (+4%), India (+9%) and Brazil (+10%) since late February. Two things are cushioning users there. Firstly, these governments use "administered pricing" – setting fuel prices directly rather than letting them move freely with the international market. Secondly, each of these countries refines much of its own oil domestically, rather than depending heavily on imported diesel.

National measures expiring

The past fortnight has seen the withdrawal of government support measures, just as prices move back upwards.

Czechia is a good case: the cabinet decided on 13 July not to extend its twin measures, allowing the retail margin cap and reduced diesel excise to both lapse on 19 July with no successor measures planned.

Italy's excise cut expired on 3 July, while the average diesel price climbed from EUR 1.882 on 2 July to EUR 2 on 17 July.

Germany's rebate ended with June, restoring around 17 cents per litre of energy tax from 1 July, with the coalition ruling out any successor, and Poland's return from 8% to 23% VAT on fuels added roughly 0.87–0.89 PLN per litre in its first week. Austria's price brake survives only nominally, tapered to 0.8 cents per litre for July from 5 cents in April.

Against this trend, several governments are extending or deepening support.

Greece introduced a discount of 5 cents on diesel prices, in force from 14 July to 31 August, funded entirely by the country's two refiners – costing EUR 20 million each, with no cost to the state. However, station operators report that refinery-gate price rises neutralised about two-thirds of the diesel discount within 24 hours, leaving a real cut closer to 1.6 cents.

Serbia went furthest. Rather than letting its 10% excise cut lapse on 19 July, the government doubled it on 16 July to 20% for 20–26 July, although the measure now runs as a weekly instrument.

Ireland extended its excise reduction of 32 cents per litre on the price of diesel to 31 August, with a four-step restoration planned from September to December, and prolonged the enhanced Diesel Rebate Scheme for hauliers to 30 September.

Portugal increased its weekly fuel-tax rebate from 13 July and Spain, despite letting fuel VAT revert to 21% on 1 July, is offsetting it with a hydrocarbon-tax cut of 15 cents per litre in July (tapering to 10 cents in August and 5 cents in September) and extended its haulier diesel aid to 30 September. Sweden's carbon-tax cut of about 3 kronor per litre including VAT (1 July–30 November) briefly made its pumps the cheapest in the EU for petrol, although diesel has already surrendered around 1.25 kronor of the cut in a fortnight.

Latvia's reduced diesel excise now runs to 31 December, and Cyprus' to 17 September.

In countries where prices are more directly administered by the state, pressure is showing up inside the systems rather than at the pump.

Hungary quietly abolished its price cap on 27 June, once market prices had fallen below it, replacing it with a standing power to re-impose administered prices by decree.

Countries with dynamic price cap systems including Croatia, Montenegro, North Macedonia and Slovenia all saw heavy increases in diesel prices at their mid-July resets. Slovenia's diesel price rose 8.3 cents against 2.7 for petrol, with excise explicitly untouched, confirming that the current surge is a refining-margin event, not a tax one. Croatia's government estimates that its combined excise and margin measures are still shaving 12–13 cents per litre off what diesel would otherwise cost.

For road transport specifically, the pattern is small, targeted measures that lag the cost shock.

Finland's draft professional-diesel refund for heavy transport offers 3.3 cents per litre, about a fifth of what IRU member SKAL demanded.

The Netherlands' new truck vehicle-tax zero rate (1 July–31 December) is worth roughly EUR 300 over six months to a heavy-duty truck, vastly less than the EUR 300 per week in extra fuel cost faced by that same truck. Hauliers in the country are pressing for an excise cut instead.

The UK remains an outlier in both directions: duty frozen at 52.95 pence to end-2026, an HGV vehicle-duty holiday, and red diesel relief, resulting in pump prices that are flat to falling.

Outside Europe, Mexico raised its diesel excise stimulus for a second consecutive week (now offsetting about 26% of the full rate), Canada's federal excise holiday runs to 7 September, Australia's regulator is auditing station-level pass-through of the restored 16-cent excise with monitoring extended to 30 September, Türkiye's cancellation of the July automatic fuel-tax update is holding even as market prices pass crude through, and Argentina's deferred tax catch-up begins on 1 August.

Outlook: what to watch

Two things will determine whether the diesel price shock described in this report keeps building or starts to ease over the next two weeks. The first is Russia's diesel export ban, currently due to expire on 31 July. If it lapses as planned, some of the pressure on European diesel prices should start to ease; if Russia extends it into August however, the price squeeze would likely get worse before it gets better. The second is whether tanker traffic through the Strait of Hormuz recovers.

On the government-support side, two dates stand out. On Sunday 19 July, Czechia's retail margin cap and reduced diesel excise both lapse with no replacement planned, which should push diesel prices there higher almost immediately. And Serbia's doubled excise cut is currently only confirmed to 26 July; as it runs on a week-by-week basis, it will need another government decision to be renewed beyond that date.

More broadly, watch whether other governments follow Czechia's and Italy's lead in letting support measures expire rather than renewing them, now that prices are rising again.

Beyond the next two weeks, watch for Argentina's deferred fuel-tax catch-up on 1 August, and several European support measures that will be watered down in August, including Spain's hydrocarbons-tax cut, tapering from 15 to 10 cents per litre.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.

IRU members, strategic partners an Intelligence subscribers already have full access to the IRU fuel prices service.