On 22 May 2026, Brent crude is trading at around USD 105 a barrel, down 4% from last week. Diesel pump prices have started to ease in several markets, but the European fiscal-cliff calendar is now densely packed into the last week of May and the first week of June. Here is the latest overview for the road transport sector.

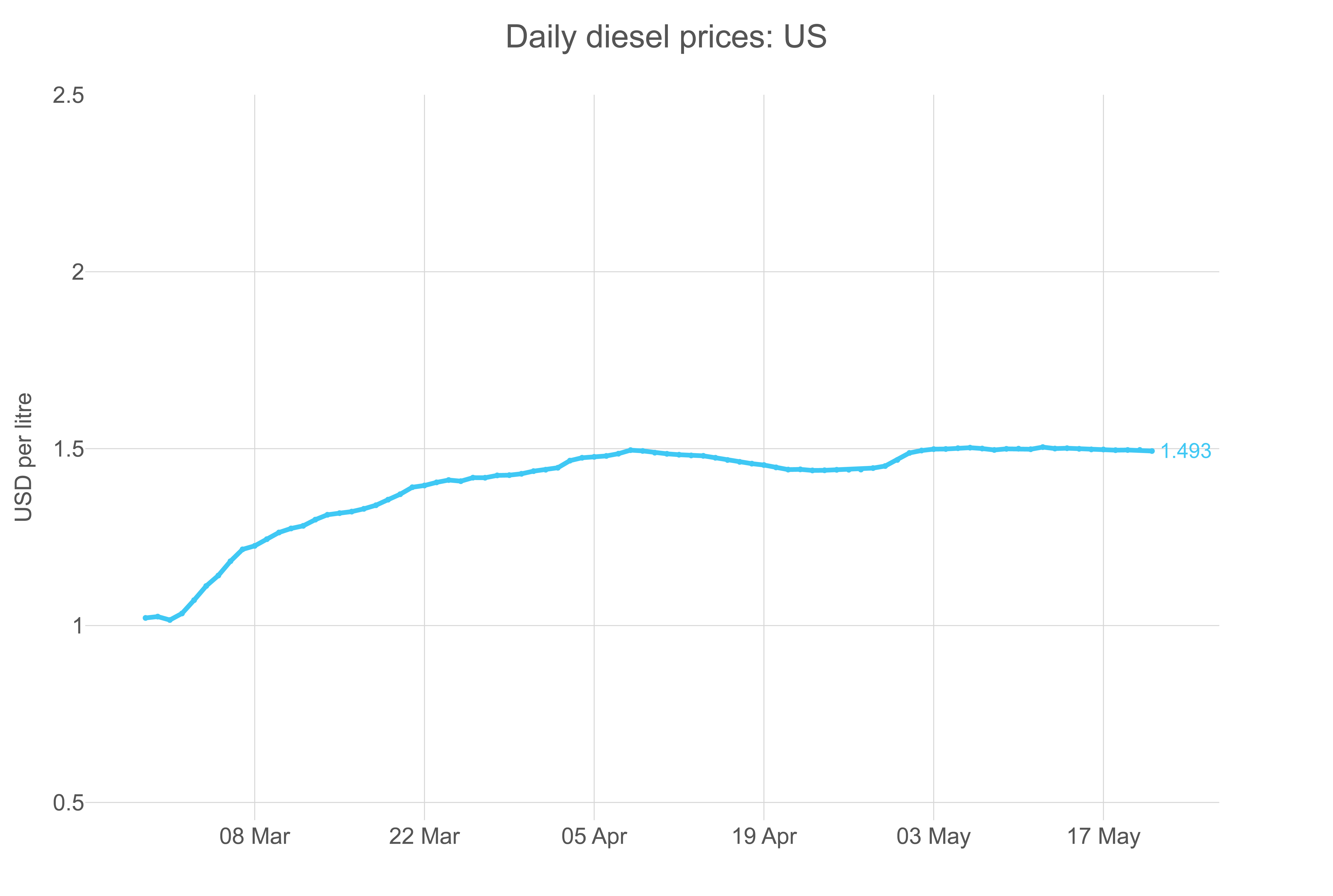

- The US national average diesel price stabilised at USD 1.493 per litre on 21 May

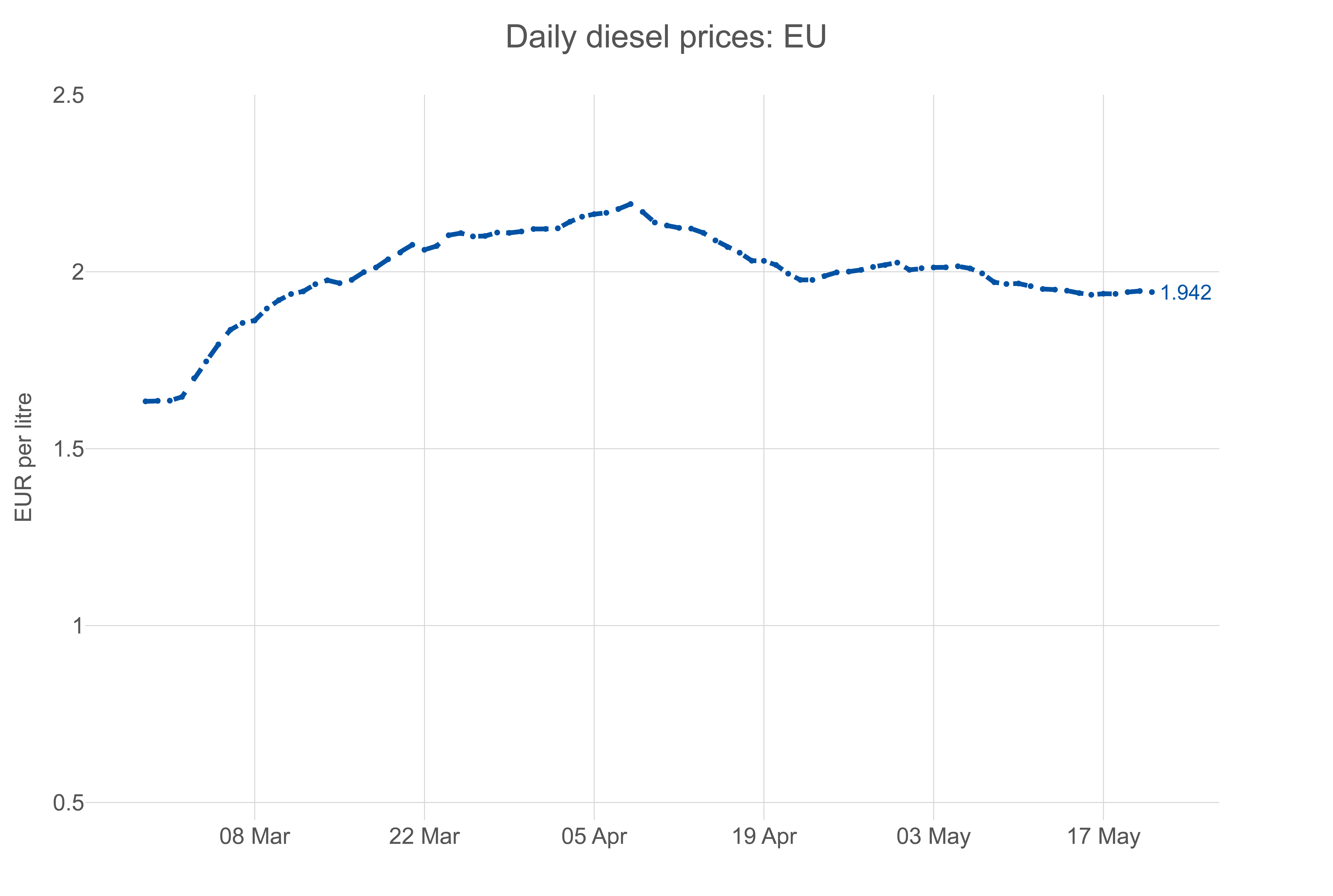

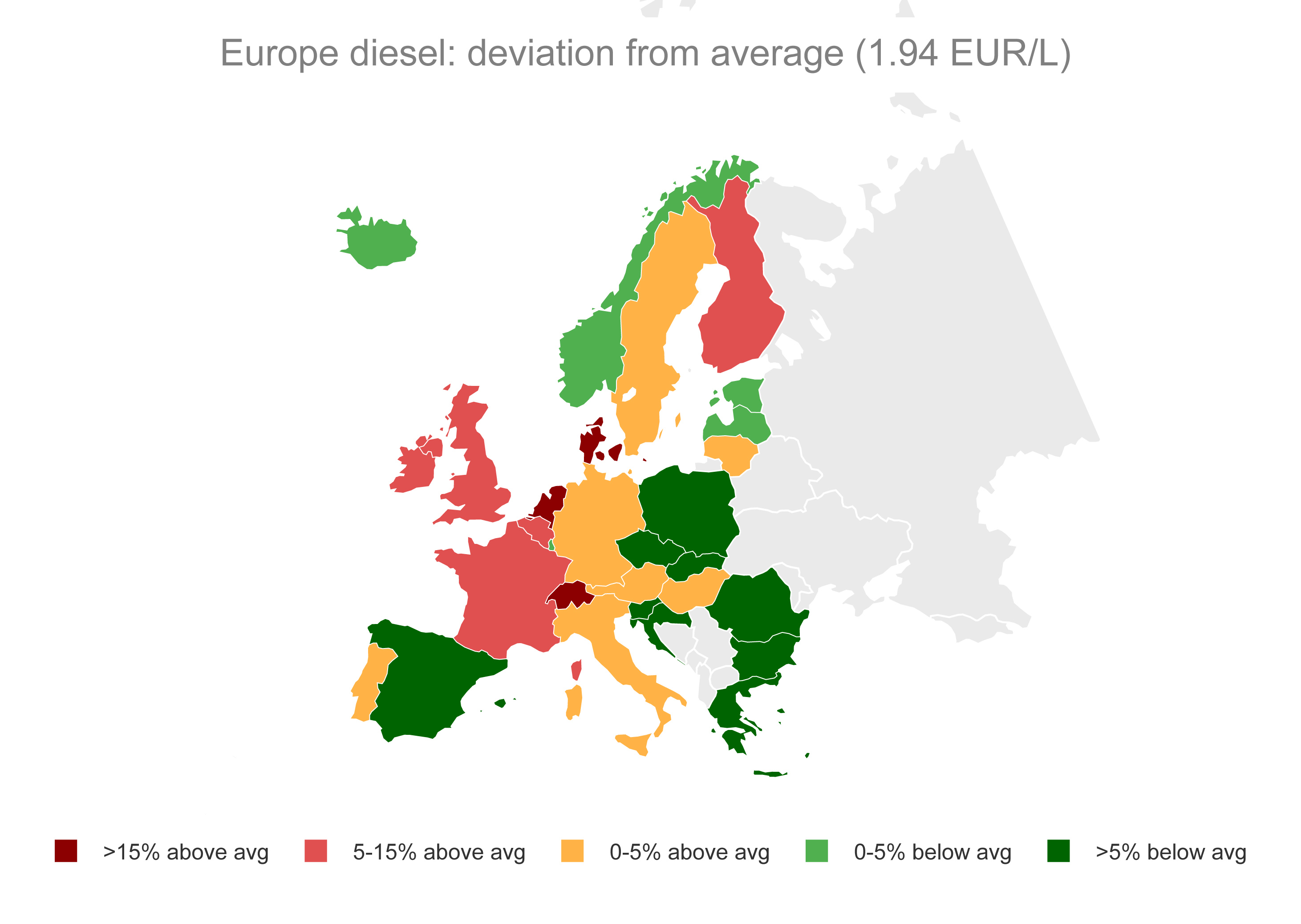

- In the EU, the average diesel price is EUR 1.942 per litre, a 0.3% increase week on week

- Italy’s Council of Ministers convenes today to extend the EUR 0.244 per litre diesel and EUR 0.061 per litre petrol excise cuts into the first week of June

- Cluster of European fiscal-cliff decisions converges on 31 May to 7 June

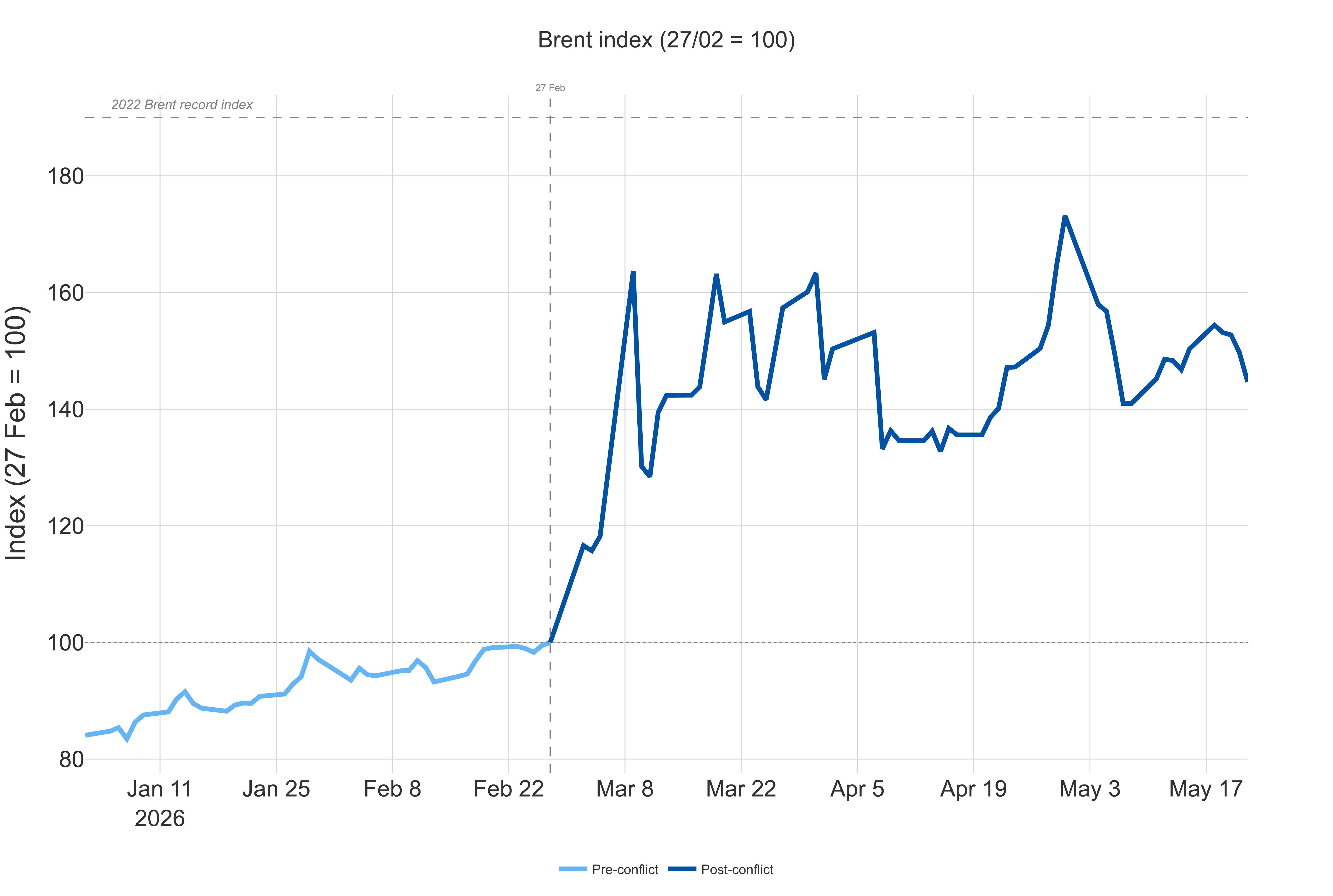

Brent crude settled at around USD 105 a barrel on 22 May, down 4% from last week. WTI is tracking just short of USD 100 a barrel.

The International Energy Agency’s (IEA) 13 May Oil Market Report quantifies the depth of the shock. Global oil supply declined by a further 1.8 million barrels a day in April to 95.1 million barrels a day, taking cumulative losses since February to 12.8 million barrels a day.

Output from Middle Eastern countries affected by the closure of the Strait of Hormuz is now 14.4 million barrels a day below pre-war levels. Cumulative supply losses from Middle East producers already exceed one billion barrels, which the IEA calls an unprecedented supply shock.

The IEA’s base-case forecast assumes that Strait of Hormuz flows will gradually resume from June, but the oil market remains in deficit until the final quarter of 2026, with a cumulative liquids deficit of around 900 million barrels by September. Rebuilding stocks, strategic reserves included, would require roughly an additional 1 million barrels a day of supply for the next three years on top of underlying demand growth.

On strategic stocks, the IEA collective action launched on 11 March is now visibly accelerating. As of 8 May, around 164 million barrels of oil have been released under the 400-million-barrel commitment, consisting of 90 million barrels from government stocks (82 million crude and 8 million products) and a further 74 million barrels made available through lower industry stockholding obligations.

Government releases ran at an average of 2.1 million barrels a day through April. The IEA expects an additional 210 million barrels of government stocks and around 45 million barrels of obligation-based industry stocks to flow through to end-July, the vast majority as crude oil. Around 70% of the public-stock releases in March were oil products, gasoline and middle distillates, predominantly in European countries. The US Department of Energy separately released 53.3 million barrels from the Strategic Petroleum Reserve on 12 May.

The macroeconomic toll is now formally on the European Commission’s books. In its forecast released on 21 May, Brussels cut its 2026 eurozone GDP growth forecast to 0.9%, down from 1.2% in November, and revised the inflation projection up to 3% from 1.9%.

Germany is now expected to grow by just 0.6%, half the November estimate; France is held at 0.8%. The European Commission’s alternative scenario, in which energy prices continue to rise until the end of 2026, sees inflation failing to slow and growth failing to recover in 2027.

Pump prices

In the EU, the average diesel price is EUR 1.942 per litre, a 19% increase since the start of the war and a 0.3% increase week on week.

At EUR 1.607 per litre, Poland has the lowest diesel price (excluding Malta), while the Netherlands has the highest price at EUR 2.367 per litre.

Prices are notably on the rise again in Belgium, Finland, Hungary, Slovenia and Spain. Shortages are also on the rise in France and Hungary.

Pénurie-carburant.fr recorded 447 stations with a total diesel outage on 21 May in France, about 5% of the stations monitored, and a doubling from the 2.0% print recorded on 18 May. France is also the clearest live case of demand destruction in Europe.

Economy Minister Roland Lescure confirmed on 22 May that French fuel consumption was down 14% year on year over the first three weeks of May, following an 11% year-on-year decline in April.

Ufip Énergies et Mobilités, citing the Comité Professionnel du Pétrole, reports diesel deliveries were down 9.1% in April (2.54 million m³) against just a 0.9% decline for petrol, with total road-fuel deliveries down 6.5%.

In Hungary, despite the 575 million litres released from the strategic reserve under the 14 May decree, the Association of Independent Petrol Stations warned on 21 May that diesel reserves are running low, and that replenishment is uncertain and costly.

The US national average diesel price stabilised at USD 1.493 per litre on 21 May, up around 46% since 27 February.

In Türkiye, diesel reached TRY 69.99 per litre on average this week, a 13% increase from the 27 February baseline. Treasury and Finance Minister Şimşek’s sliding-scale ÖTV mechanism continues to absorb the bulk of the upward pressure but is approaching the 2 March 2026 ÖTV reference level. Analysts warn that the diesel tax buffer is now nearly exhausted.

In China, diesel is around 28% above the pre-war baseline. China continues to prioritise domestic supply over state-owned refiner margins, with export restrictions on refined products in place.

In India, government-administered pricing has held diesel close to pre-war levels (+4%); a US Treasury waiver continues to allow Iranian crude imports via the Chabahar transit route, and export taxes on refined diesel remain in force.

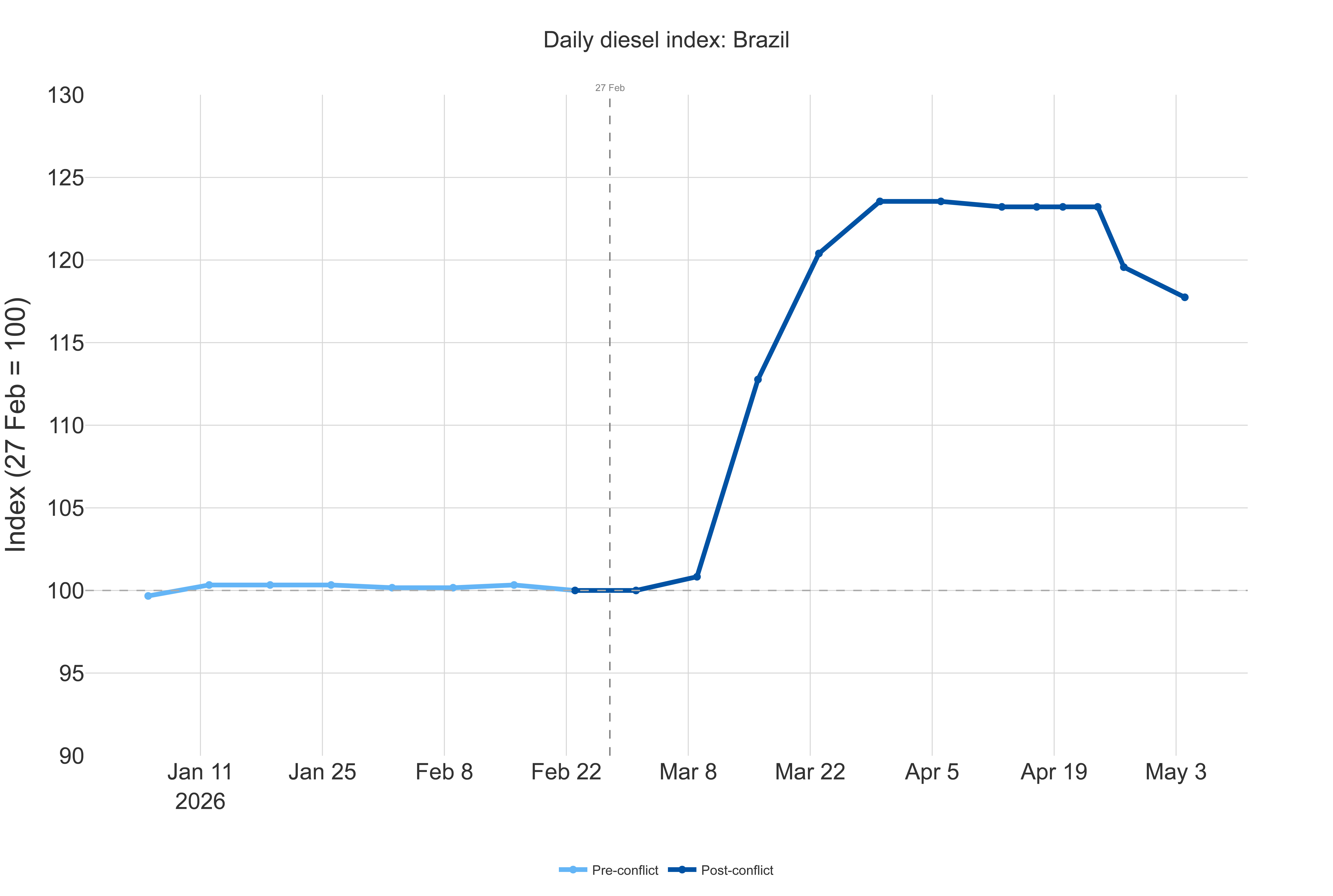

In Brazil, retail diesel is around BRL 7.0 per litre on average this week, with the defasagem softening modestly from 35-40% on diesel on the Brent retracement.

Provisional Measure 1358/2026, signed on 13 May, layers an additional subsidy for Brazil-produced and imported gasoline and diesel on top of the existing MP 1349 framework (BRL 1.20 per litre on imported diesel and BRL 0.80 on domestic).

The Petrobras Board approved adherence to the new subsidy on 21 May, but execution remains blocked by lack of inter-institutional agreement. In the meantime, the federal government delayed the first diesel subsidy payment for March for operators, and said it will be the same for April.

In Argentina, YPF, the majority state-owned energy company, executed a 1% pump adjustment on 14 May and confirmed a new 45-day price-stabilisation window through around 28 June. Shell, Axion and Puma followed within hours. Buenos Aires pump prices stand at around ARS 2,080 on grade-2 gasóleo. The deferred ICL/CO2 tax scheduled for 1 June remains in the buffer window and is likely to be absorbed by YPF rather than passed through to the pump.

In Mexico, retail diesel is at around MXN 27.71 per litre on average. The Ministry of Finance has maintained its weekly IEPS (federal excise tax) stimulus, with diesel at 62.92% under the prior DOF publication (official government gazette); the new DOF for the week of 23 to 29 May is expected to be published today.

Natural gas

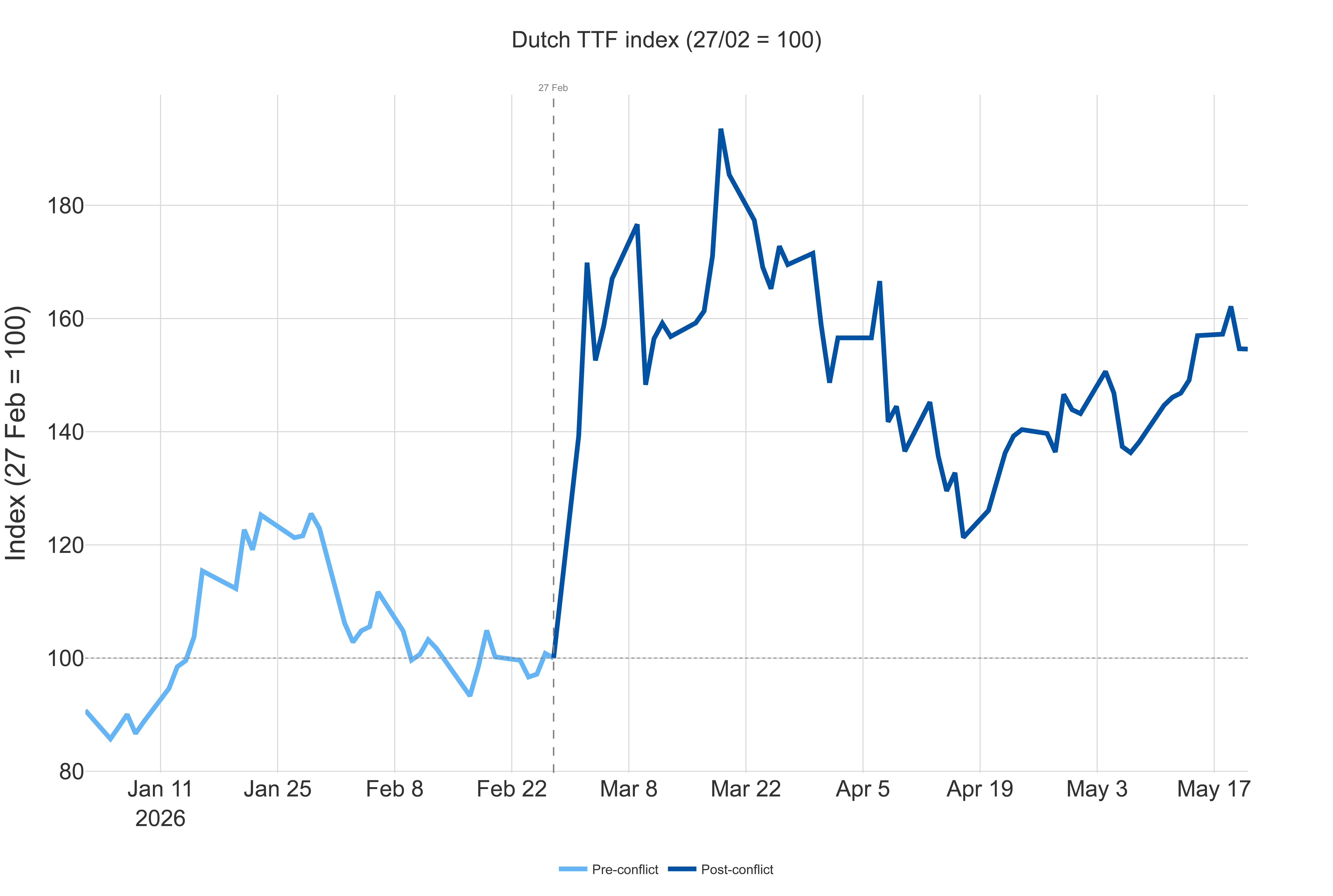

Dutch TTF natural gas continues to track the Brent path, reaching around EUR 49 per MWh this week, down by EUR 1 per MWh from last week. Since the start of the war, the TTF has risen by 53%.

EU gas storage stands at around 37% full at the start of the injection season, the weakest starting position in at least four years. Sweden has the lowest level in the EU at below 10%, with the Netherlands and Germany among the ten countries under the EU average.

Road transport impact

For European operators, this week’s pivot is in Rome. Italy’s Council of Ministers convenes at 19:00 today to issue a fresh “DL accise-quater” extending the cumulative EUR 0.244 per litre diesel and EUR 0.061 per litre petrol excise cut into the first week of June, paired with a transport-sector compensation package.

At the global diesel supply level, the IEA highlights a sharp redrawing of trade flows. Middle Eastern diesel and gasoil exports have fallen from 1.4 million barrels per day in 2025 to around 700,000 barrels a day in April, with exports to Europe down by 270,000 barrels per day and exports to Africa down by 430,000 barrels per day.

Europe is partly insulated because domestic refining covers around 80% of demand, and North American refiners, largely in the US, have increased diesel and gasoil exports by 430,000 barrels a day in April compared with 2025 levels, with around 80% of that volume directed to OECD Europe, Africa and Asia.

As the crisis enters its twelfth week, operators remain exposed to a volatile fuel-price environment despite this week’s diplomatically led retracement.

The Strait of Hormuz remains effectively closed, the OPEC+ buffer has been exhausted, and the European fiscal cliff has shifted from late May to mid-June.

Even if a comprehensive understanding with Iran is reached, the IEA cautions that a return to normal trade flows will be slow.

The only certainty for operators is that fuel prices will remain elevated and unstable through the second half of 2026.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.

IRU members, strategic partners an Intelligence subscribers already have full access to the IRU fuel prices service