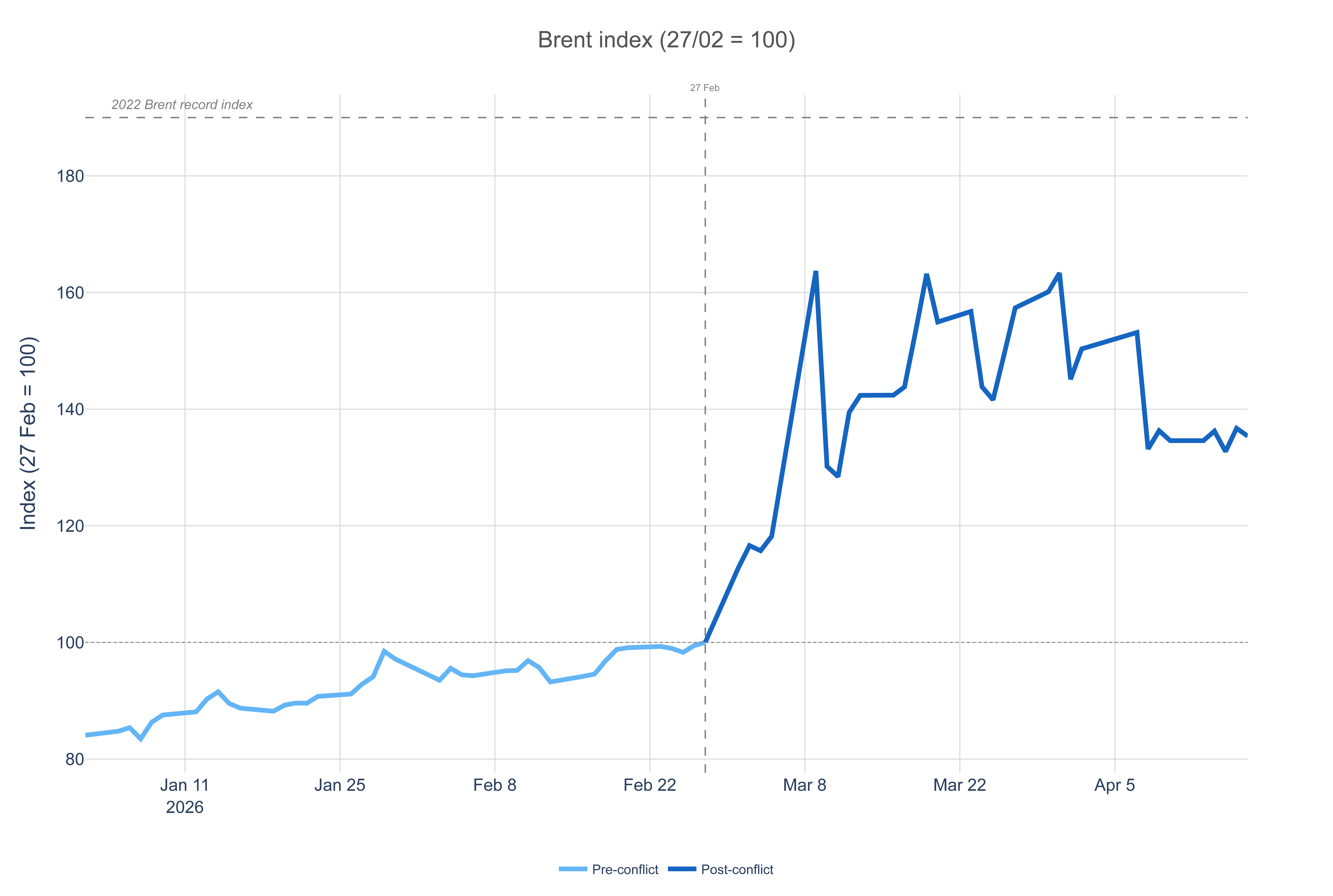

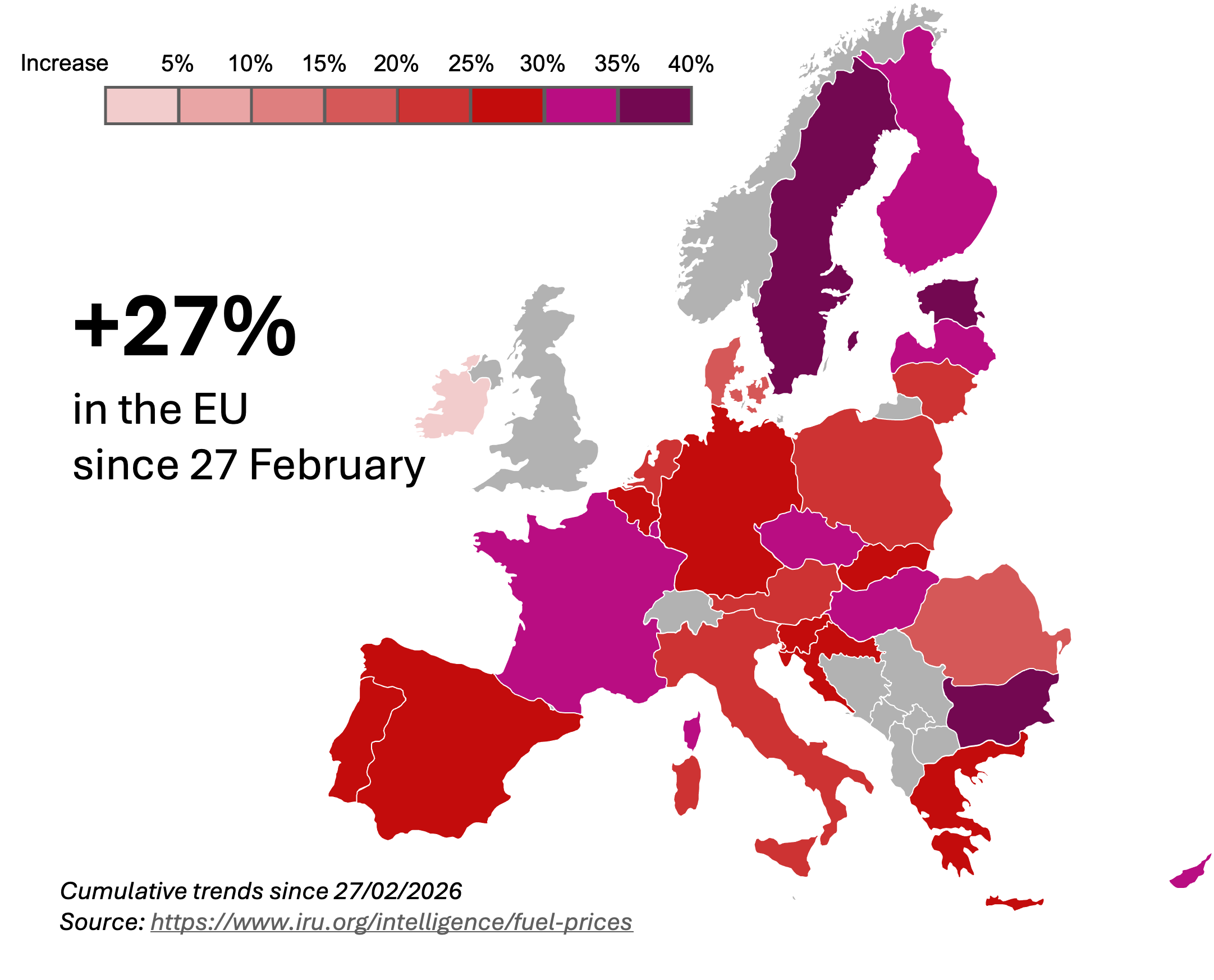

On 17 April 2026, Brent reached USD 98.83 a barrel, up 35% since 27 February, while the week-on-week move was flat at +0.6%. Although huge price gaps remain between countries, EU diesel averaged EUR 2.07 per litre, up 27% cumulatively since the start of the war, down from 33% last week. A similar slight easing of pump prices was also seen in Brazil, Türkiye and the US, but not China. Here is the latest overview for the road transport sector.

- Spot crude prices are around 40% above Brent, meaning refineries pay far more than headline prices suggest

- Global crude supply fell 10% in March, double the worst disruption in any previous energy crisis

- France recorded the steepest rise among the top five EU economies (+34%), although overall EU pump prices have eased

- Germany approved a EUR 0.17 per litre fuel tax cut; a new Spanish law helps operators factor fuel price increases into invoices

Oil markets and supply

Brent, the EU benchmark, reached USD 98 a barrel on Friday 17 April, up 35% since the start of the war.

On the other side of the Atlantic, WTI, the US benchmark, reached USD 94 a barrel, also up 35% over the same period.

However, recent data reported by The New York Times and Argus Media suggests a widening gap between Brent for future delivery, the main benchmark, and the spot price paid for immediate crude purchases.

Under normal conditions, these prices track closely. At present, spot prices are around 40% higher than Brent, meaning refineries are buying crude at a higher cost than the benchmark, which is pushing pump prices up.

Latest IEA data suggests global crude oil supply fell by 10% in March. This is a historic reduction of around 10 million barrels a day. Past energy crises, such as in the 1970s and 1990s, peaked at 5 million barrels a day, with long-lasting consequences.

With 80 production sites damaged since the start of the war, even an immediate reopening of the Strait of Hormuz to crude tankers would take months to restore pre-war conditions.

More importantly, around 80% of production could be reactivated quickly, while the remaining 20% may take years, if it can be restored at all. Adding further pressure to the crude oil market, Iran exported 3.6 million barrels a day in March, a volume now at risk given the current US Strait of Hormuz blockage.

The Brent–WTI spread narrowed slightly. WTI stood at USD 93 a barrel versus Brent at USD 98, a discount of just over USD 5. This is roughly half the typical arbitrage gap and suggests US refiners are pulling domestic crude into product runs to partly offset Middle East shortfalls.

US crude oil exports increased by 25% last week, according to the latest EIA data, rising from 4 to 5 million barrels a day.

Pump prices

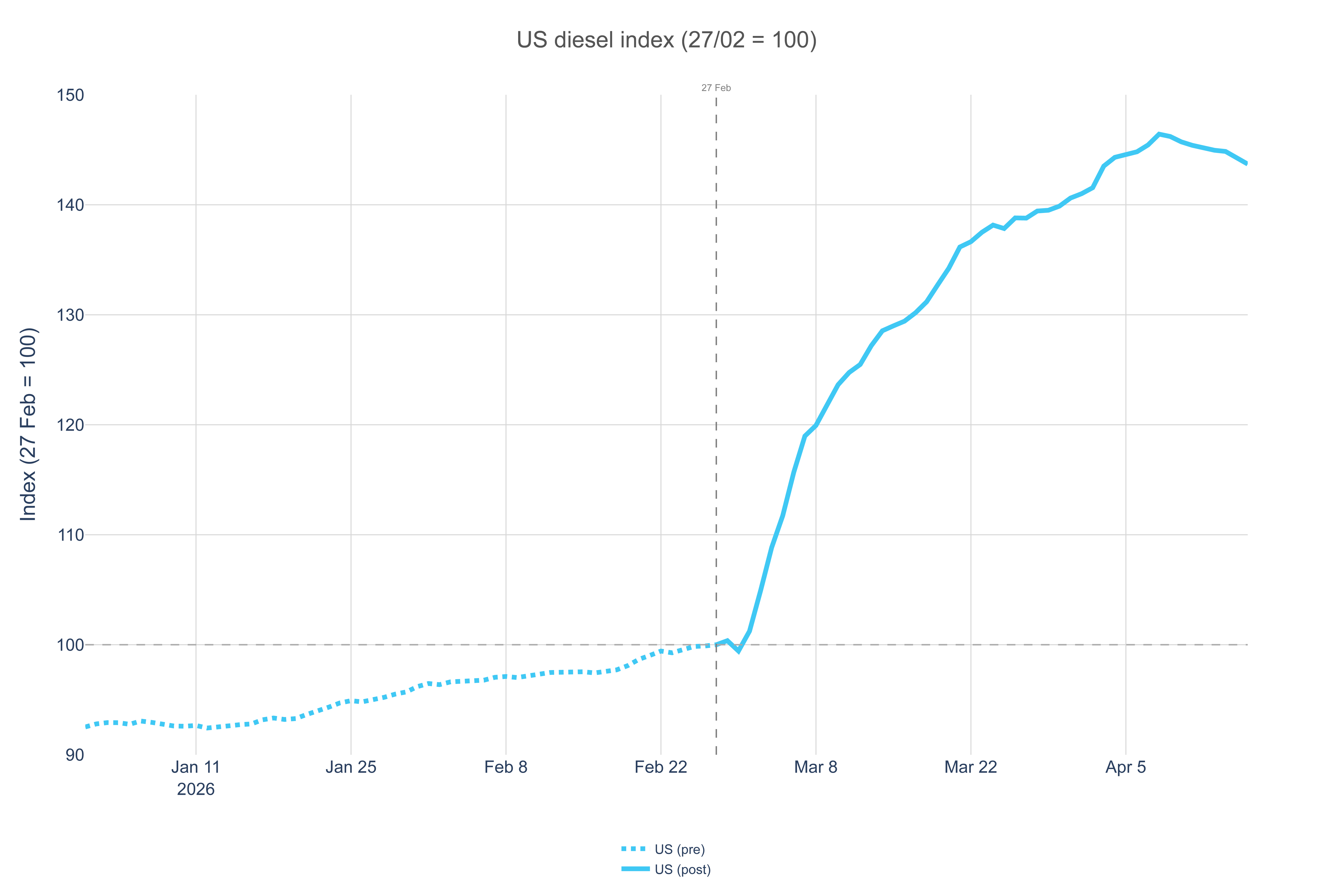

US national average diesel price reached USD 1.5 per litre on 17 April, up 44% since 27 February. This is down slightly on last week’s reported increase of 46% since the outbreak of war but nevertheless remains the steepest rise among all major economies covered in this article.

Some states are considering temporary fuel tax suspensions. However, unlike Canada, which suspended its federal fuel excise on 20 April, the US has not suspended or reduced the federal diesel excise tax. There is also no equivalent of the European-style operator rebate scheme.

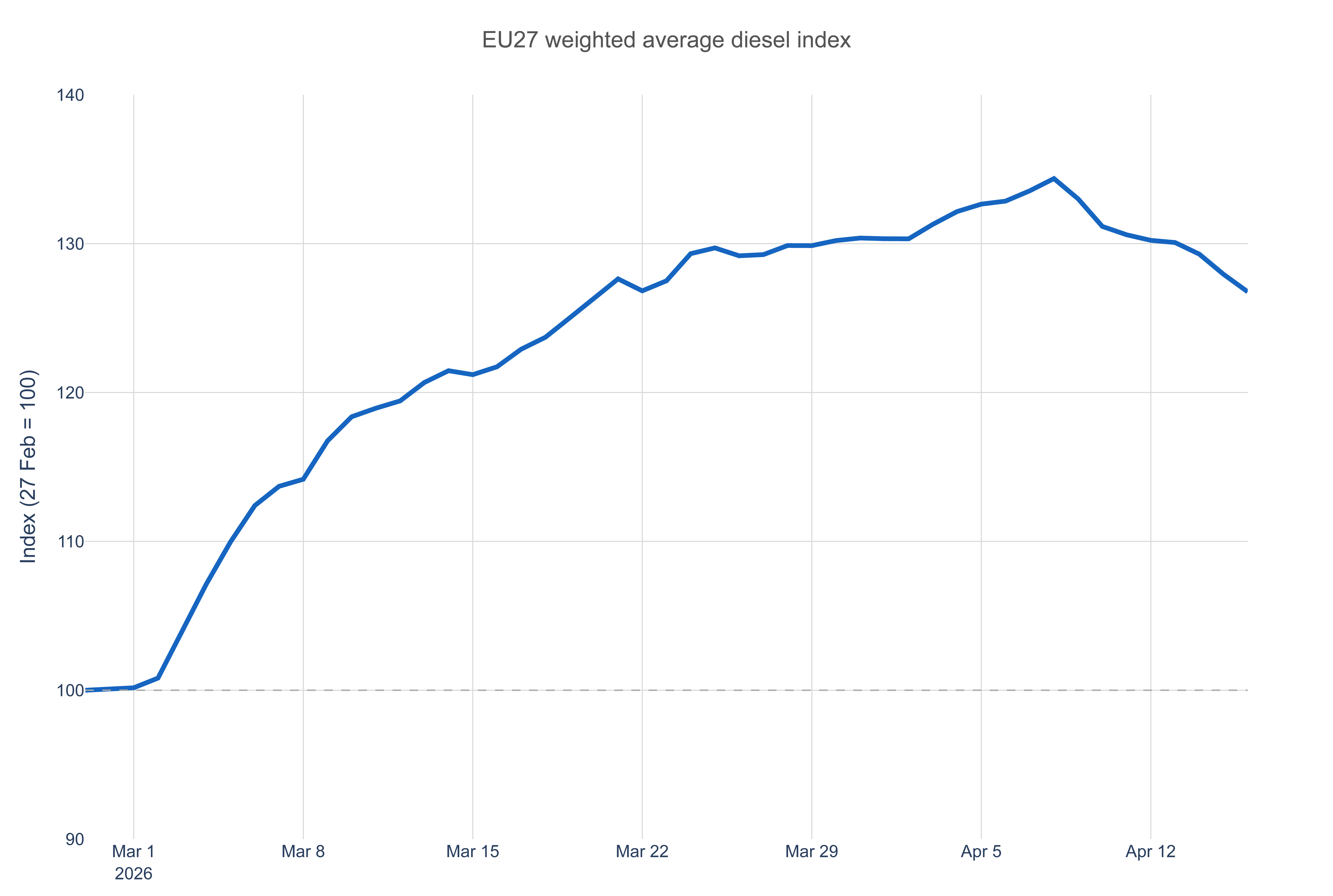

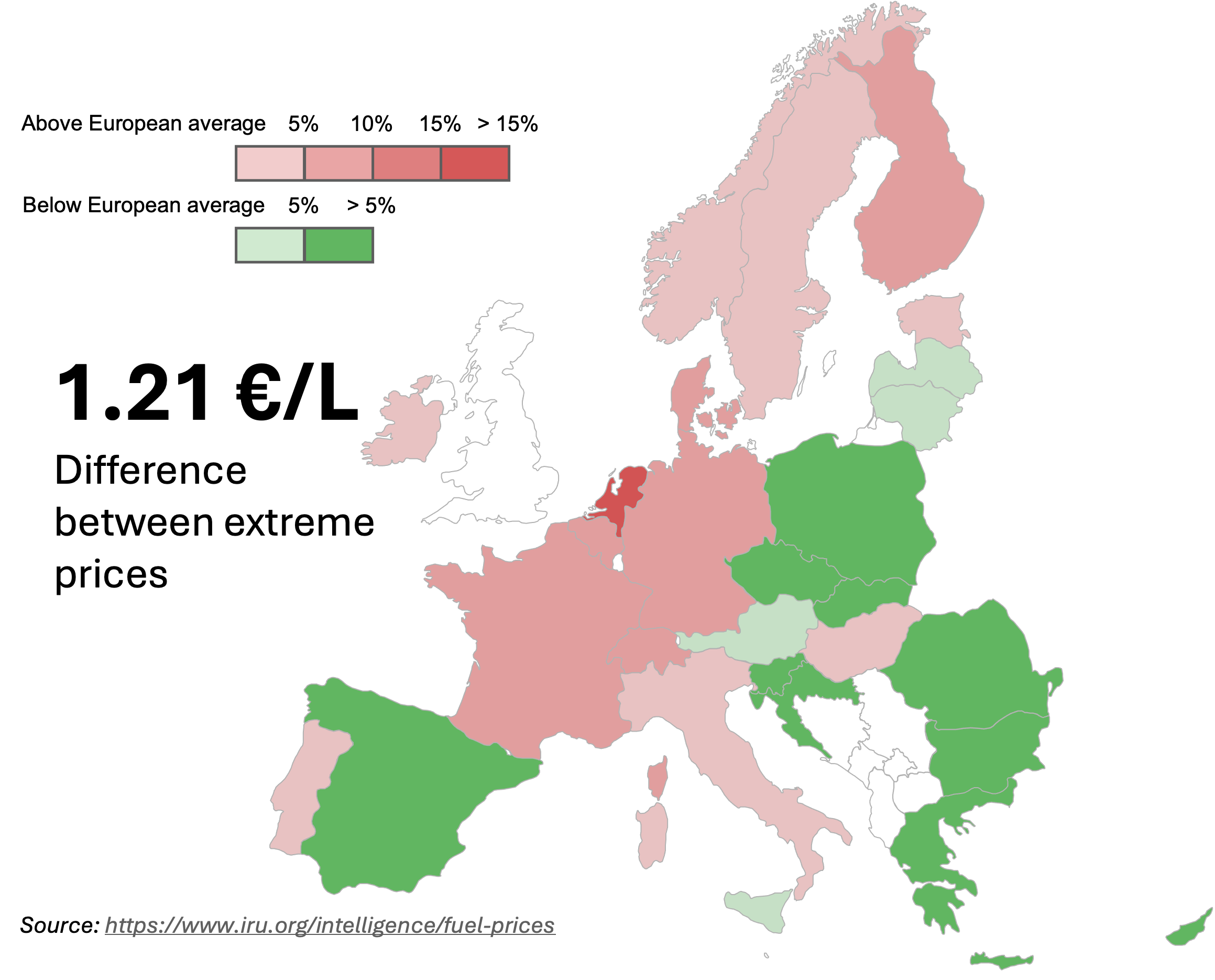

EU retail diesel averaged EUR 2.1 per litre on 16 April, up 27% cumulatively since the start of the war. Week on week, the EU average price eased slightly, falling 4.6%.

The Netherlands leads the expensive cluster at EUR 2.416 per litre (up 24% in local currency), followed by Finland at EUR 2.295 (+31%), Denmark at EUR 2.291 (+23%), France at EUR 2.287 (+34%), and Germany at EUR 2.214 (+27%). Excluding Malta, the lowest EU pump prices are in Poland at EUR 1.718 per litre (+21% in PLN) and Bulgaria at EUR 1.748 (+36%).

Announcements of new and revised national measures have increased sharply in the EU.

Germany approved a two-month fuel tax cut of EUR 0.17 per litre on 13 April as part of a EUR 1.6 billion relief package, alongside a "no more than one retail price increase per day" rule in force since 1 April and a 19.7 million-barrel crude stockpile release.

In France, IRU member TotalEnergies has activated a voluntary price cap at EUR 2.25 per litre. France also released 14.5 million barrels from strategic reserves and announced EUR 70 million in support for SMEs for April 2026.

Since 7 April, several additional EU countries have escalated their responses:

- Croatia activated a price cap with a margin cap for distributors (7–20 April), though it does not apply to highway stations

- Czechia cut excise duty to the lowest EU-allowable level, released 100,000 tonnes of stockpiled fuel on 8 April, and introduced a daily maximum-price publication by the Ministry of Finance (posted at 14:00 for the following day), with a retail margin cap of approximately CZK 2.50 per litre

- Lithuania activated an excise reduction on 15 April, effective until 15 June

- Sweden is debating an excise reduction with a parliamentary vote expected in April, targeting a 1 May start

However, several EU countries have not activated any fiscal or price-control measures beyond participation in the IEA collective stockpile release. For example, the Netherlands – despite having the highest pump price in the EU (EUR 2.416/L) and the lowest gas storage (6.6%) – has taken no domestic action.

At the EU level, no coordinated fiscal response has been announced. Unlike the 2022 energy crisis, where the European Commission proposed emergency revenue caps and windfall taxes, the current response remains entirely national. This absence of EU-level coordination is particularly striking given that the price spread between cheapest and most expensive EU country has reached EUR 1.21 per litre, creating significant cross-border arbitrage distortions for operators.

AdBlue supply is the secondary pressure. Global urea hit USD 601 per tonne in March, up 35% month on month and 57% year on year. Italian operators already report 20–25% retail AdBlue price rises.

There is no confirmed pan-European shortage yet, but the natural-gas feedstock exposure through Qatar LNG, discussed in the next section, means the risk is elevated through Q2.

While AdBlue accounts for less than 1% of overall TCO, it is mandatory for all diesel trucks. Any shortage would be catastrophic for operators.

Turkish diesel prices rose 17% in Turkish lira, from TRY 61.88 per litre on 27 February to TRY 72.25. Week on week, however, prices fell 7%. The ÖTV sliding-scale excise mechanism – which automatically adjusts excise duty downward when crude rises above a threshold, absorbing roughly 60% of the crude price increase for the consumer – has absorbed most of the pressure so far.

No EU country currently operates an equivalent automatic stabiliser. However, Ministry of Finance headroom is narrowing, and any Q2 revision would flow directly into transport company operating costs given Türkiye’s transit weight in EU–GCC flows.

Chinese diesel reached a 28% increase this week compared to the start of the war, rising from CNY 6.72 per litre to CNY 8.59 per litre on average. China is particularly exposed to the flow of crude passing through the Strait of Hormuz, and US blockage of Iran exports is exposing the country even more. Export restrictions on refined products tightened again in early April as Beijing prioritised domestic supply over state-owned refiner margins.

In India, diesel prices are set by the government, which has held them at their pre-war level through at least mid-April. On the policy side, press reports flag temporary excise reductions, export taxes on refined fuel, and a US Treasury waiver allowing continued Iranian crude imports via the Chabahar transit route – the latter is a material lifeline for Indian refiners.

Brazilian retail diesel reached BRL 7.43 per litre this week, a slight decrease from 7.45 last week but up 23% from BRL 6.08 compared to the 27 February baseline.

The government has maintained the PIS/Cofins tax zero rating on diesel and extended the BRL 0.32-per-litre subsidy, while Petrobras refinery pricing has absorbed part of the crude spike without fully passing through. A 50% diesel export tax remains in force to prioritise domestic supply.

Natural gas

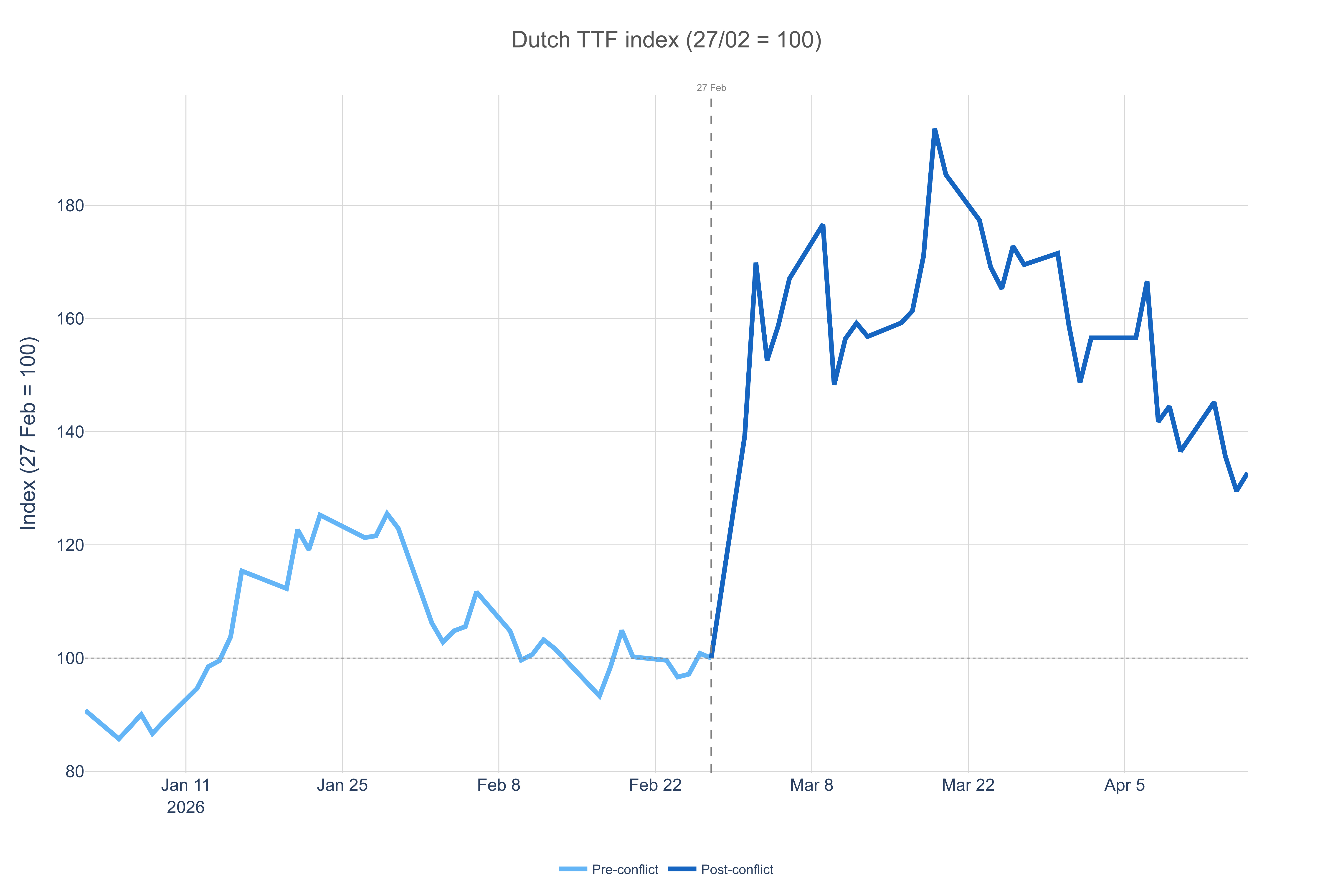

TTF gas reached EUR 42.42 per MWh on 16 April, up 33% from EUR 31.96 on 27 February.

The week was mostly down – prices eased from EUR 45.30 on 8 April, ticked up to EUR 46.17 on 9 April, fell to EUR 43.64 on 10 April after EU gas storage data came in above expectations, climbed again to EUR 46.41 on 13 April as Ras Laffan (Qatar’s main LNG production site) uncertainty resurfaced, then declined through the week to EUR 41.40 on 15 April before settling at EUR 42.42 on 16 April. Week on week, TTF is down 8%, in line with the Brent pattern.

Goldman Sachs has warned that European TTF underprices the disruption risk and could enter a EUR 75–100 per MWh scenario if flows remain suppressed beyond April. ICIS independently flagged 30 April as an internal decision point: if Hormuz is still throttled at month-end, its modelled elevated-price scenario triggers.

EU gas storage sits at 29.6% full, equivalent to approximately 95 days of supply at current draw rates.

That aggregate number hides a sharp national divergence. The Netherlands' gas storage is at 6.6% – the lowest reading in the EU and well below the level at which replenishment typically begins. Sweden follows at 9.9%, Croatia at 17%, Slovakia and Germany are tied at 23%.

These five countries account for a disproportionate share of the injection capacity that Europe will need as summer nears, and the Netherlands figure in particular is consistent with the prolonged shut-ins at the Groningen field rather than import-flow disruption alone.

If Ras Laffan flows do not resume and the Hormuz situation prevents substitution from other Persian Gulf LNG origins, the injection season starts from the worst position in at least five years.

Road transport impact

For European operators, the combination of a 27% diesel price surge, a EUR 1.21 per litre price spread across the EU, emerging AdBlue supply risks, and the absence of EU-level fiscal coordination creates a uniquely challenging operating environment.

Cross-border operators face unpredictable cost differentials depending on where they refuel, while domestic operators in countries without relief measures (notably the Netherlands, Belgium and Finland) absorb the full price impact.

The few measures explicitly targeting commercial road transport, such as Italy’s highway price reduction, remain national exceptions rather than a coordinated framework. With the ceasefire expiring on 21 April and no EU-wide response in sight, operators face continued uncertainty in Q2.

Adding to the pressure, freight-rate dynamics are not keeping pace with fuel prices. Recent diesel increases are not reflected in current rates, according to the latest Upply data and IRU TCO calculations, meaning operators are burning through cash reserves during this crisis.

A significant legislative development came from Spain on 16 April, where the Council of Ministers approved Royal Decree-Law 9/2026.

The decree substantially strengthens operators' ability to pass through fuel cost increases in the invoicing of their transport services. It updates both the calculation formula for the amounts to be passed through and the way this must be applied – making it mandatory, without the possibility of agreeing otherwise – and establishes penalties for non-compliance.

Outlook: what to watch

21 April – US–Iran ceasefire expiry. The two-week term ends with no extension announced as of today

30 April – Italy's decision on extending the March excise cut, and Croatia’s price-cap expiry on highways

3 May – OPEC+ eight-country monthly review. The group will decide whether to roll the 206,000-barrel-a-day May increment into June or pause

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.

IRU members, strategic partners an Intelligence subscribers already have full access to the IRU fuel prices service