As of 10 April 2026, traffic through the Strait of Hormuz remains severely restricted, with only 5–7 vessels transiting daily versus over 100 pre-war. Brent crude reached USD 97.08 a barrel, down 11.5% from last week's peak of USD 119.24 but still 33% above the pre-war baseline. Here is the latest overview for the road transport sector.

- Pump prices up since pre-war: 46% in US, 40% in Türkiye, 33% in EU

- Italy's EUR 0.25 per litre excise extended until 1 May

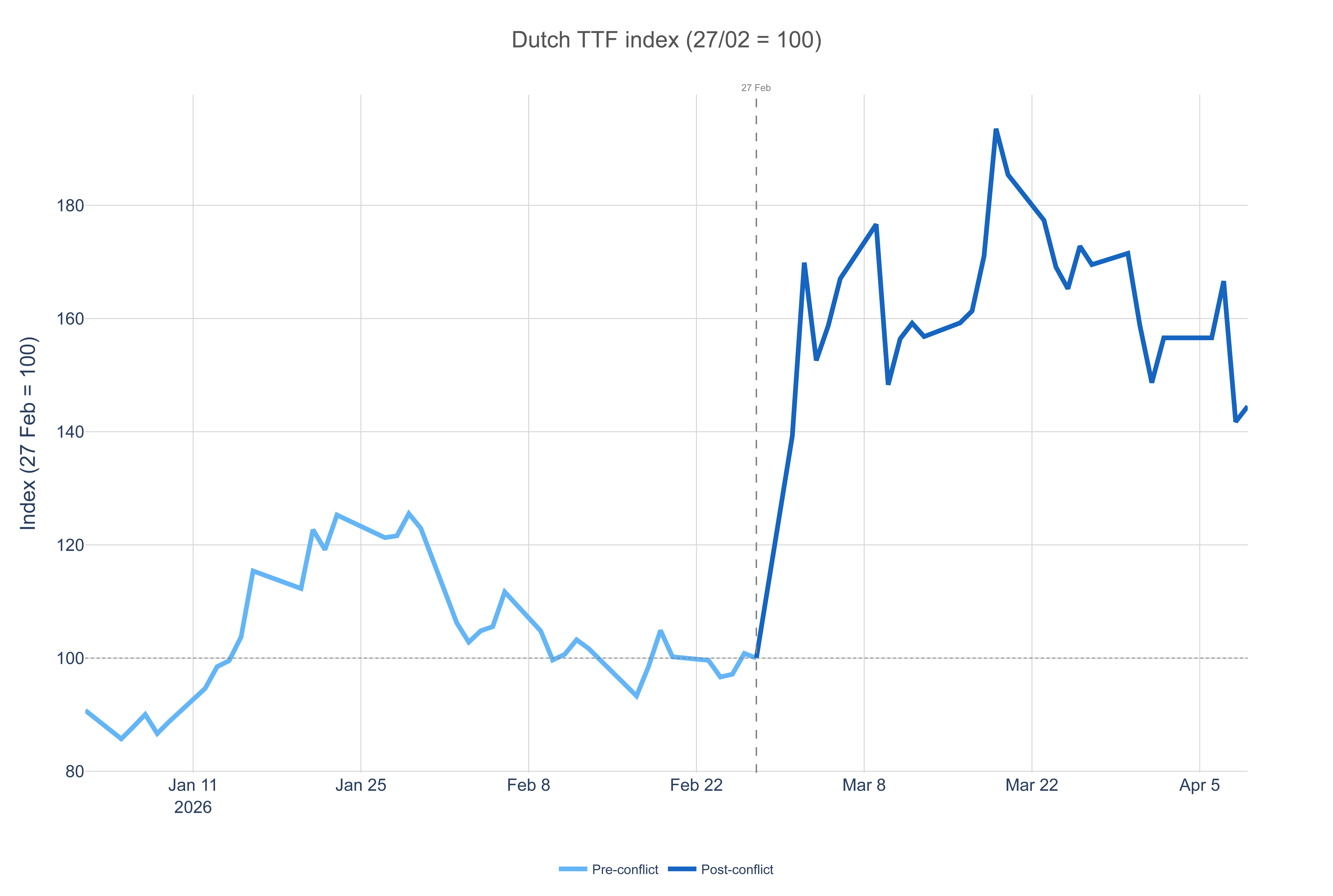

- Dutch TTF natural gas reached EUR 46.17 per MWh on 9 April, up 44.5% from pre-war

- Goldman Sachs cut Q2 Brent forecast to USD 90 a barrel (from USD 99)

Oil markets and supply

Brent crude reached USD 97.08 a barrel on 10 April, up 33% from the pre-war baseline of USD 73 on 27 February.

WTI is at USD 99.09 a barrel (+46.1%). Week on week, both benchmarks dropped sharply – Brent fell 11.5% and WTI 13.0% – reflecting the initial market relief from the 8 April ceasefire announcement.

But that relief was short-lived. The Strait of Hormuz remained severely constrained on 9 April, with traffic limited to a fraction of normal levels rather than fully resuming. Approximately 600 vessels – including 325 tankers – remain stranded in the Persian Gulf. Brent stabilised near USD 97 rather than continuing its decline, signalling that the market is pricing in significant re-escalation risk.

OPEC+ agreed on 5 April to raise production by 206,000 barrels a day in May 2026, using part of the 1.65 million barrels a day it had previously kept off the market. However, this increase is small compared with the roughly 10 million barrels a day of Middle Eastern supply that has been disrupted since the war began.

Analyst forecasts diverge. Goldman Sachs lowered its Q2 2026 Brent forecast to USD 90 a barrel (from USD 99) after ceasefire signals, with Q3 at USD 82 and Q4 at USD 80. JP Morgan is less optimistic, forecasting USD 100 a barrel for Q2 with an overshoot risk towards USD 150 if the strait remains shut past mid-May. The International Energy Agency's March report cut global oil demand growth forecasts to 640,000 barrels a day for 2026, down 210,000 from February.

Pump prices

In the US, diesel reached USD 1.494 per litre on 9 April, a 46.2% increase since 27 February. The Brent–WTI spread has narrowed as both benchmarks fell in tandem on ceasefire news.

Despite relative insulation from domestic production capacity, the US cannot fully decouple from global crude dynamics.

The EU weighted average diesel price reached EUR 2.169 per litre on 10 April, up 32.8% from the EUR 1.634 baseline.

The spread between the cheapest and most expensive markets stands at EUR 1.38 per litre, an indication of how unevenly the crisis is affecting different EU countries.

Most expensive: The Netherlands leads at EUR 2.588 per litre (+32.7%), followed by Denmark (EUR 2.441, +30.6%), Belgium (EUR 2.409, +41.4%), France (EUR 2.386, +39.5%), and Germany (EUR 2.349, +34.7%). Belgium's 41.4% increase is the steepest in the top five.

Cheapest: Malta remains an outlier at EUR 1.21 per litre, unchanged since February, fully absorbed by its regulated price structure. Bulgaria (EUR 1.719, +33.4%) and Poland (EUR 1.81, +26.6%) recorded the cheapest average prices at the pump.

Government measures are accelerating across the Europe. At least 15 countries have activated fiscal interventions:

- Austria cut excise by EUR 0.05 per litre from 1 April until 31 December 2026 and activated a price cap.

- Croatia activated a EUR 0.16 per litre refund from 1 April 2026 and set a temporary price cap at EUR 1.73 per litre.

- Germany introduced a one-price-increase-per-day rule at petrol stations on 1 April (market transparency, not a tax cut). Actual excise cuts, VAT reductions, and a windfall tax remain under discussion.

- Hungary reduced its excise duty to the EU minimum level until 1 May and imposed fuel price caps applicable only to vehicles with Hungarian number plates.

- Ireland has cut its excise duty on diesel by EUR 0.20 per litre until end of May, doubled the fuel allowance to EUR 76 per week, and introduced an operator diesel rebate backdated to January 2026.

- Italy has extended its temporary fuel tax cut by a month until 1 May 2026. Since March, Italy has cut its excise duty by EUR 0.25 per litre and approved a 28% diesel tax credit for truckers.

- Poland reduced its fuel VAT from 23% to 8% and cut its diesel excise to the EU minimum of EUR 0.33 per litre and implemented a maximum price cap on diesel at PLN 6.16 per litre.

- Portugal cancelled its excise refund scheme, eliminating any benefit for transport operators.

- Romania has activated a price cap with a EUR 0.17 per litre reduction mechanism.

- Slovakia has activated a price cap at EUR 1.826 per litre.

- Slovenia imposed a retail diesel price cap at EUR 1.528 per litre on 10 March, creating a gap of approximately EUR 0.50 below Italy and EUR 0.30 below Germany.

- Spain cut its diesel VAT rate from 21% to 10% and introduced a EUR 0.20 per litre transport subsidy via a fuel card, effective from 22 March to 30 June 2026.

Outside the EU, Serbia has cut its excise duty by 61% and released 40,000 tonnes of diesel from its reserves. Albania has cut by 20%, and Montenegro by 50%.

AdBlue supply risk: The Strait of Hormuz blockade threatens 50% of global urea and sulphur exports. IRU member BGL has warned of up to 170% AdBlue price increases, echoing the 2022 crisis when prices surged from EUR 0.35 to over EUR 2.00 per litre. No EU or Member State emergency stockpiling has been announced.

Türkiye saw a 40% increase in diesel prices (in Turkish lira) since the beginning of the war. The ÖTV sliding-scale excise mechanism has absorbed a portion of the increase, but its fiscal capacity is approaching its limits, with Brent sustaining above USD 90 a barrel.

In China, diesel prices have risen by 25% since the start of the war.

China ordered its top oil refiners to immediately suspend diesel, gasoline and jet fuel exports in early March to protect domestic supply. This was followed by repeated government interventions to limit the pass-through of higher crude prices to consumers.

On 7 April, China again raised retail gasoline and diesel prices, but it capped the increase at roughly half the level implied by its pricing mechanism. However, these measures have only moderated rather than contained the rise, with prices continuing to trend upwards. China imports around 57% of its crude oil from the Middle East, leaving it highly exposed to disruption in the Strait of Hormuz.

In India, diesel prices have risen by 5% since the start of the war, among the lowest of any major economy.

On 27 March, the government took further action, eliminating the central excise duty on diesel entirely and imposing export taxes on diesel and jet fuel to lock supply into the domestic market. India also benefits from Iran's policy of allowing "friendly nations" to transit the Strait of Hormuz. The combination of these measures means that India's pump prices have been substantially contained.

In Brazil, diesel prices have risen by 24% since the war started, reaching BRL 7.45 per litre (USD 1.44). The government's 12 March package zeroed PIS/Cofins import taxes on diesel, created a BRL 0.32 per litre subsidy until 31 December 2026, and imposed a 50% export tax on diesel.

The initial impact was undermined when Petrobras raised diesel prices by BRL 0.38 per litre. However, the situation has since shifted significantly as Petrobras is now pricing diesel at the refinery gate at 63% below import levels, aligning with government pressure to contain prices.

Brent price dynamics

Brent crude reached USD 97 a barrel on 10 April, up 33% from the pre-war baseline of USD 73 on 27 February. The intra-war peak of USD 119.24 was recorded on 31 March.

The week's price action was dramatic. Brent reached USD 119.24 on 31 March before plunging to USD 105.94 on 1 April as ceasefire signals first emerged. Prices recovered to USD 109.74 on 2 April, then climbed to USD 111.80 on 7 April before the ceasefire announcement sent Brent down to USD 97.22 on 8 April. A brief recovery to USD 99.50 on 9 April followed Iran's re-closure of the Strait of Hormuz, before settling at USD 97.08 on 10 April. The USD 22.16 range between the 31 March high and the 8 April low is the widest intra-war swing to date.

Natural gas

Dutch TTF natural gas reached EUR 46.17 per MWh on 9 April, up 44.5% from the pre-war baseline of EUR 31.96.

Week on week, TTF fell 7.7% from its recent peak. Prices held steady on 6 April, spiked to EUR 53.25 on 7 April as Strait of Hormuz tensions peaked, then dropped sharply to EUR 45.30 on 8 April on the ceasefire announcement before recovering slightly to EUR 46.17 on 9 April.

Qatar's Ras Laffan LNG facility, the world's largest, remains under force majeure. According to Reuters, approximately 17% of Qatar's LNG capacity is offline. It is estimated that the damage could take 3–5 years to repair.

LNG cargoes are being diverted to Asia as higher Asian prices outbid Europe, with realistic alternative supply totalling less than 2 million tonnes a month against a 5.8 million tonne monthly loss.

EU gas storage stands at 28.9% full. The five lowest-fill countries are the Netherlands (5.5%), Sweden (9.9%), Croatia (16.0%), Germany (23.0%) and Slovakia (23.2%).

Goldman Sachs warned on 6 April that Europe is under-pricing Strait of Hormuz disruption risk. If the supply shock persists beyond April, TTF could test EUR 75–100 per MWh. The Q2 gas storage refill season is now open, and failure to source LNG cargoes could push prices towards that scenario

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.