As of 5 March 2026, global oil and fuel prices are trending upwards, driven by geopolitical tensions and supply disruptions in the Middle East. Here is an overview.

The ongoing conflict has affected fuel prices through oil supply disruptions in the Middle East, particularly around the Strait of Hormuz.

As gasoline and diesel prices follow global crude prices, pump prices have been impacted.

We first look at the impact of diesel prices at the pump, before turning to wholesale energy dynamics, including Brent and LNG trends.

Prices at the pumps

Fuel prices have risen globally since the start of the conflict. Asia and Europe faced the first pump-price pressure, while the US is more insulated thanks to domestic oil production. Even if Europe does not buy much oil directly from Iran, it still pays the global market price as global energy markets are under stress.

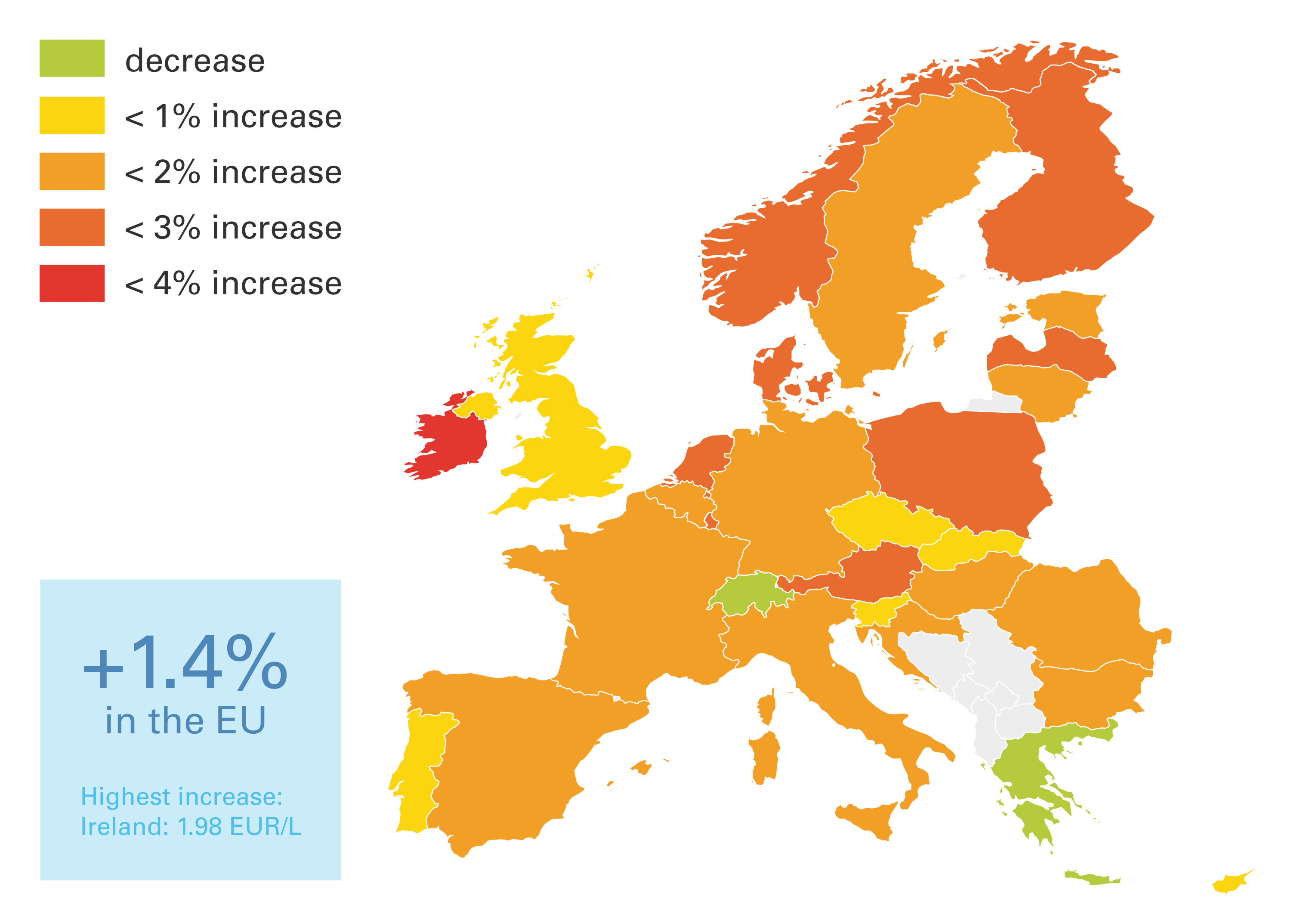

The trend at European pumps since 27 February 2026 has been upwards, with the strongest increase observed in Ireland (3%, reaching EUR 1.98 per litre). However, diesel prices at the pump remain volatile in some countries, notably Germany.

Pump prices rise by EUR 5–15 cents/litre as refineries pass on costs.

Early fuel price trends Europe

Source: https://www.iru.org/intelligence/fuel-prices

With excise duties averaging EUR 0.45 per litre in the EU, diesel prices at the pump could increase by 8% next week (average EU, cumulative) if Brent stays around USD 85 per barrel.

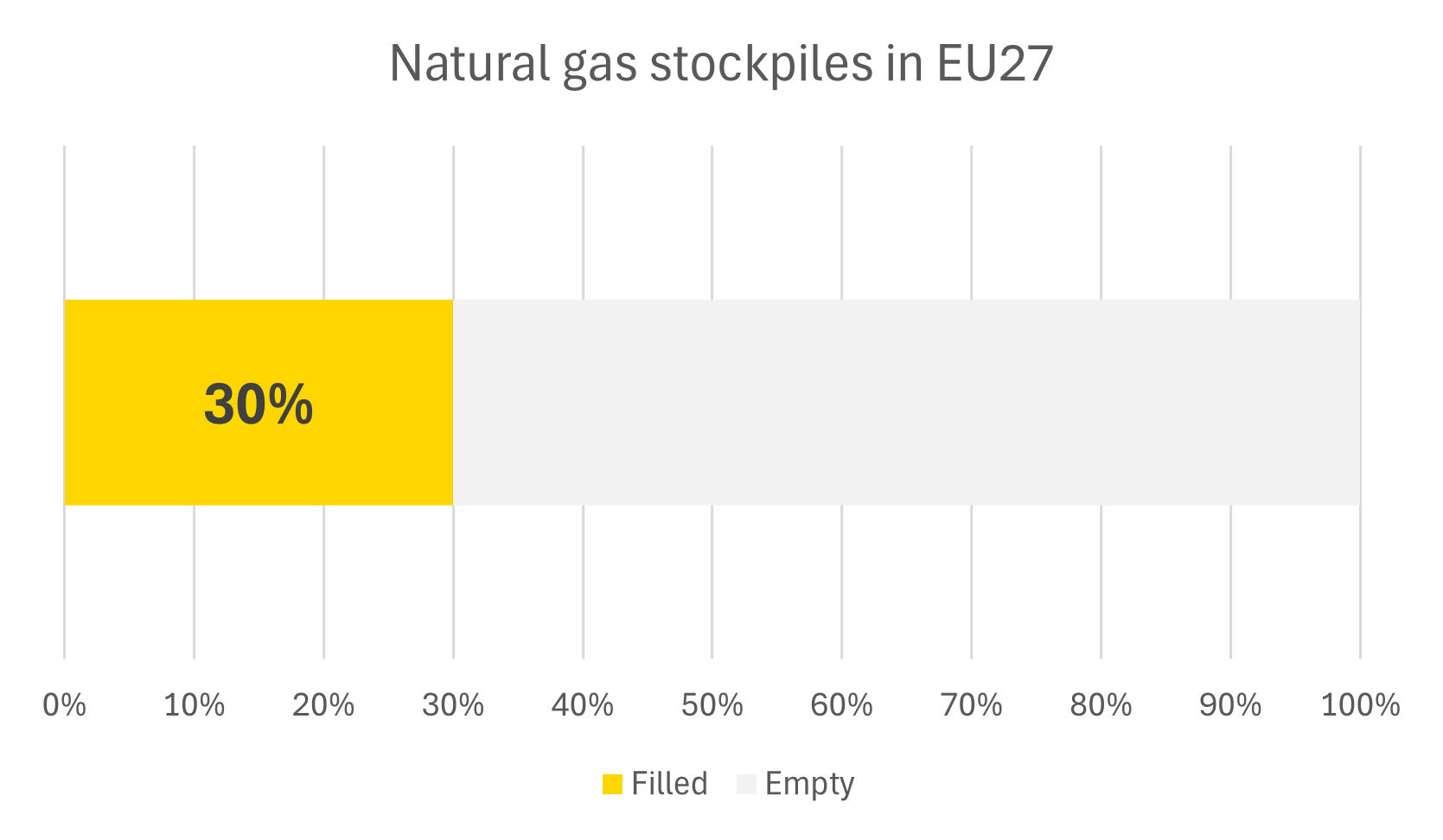

Latest stockpiles data on oil in the EU show 90 days of reserve (late 2025). These stockpiles are a strategic reserve helping mitigate the impact of supply disruptions.

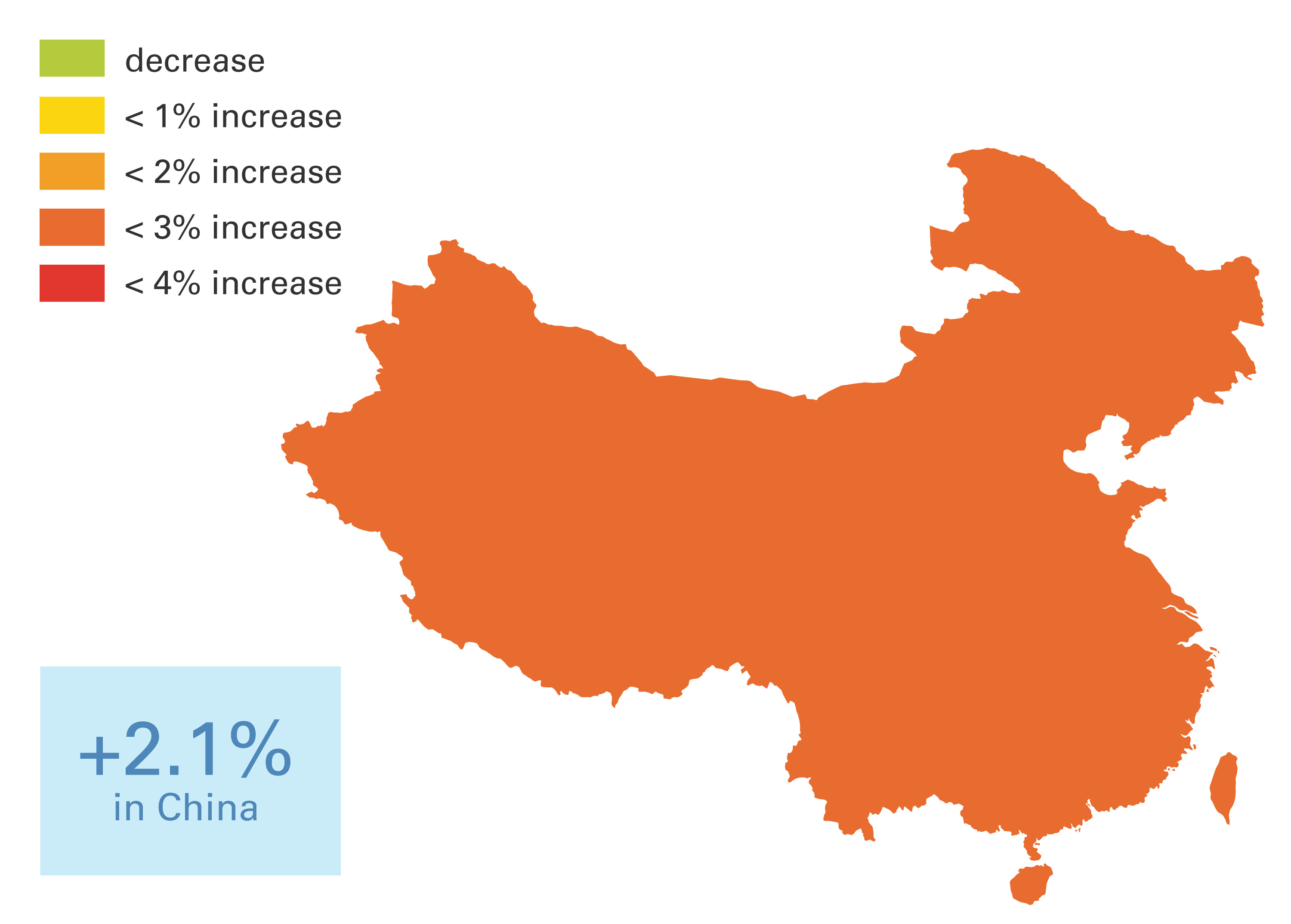

In China, fuel prices are partly controlled by the government.

Consequently, wholesale prices jumped quickly (10% increase since 27 February), but pump prices increased more slowly.

Average diesel prices at the pump are starting to rise by 2.1% to date and further increases are expected if the Strait of Hormuz remains impractical for fuel tankers.

China is actively trying to limit domestic pump price spikes:

- Authorities have asked major refiners to suspend exports of diesel and gasoline to keep more fuel in the domestic market

- Retail fuel prices in China are adjusted by the government based on international crude movements, rather than purely market pricing

This means price increases at the pump usually happen gradually, with changes after official adjustments rather than continuously like in Europe.

Fuel price trends in China

Source: https://www.iru.org/intelligence/fuel-prices

Summary of impact at the pump

| Region | Early pump price reaction | Drivers | |

| US | Low-moderate | - | Large domestic oil Production limiting the impact |

| Europe | Moderate-High | Immediate rise (few cents/litre already) | High dependence on imported oil and LNG via global market |

| China | Moderate | Stepwise increases | Government-controlled retail pricing;authorities delay or smooth adjustments |

| Asia (excl. China) | High | Faster increases than Europe (South Korea, India, Thailand) | Heavy reliance on Persian Gulf shipping routes |

| Middle East | Mixed effect | - | Mostly insulated due to subsidies and domestic supply |

Brent price dynamics

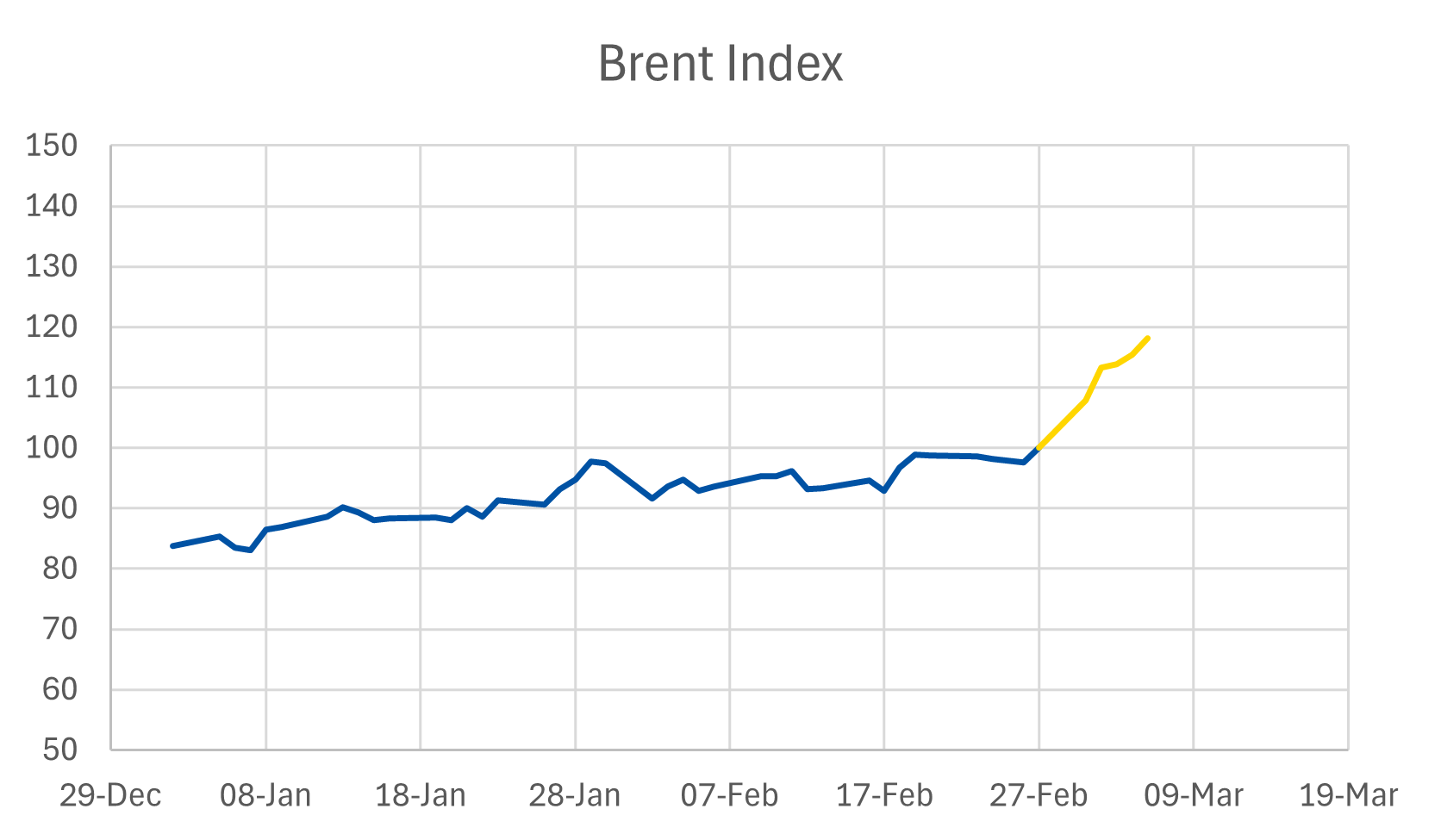

The conflict in the Middle East has pushed Brent from roughly USD 70 per barrel on 27 February to USD 85 per barrel on 5 March, representing a 15% increase.

Markets are pricing in the risk of supply disruptions in the Middle East, particularly through the Strait of Hormuz. The next move in oil prices will depend almost entirely on whether shipping through that corridor normalises or worsens.

On 5 March 2026, Brent rose by about 3–4% in a day to USD 85 per barrel.

Why Brent is rising

Strait of Hormuz disruption

Around 20% of global oil supply normally passes through this route

Tanker attacks and shipping suspensions have stranded hundreds of vessels

Supply risks

Potential loss of several million barrels per day from GCC exporters

Energy infrastructure

Strikes on oil facilities and tankers have amplified market risks

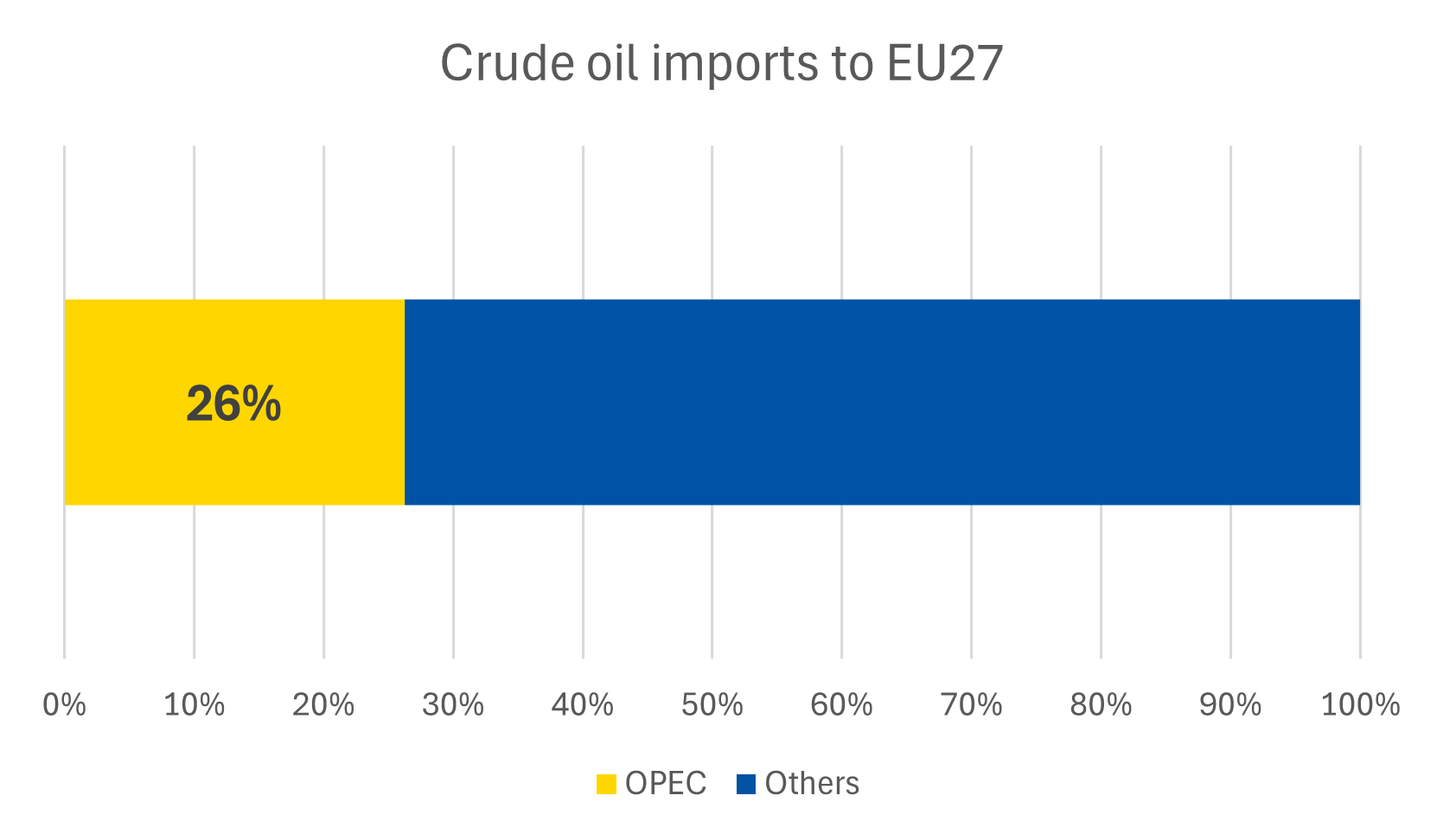

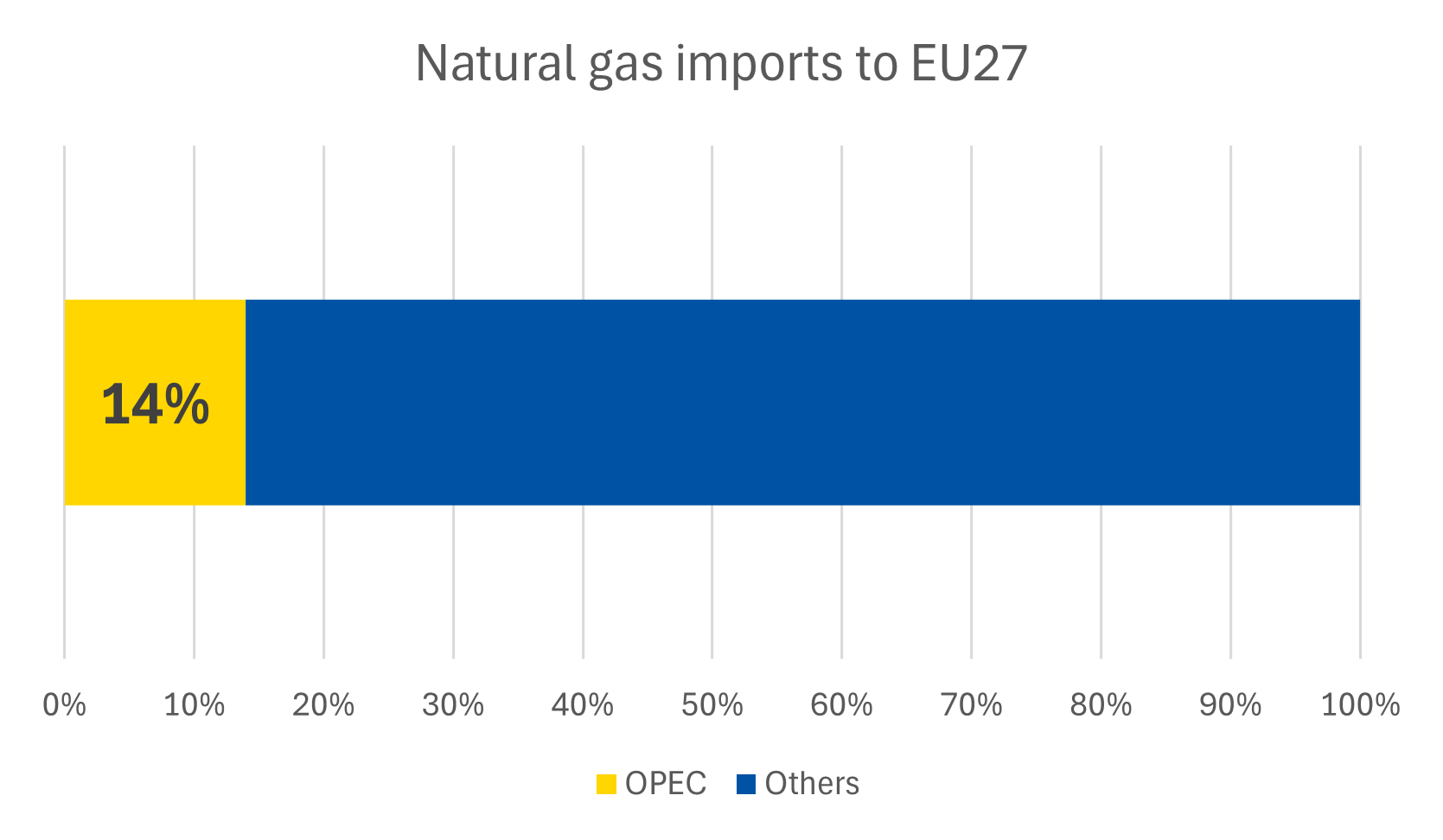

OPEC countries supply 26% of the crude oil consumed in the EU and 15% of its road diesel. Due to limitations along the Strait of Hormuz, most OPEC production cannot be exported, significantly affecting Asian countries and, to a lesser extent, the EU.

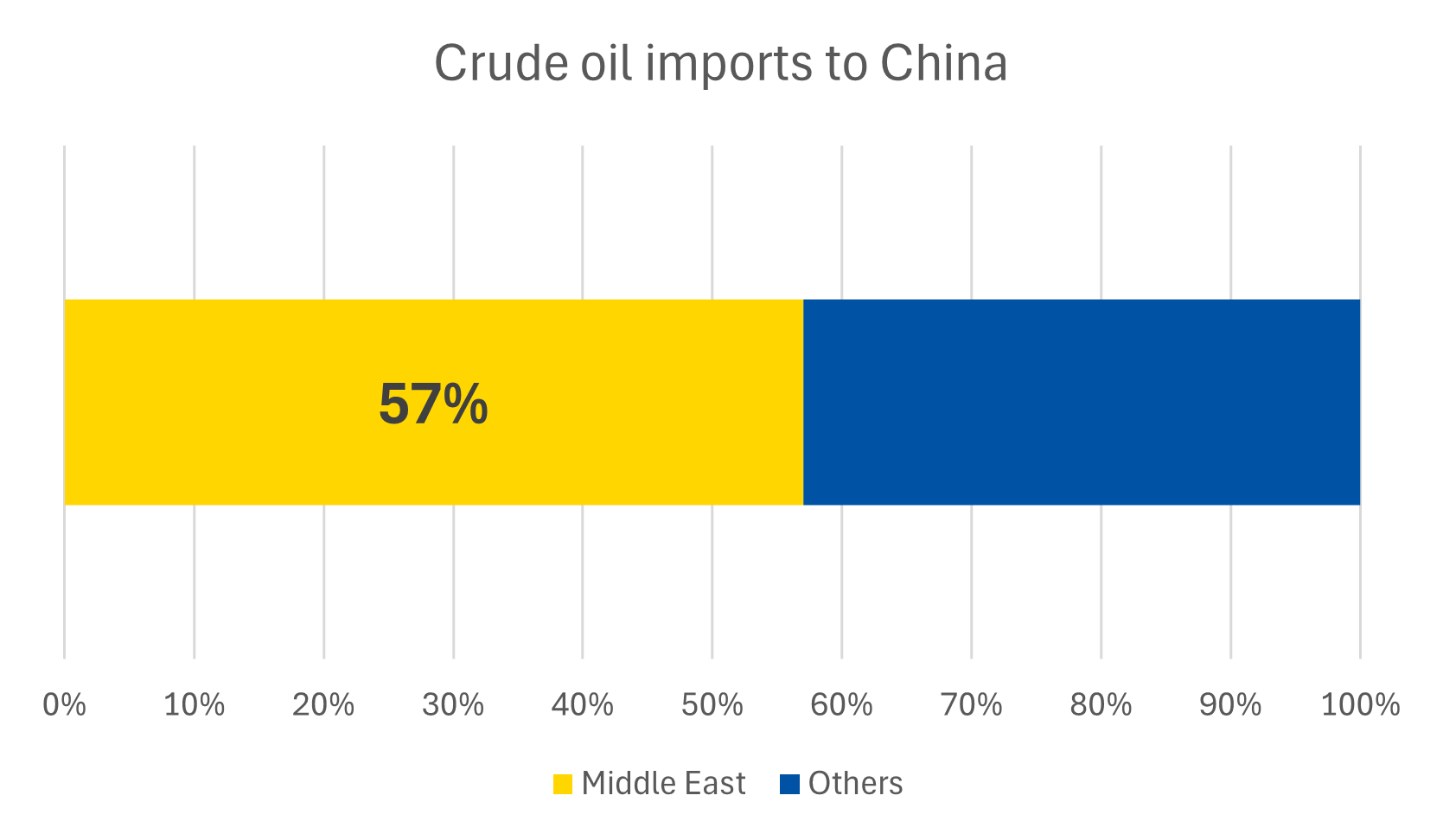

China is increasingly exposed to crude oil supply disruptions, as most of its imports come from the Middle East.

According to Bloomberg, officials from the National Development and Reform Commission have verbally urged refiners to temporarily suspend shipments of refined products with immediate effect.

Refiners were reportedly asked to stop signing new contracts and to negotiate the cancellation of shipments that had already been agreed.

If the situation does not move towards a resolution, Brent could reach USD 100–120 per barrel in the coming weeks, a 40% increase.

Natural gas price dynamics

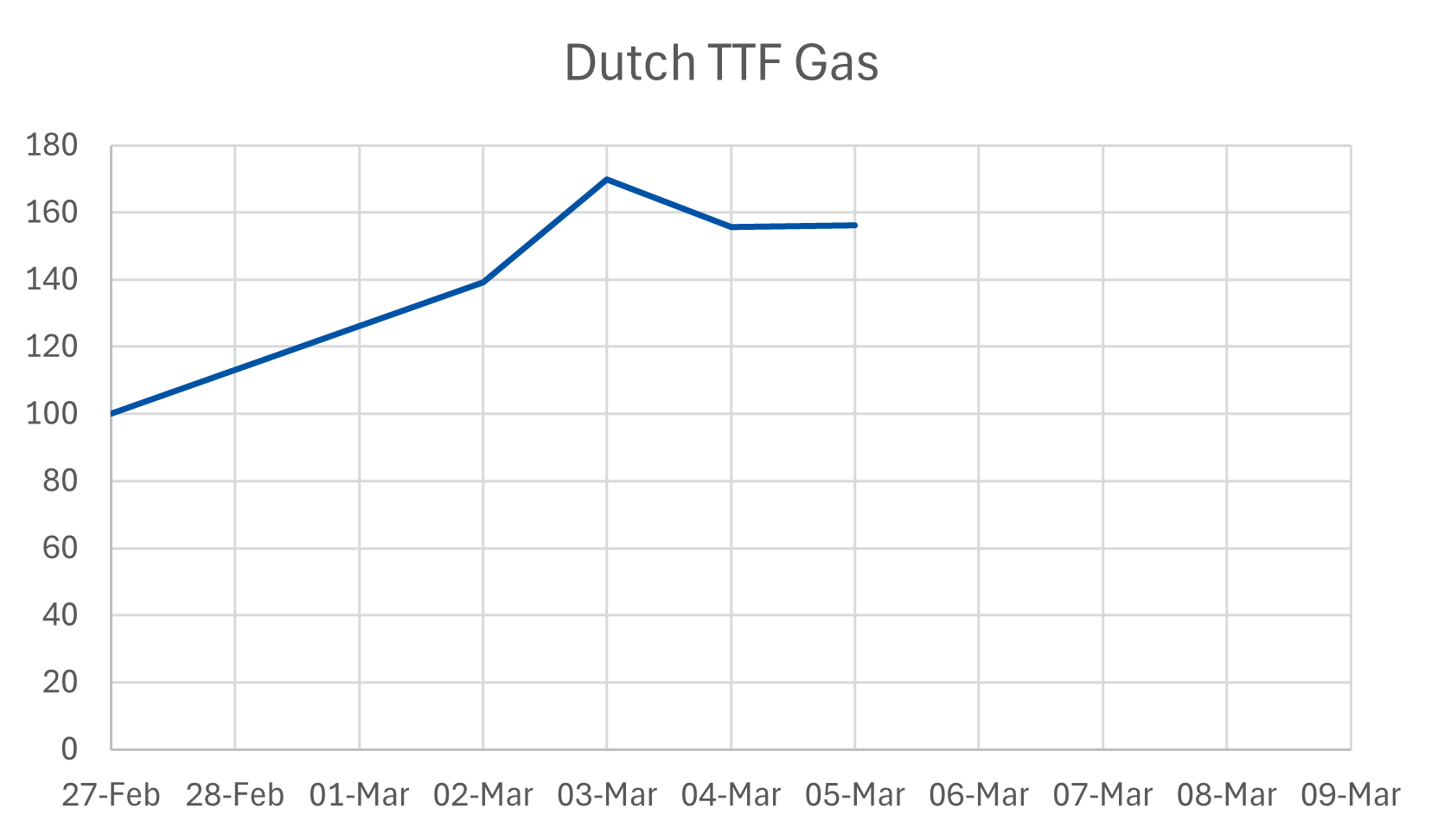

Dutch TTF Gas prices, Europe’s benchmark gas hub, have been strongly affected, mainly through LNG supply risk, shipping chokepoints, and storage dynamics. Below are the key market dynamics shaping Dutch TTF Gas prices.

Since 27 February, prices have increased by 57%, closing at EUR 50 per MWh.

LNG supply

- Around 20% of global LNG trade passes through the Strait of Hormuz

- Disruptions affecting Qatar’s LNG facilities and shipping routes have tightened global gas markets

- Qatar accounts for a major share of global LNG supply. Outages immediately reduce available cargoes

Qatar LNG disruption

A critical recent factor: QatarEnergy’s LNG facilities have halted production, which normally account for around 20% of global LNG output.

Implications for Europe

Qatar supplies a smaller share than the US but is still significant (around 8% of EU imports). OPEC countries supply 14% of natural gas consumed in the EU, mostly from Qatar.

Stockpiles are lower than usual in the EU, averaging 30%, with the Netherlands at 10% and Germany at 20%. Stockpiles will need to be replenished at potentially higher prices, which could have an impact on economic outputs and freight activity.

If the situation does not move towards a resolution, Dutch TTF Gas can potentially rise to EUR 60 per MWh.

Summary of Brent price dynamics

- Pre-conflict: around USD 70 per barrel

- Now (5 March 2026): around USD 85 per barrel

Summary of gas price dynamics

- Increase: around 15–20% spike driven by supply risks and Hormuz disruptions Dutch TTF Gas

- Pre-conflict: around EUR 30–32 per MWh

- Now (5 March 2026): EUR 49–50 per MWh

- Increase: Around 50–60% spike driven by LNG supply risk, potential Strait of Hormuz disruptions, and Qatar LNG outages, combined with low European storage levels and stronger competition with Asia for LNG cargoes

IRU will continue to monitor prices for the industry. Fuel price shifts shrink margins.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.