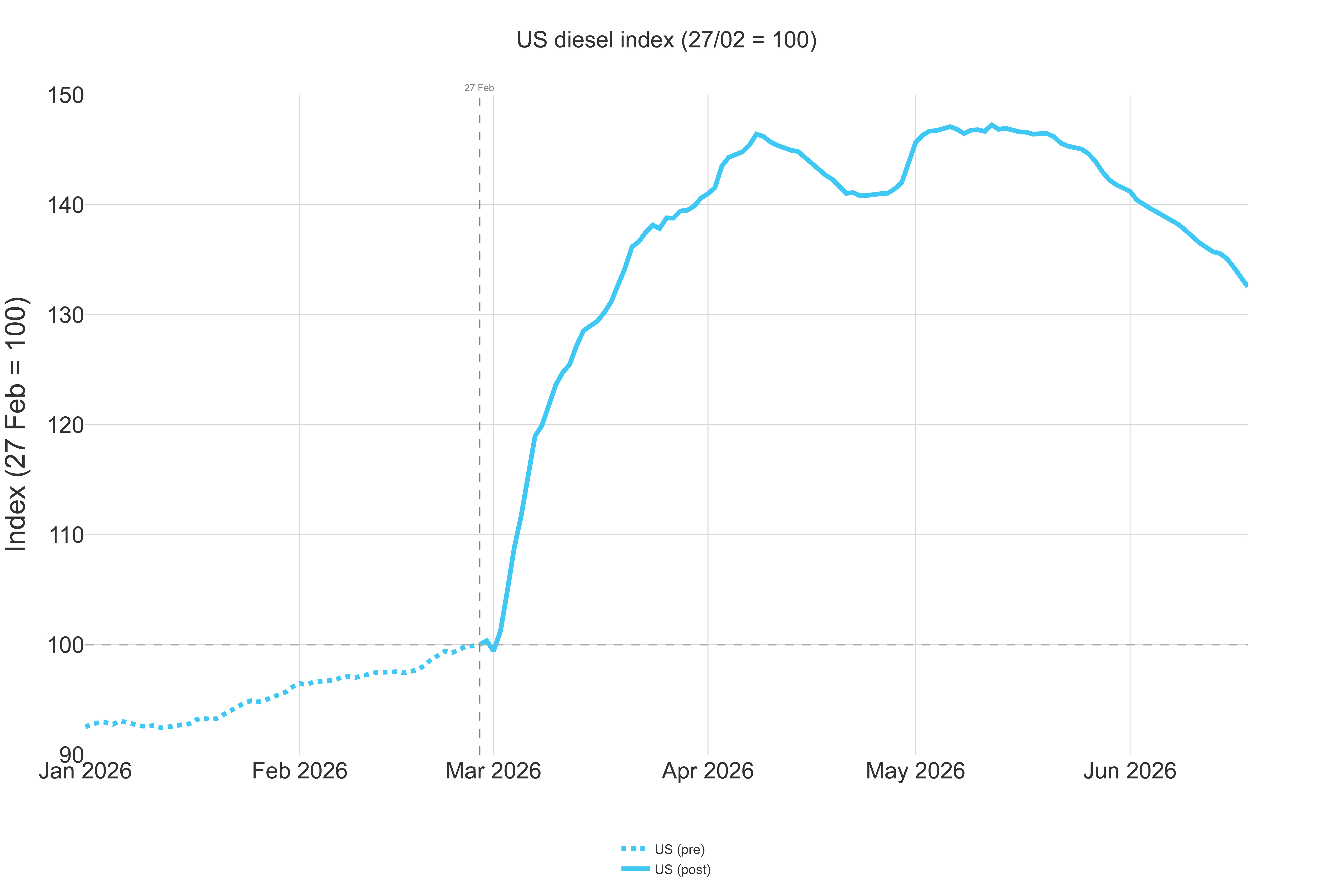

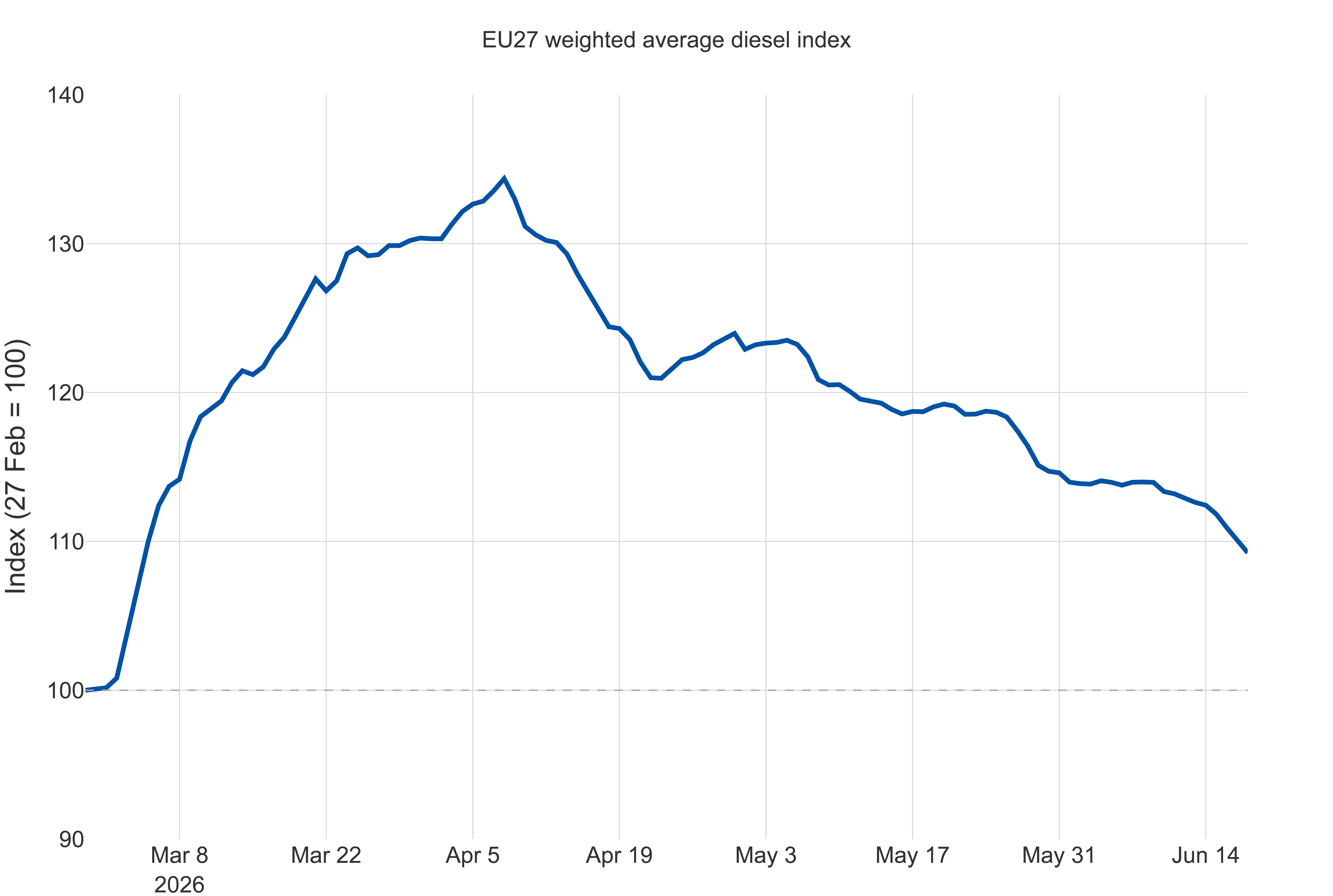

As of 19 June 2026, Brent crude is trading at around USD 80 a barrel, its lowest level since early March. Brent is now broadly flat year on year. At the pump, the relief is starting to show: the EU weighted diesel average has eased to EUR 1.783 a litre, now just 9% above the 27 February baseline. The US average diesel price has fallen to USD 1.354 per litre. Here’s the latest overview for the road transport sector.

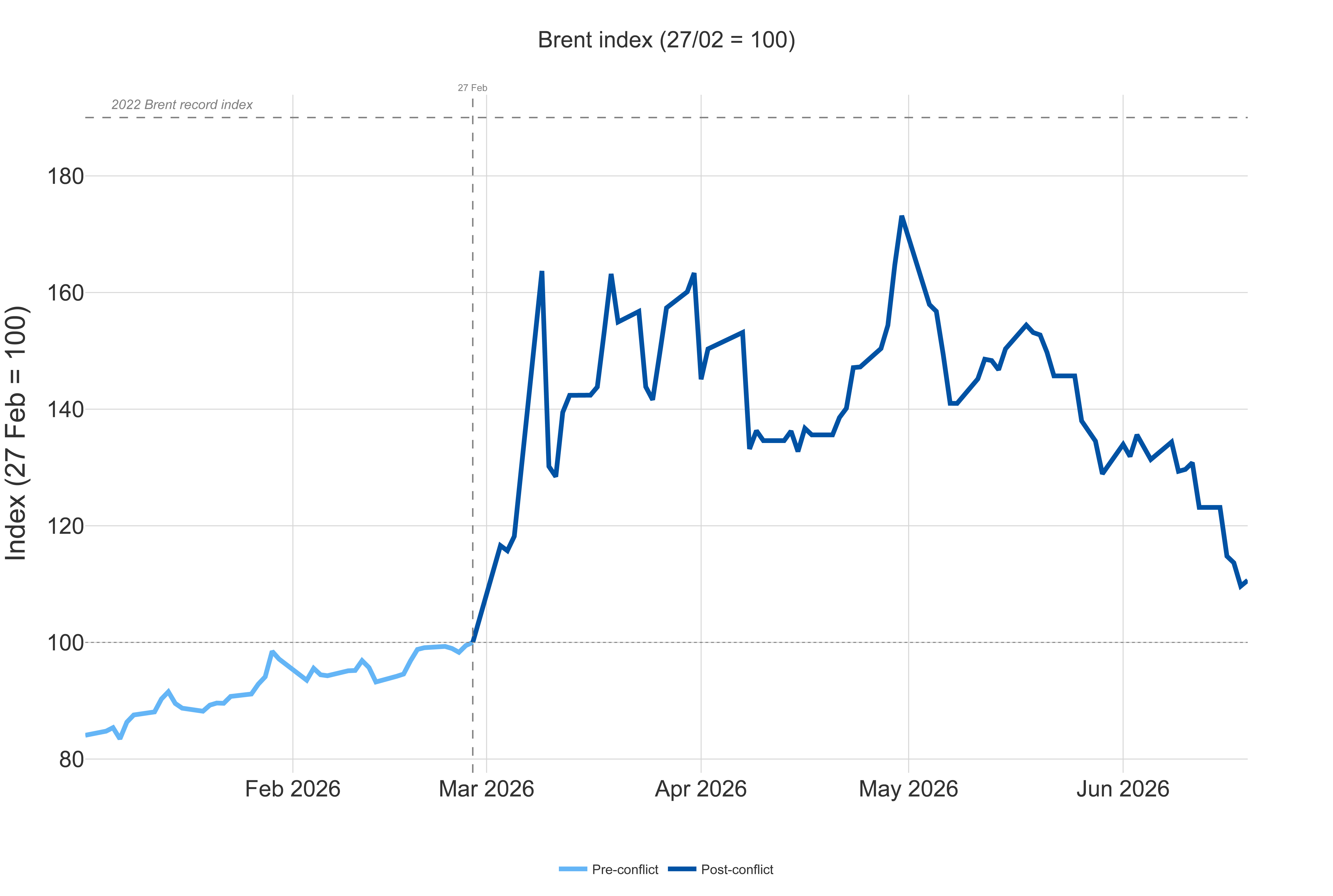

Brent is trading around USD 80 a barrel, a 10% reduction week on week, and sitting now at +11% compared to the 27 February baseline.

Several oil companies and banks argue against reading the sell-off as a return to normal. The chief executives of Chevron and ExxonMobil have told investors that the buffers behind the spring’s relative calm are largely exhausted, and that prices will settle above the pre-war baseline even after a deal, as countries rebuild reserves and the industry absorbs years of repair costs.

A 16 June note from BNP Paribas frames the same tension. In its relatively optimistic scenario, Brent could fall quite rapidly into a USD 70–80 range, as the extra barrels from the Middle East meet demand already weakened by the crisis, especially in Asia, the region most dependent on Middle Eastern crude. But it stresses the relief may be short-lived: the two buffers that have absorbed the market’s roughly 7 million barrels per day net loss since April (an accelerating OECD reserve drawdown and a fall in Chinese imports to a decade low) are not sustainable. BNP expects strategic reserves to reach a critical level during July, with a significant upwards impact on prices.

The International Energy Agency (IEA) expects global oil demand to fall by 1.1 million barrels per day in 2026, with Q2 2026 deliveries decreasing by 5 million barrels per day, when the global baseline is above 105 million barrels per day.

The damage is broad: April and May deliveries fell by 4.6 and 5.4 million barrels per day, respectively, across almost every product and region. China’s apparent demand is set for its first significant annual drop since the oil crises of the 1970s–80s.

On the supply side, May global output of crude was down by 13.6 million barrels per day, a 9% decrease. With 2027 supply growth running at roughly four times projected demand growth, the IEA now sees “a significant overhang emerging next year”, a prospective oversupply that could let countries rebuild depleted inventories or new strategic reserves.

Middle Eastern flows are already recovering, rising from a May low of 9.6 million barrels per day to about 12 million barrels per day in early June, lifted by ship-to-ship transfers off the Omani coast. The UAE said it could restore pre-war production within two weeks. But it warned that even if the war is over, it will not return to full pre-war export levels before the first or second quarter of 2027. The IEA warns that the buffers are not yet rebuilt. Observed global inventories fell by 143 million barrels (−4.6 million barrels per day) in May, accelerating from April and lifting the average draw since the war began to 3.8 million barrels per day.

OECD government stocks have fallen to their lowest level since December 1990 following emergency releases. The agency’s own balance still implies a 2.1 million barrels per day deficit from June to August. Only towards the end of 2026 does it expect the market to tip into surplus. In short, the price has already moved to the “after”, while the physical system is still living in the “during”. WTI is trading around USD 76 a barrel, a USD 4 spread with Brent, indicating that the market remains under pressure despite the recently signed deal.

All signs suggest that the global energy crisis, while showing signs of easing, will have long-term consequences as supply, demand and stock balances are far from pre-war levels. The standard deviation of Brent prices suggests that the current crisis is now worse than the 1990 Gulf crisis and getting closer to the 1979 Iranian revolution. The next 60 days will be critical to reassure the markets on the future stability of the global energy supply.

Pump prices

In the US, diesel has eased to USD 1.354 a litre, up 33% on the 27 February baseline, down from USD 1.43 (+40%) two weeks ago, below the wartime pass-through rate, which the IEA estimated at as much as 51% (the fastest and most complete of any major economy, with no caps or tax cuts to cushion it).

The EU weighted diesel mean eased to EUR 1.783 a litre, down 3.5% on the week and 9% above the 27 February baseline, from EUR 1.863 (+14%) two weeks ago.

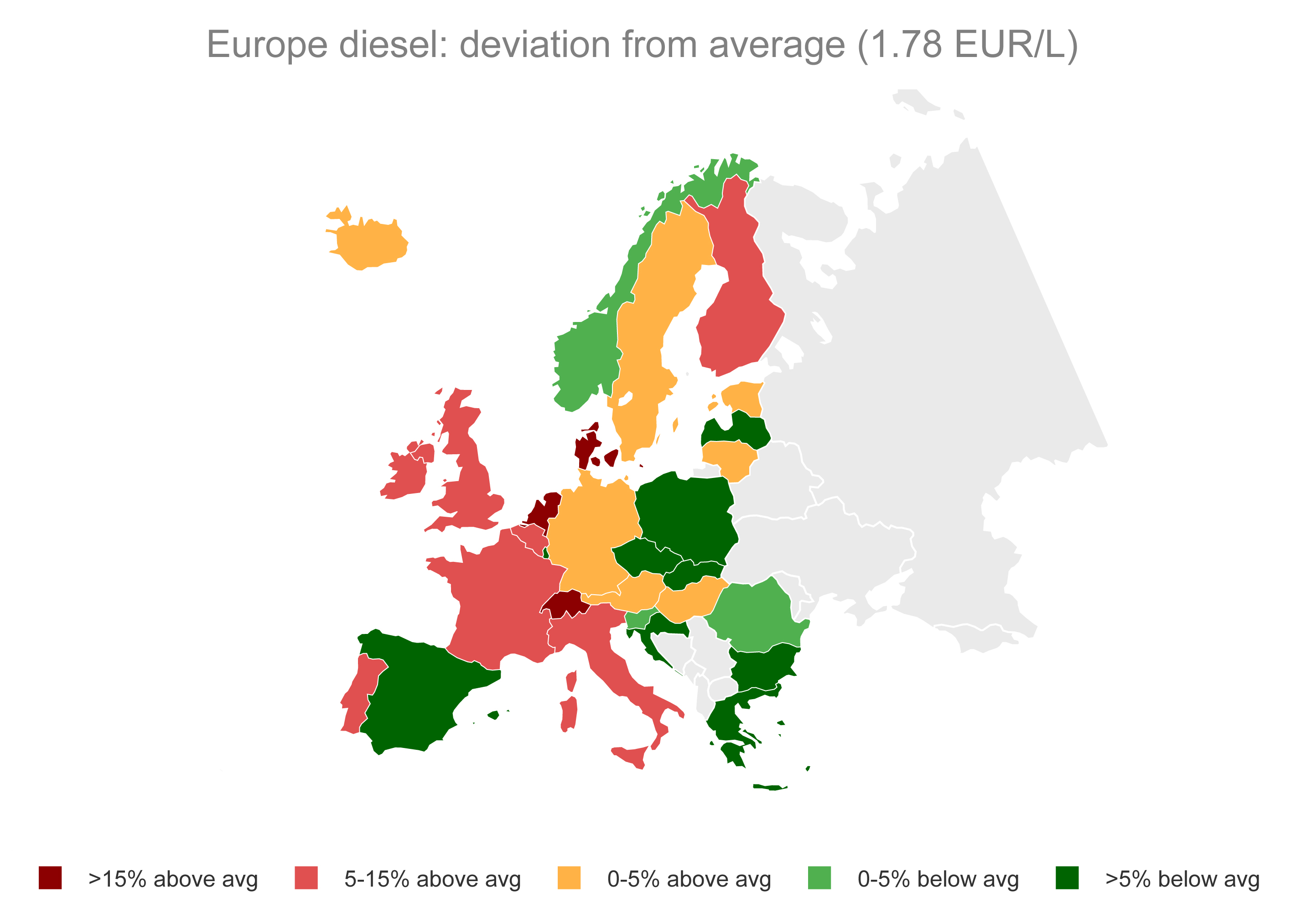

Diesel is most expensive in the Netherlands (EUR 2.109), Denmark (EUR 2.082), Finland (EUR 2.032), Italy (EUR 1.964) and Belgium (EUR 1.962). The lowest price is in Malta, at EUR 1.210 (unchanged), with Poland at EUR 1.466 and Czechia EUR 1.502.

Two readings stand out: Ireland, at EUR 1.878, is now the furthest below its pre-war level (−6.3%), while Bulgaria, at EUR 1.609, still shows the steepest rise in the sample (+24.8%). The spread between the lowest and highest prices has narrowed to about EUR 0.90 but remains historically wide.

In the UK, diesel has eased to about GBP 1.74 a litre, up 23% on the 27 February baseline (from GBP 1.82, +29%, two weeks ago). The GBP 0.05 fuel-duty cut runs to 31 August 2026 with phased restoration thereafter.

Across the major non-OECD markets, pump prices have eased with crude but stay well above baseline.

In China, diesel is around CNY 8.03 a litre (+22%) even as refiners slash runs. Crude imports ran nearly 5 million barrels per day below February, with product exports still suspended and urea-export licensing squeezing the European AdBlue chain.

In India, diesel holds at INR 98.13 (+8%), shielded by discounted barrels and partial excise relief even as LPG rationing spreads.

In Türkiye, diesel is near TRY 66.22 (+7%), its Eşel Mobil mechanism is still absorbing roughly three-quarters of wholesale moves.

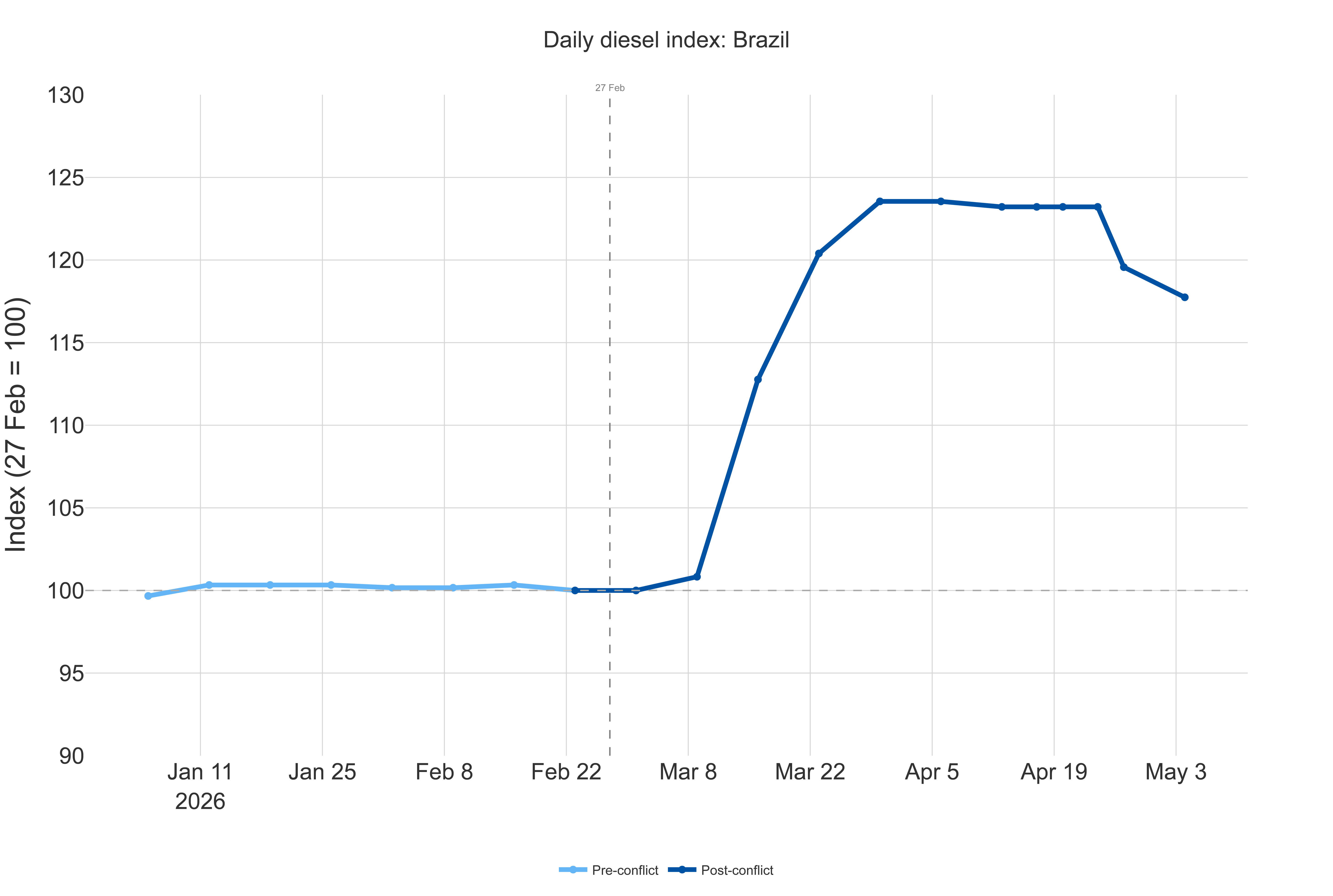

In Brazil, diesel is around BRL 6.81 (+13%) after the timely switch between support schemes, though importers warn of unpaid subsidies.

National measures

For road transport operators, the message on national support is mixed. Diesel prices are easing and the crude sell-off should continue to feed through over the coming weeks. The main risk is shifting from markets to the policy calendar.

Several measures in the “15 June” relief cluster have already lapsed: Poland’s excise cut ended (while 8% VAT and price caps were extended to 30 June), Croatia’s cap cycle expired, and Lithuania’s relief lapsed with legislative amendments still pending. The focus now turns to the 30 June cliff:

- Ending: Germany has confirmed it will not extend the EUR 0.1404 per litre fuel discount, and Spain’s VAT cut is also due to lapse.

- Under review: Australia’s AUD 0.32 excise cut remains subject to weekly review (the RBA signalling it “won’t stand in the way” of an extension).

- Extended/deepened: Latvia has extended its diesel excise relief to 31 December; Sweden has deepened its cut from 1 July; and Austria has agreed to maintain its excise relief.

Where measures fall away, EU pump prices could rise by EUR 0.14–0.20 per litre on 1 July, regardless of what Brent does. Market relief also reaches the pump slowly – fuel prices move “up like a rocket, down like a feather” – so the crude sell-off may take weeks to fully feed through, and months to approach pre-war levels.

Natural gas

Gas has moved lower alongside crude.

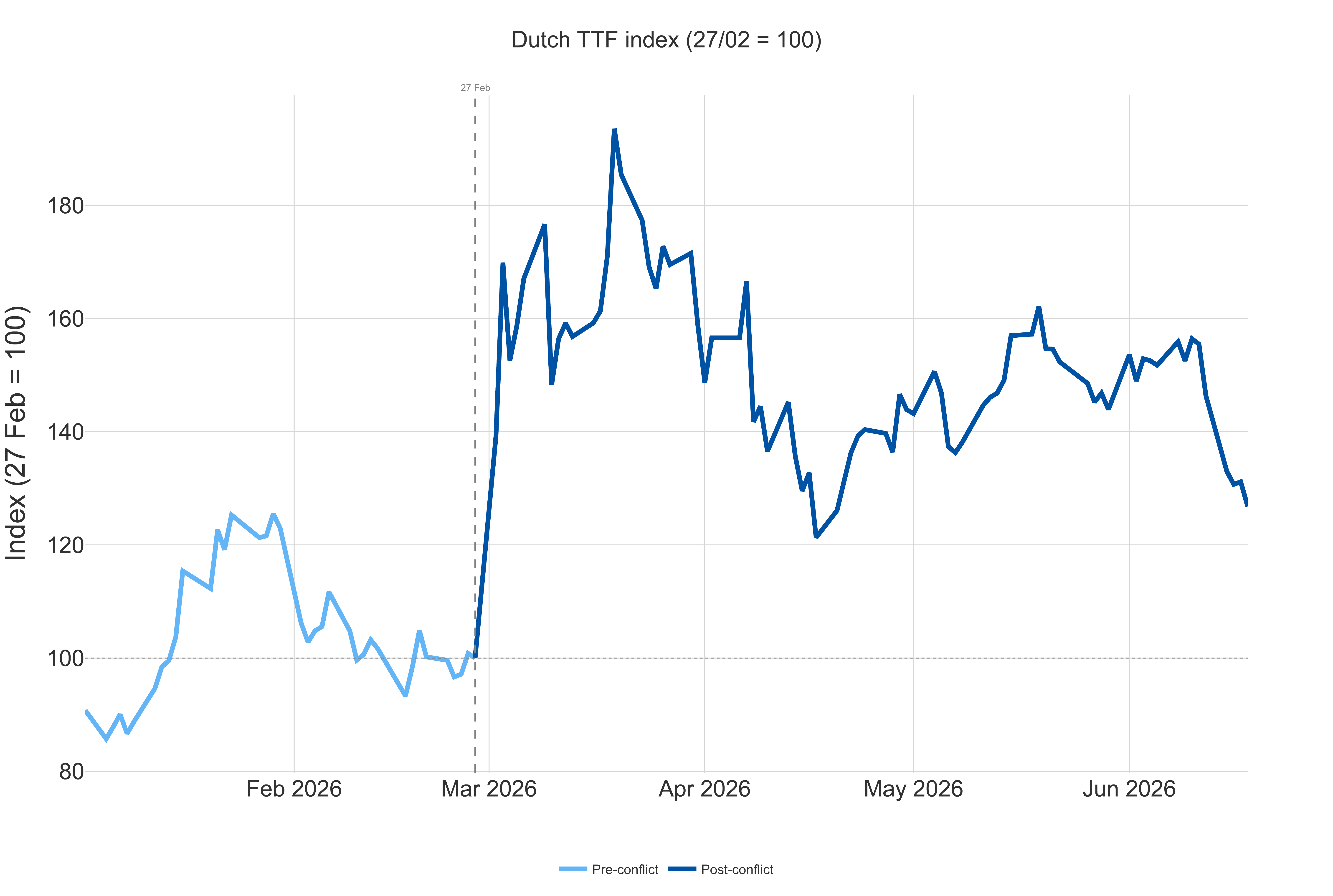

The Dutch TTF benchmark has fallen to around EUR 40.5/MWh (−18% on the week), from EUR 48.75/MWh on 4 June. Two weeks ago, it was the only major energy benchmark still rising despite softer oil prices.

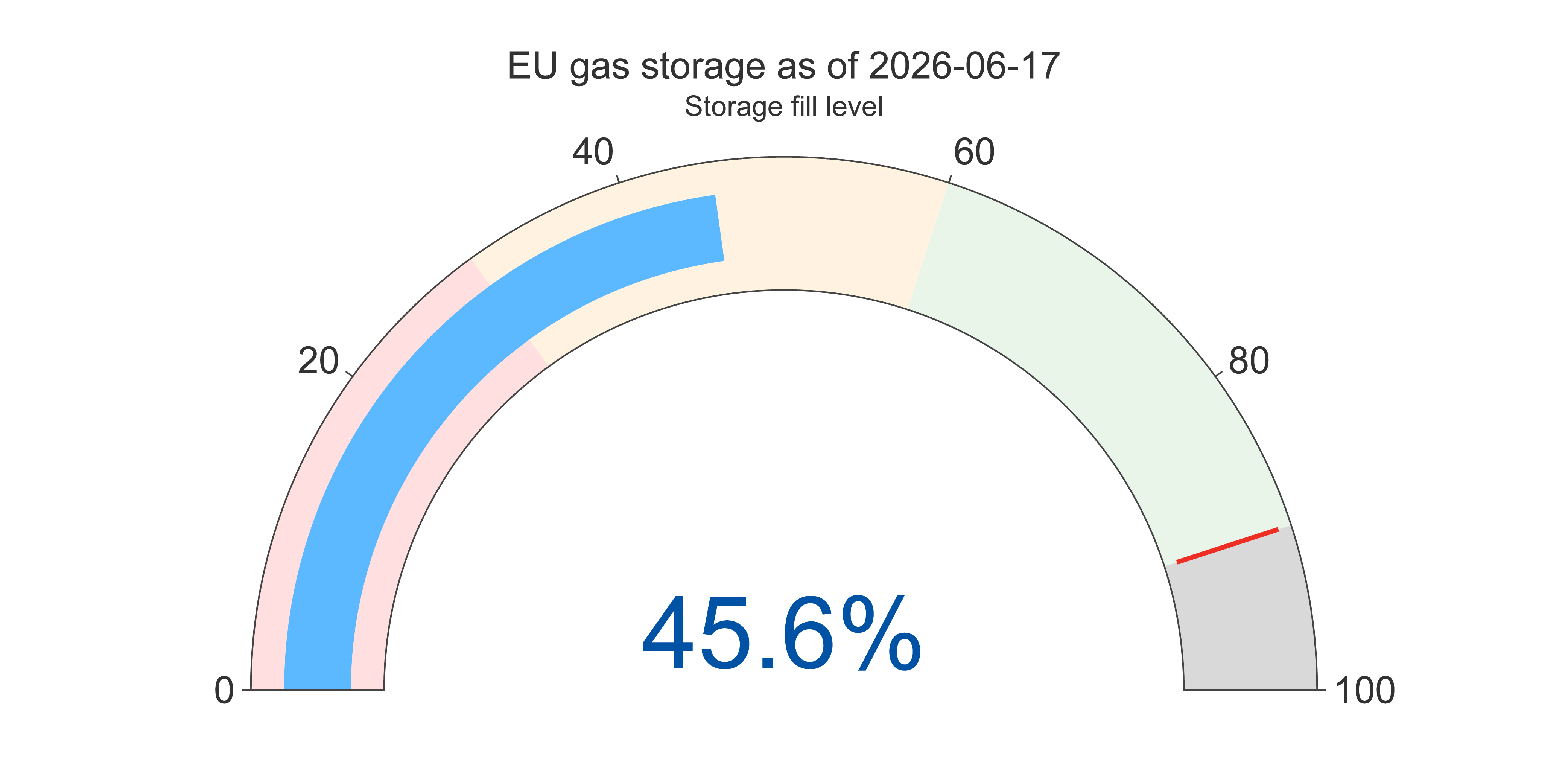

EU storage has increased to 45.6% full (around 54 days’ cover; data as of 17 June) as the injection season progresses (from 41.3% previously). But it remains well below the five-year seasonal norm of roughly 55%.

Injections are also proceeding with the smallest LNG cushion in years. BNP Paribas expects the decline to remain limited despite the deal: the resumption of LNG flows (supported by new US liquefaction capacity) should ease the squeeze, but the lost Qatari capacity is equivalent to about a fifth of global LNG trade.

EU restocking continues to draw on supply; and strong Asian summer demand should cap the downside. Any improvement is also likely to take time to benefit industries and citizens. Asian LNG remains indexed to oil with a three-to-six-month lag, meaning March’s USD 100+ crude is only now feeding through. Elevated gas costs may therefore persist into the autumn, even as spot prices ease.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.

IRU members, strategic partners an Intelligence subscribers already have full access to the IRU fuel prices service.