As of 5 June 2026, Brent crude is trading around USD 95 a barrel, a 3% reduction since 22 May. However, it has seen great volatility since 28 May, trading between USD 91 and USD 99 a barrel. Here is the latest overview for the road transport sector, including pump prices.

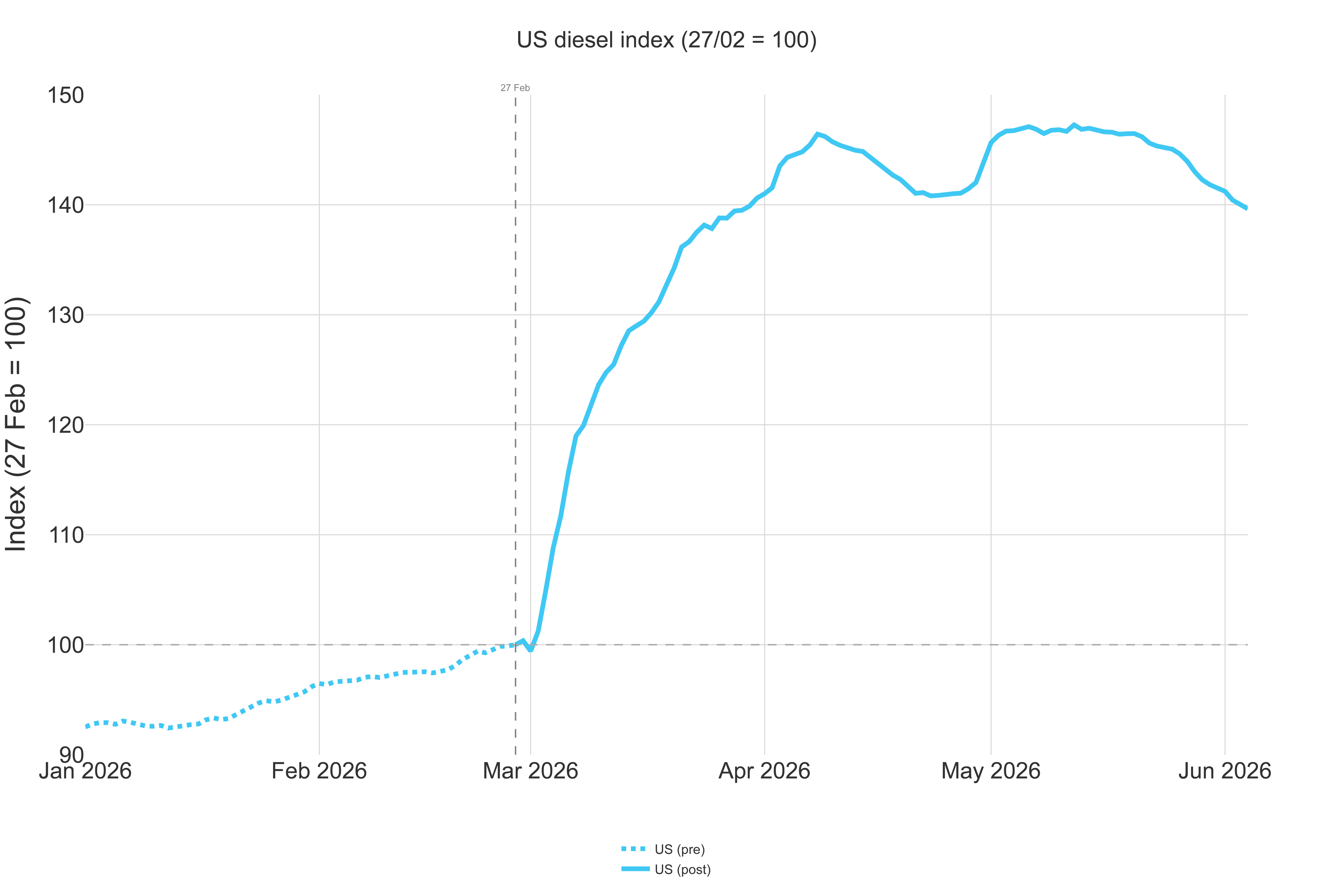

- US diesel reached USD 1.43 per litre, up 40.0% since 27 February but down from USD 1.47 on 22 May

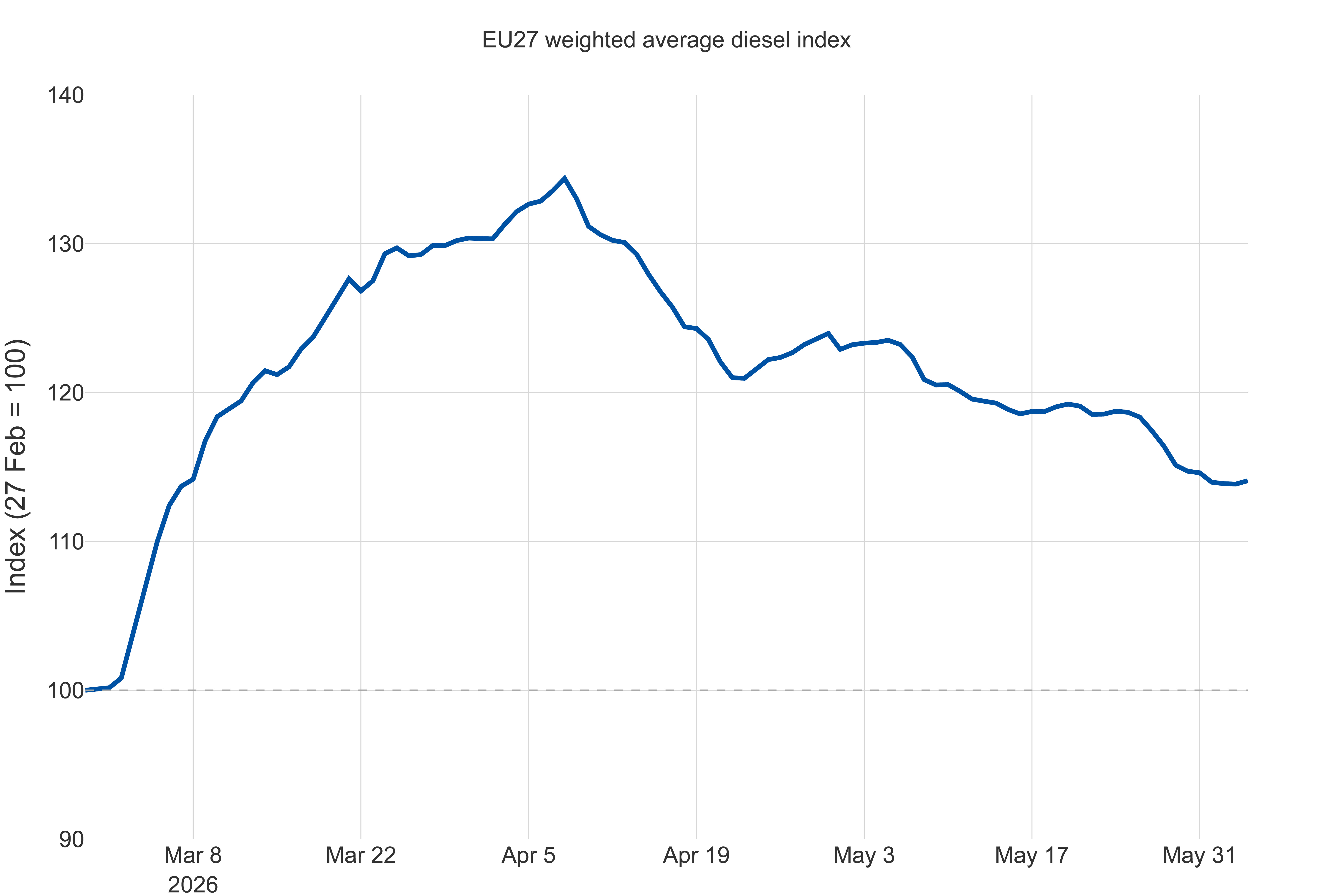

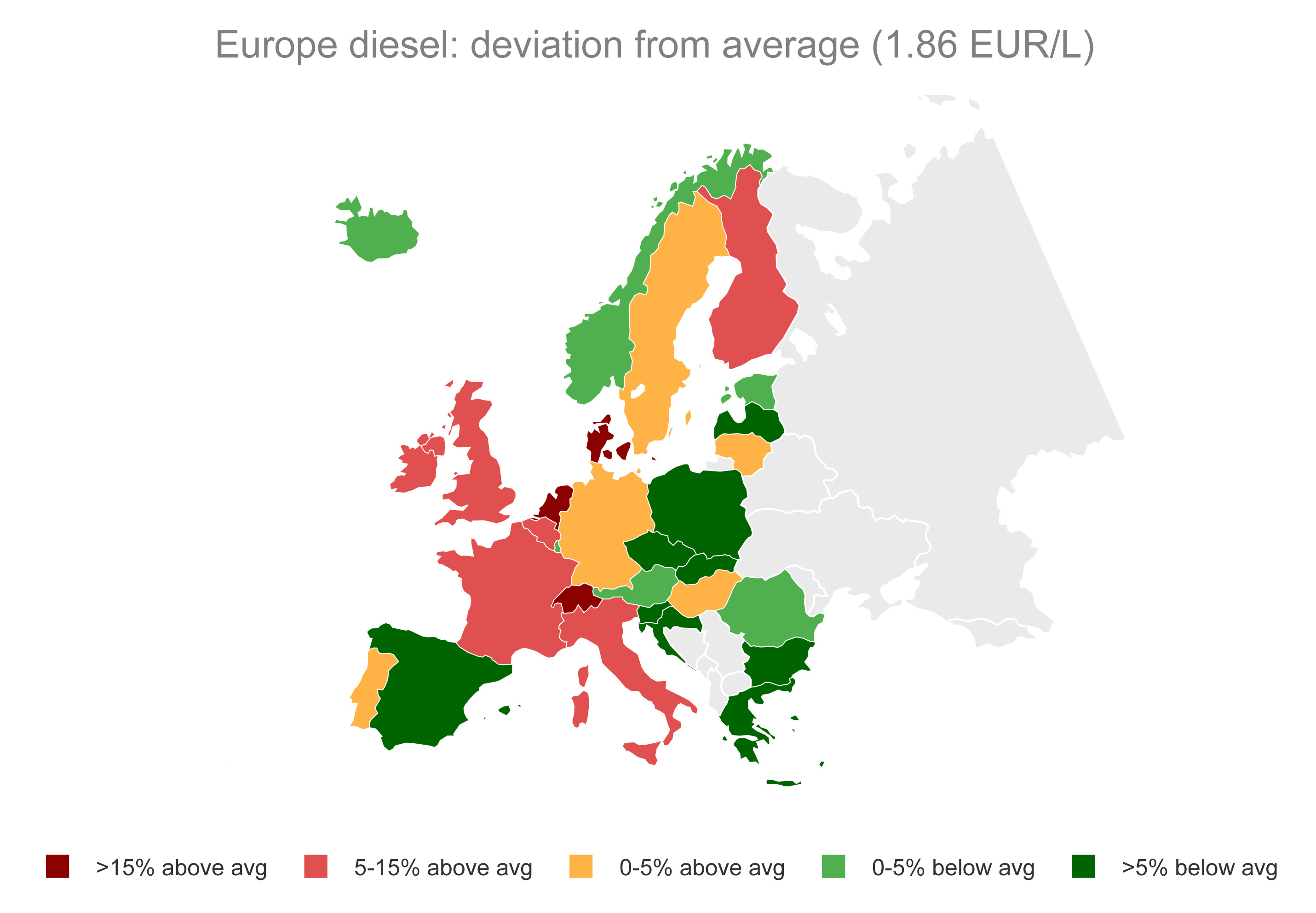

- EU average diesel price reached EUR 1.863 per litre, down 1.9% on the week – a second consecutive weekly fall

- UK diesel stands at GBP 1.82 per litre, up 29% since 27 February

- The Dutch TTF gas benchmark reached EUR 48.75 per MWh on 4 June, up 3.9% on the week and 52.5% above the 27 February baseline – the only major energy benchmark to rise while crude eased

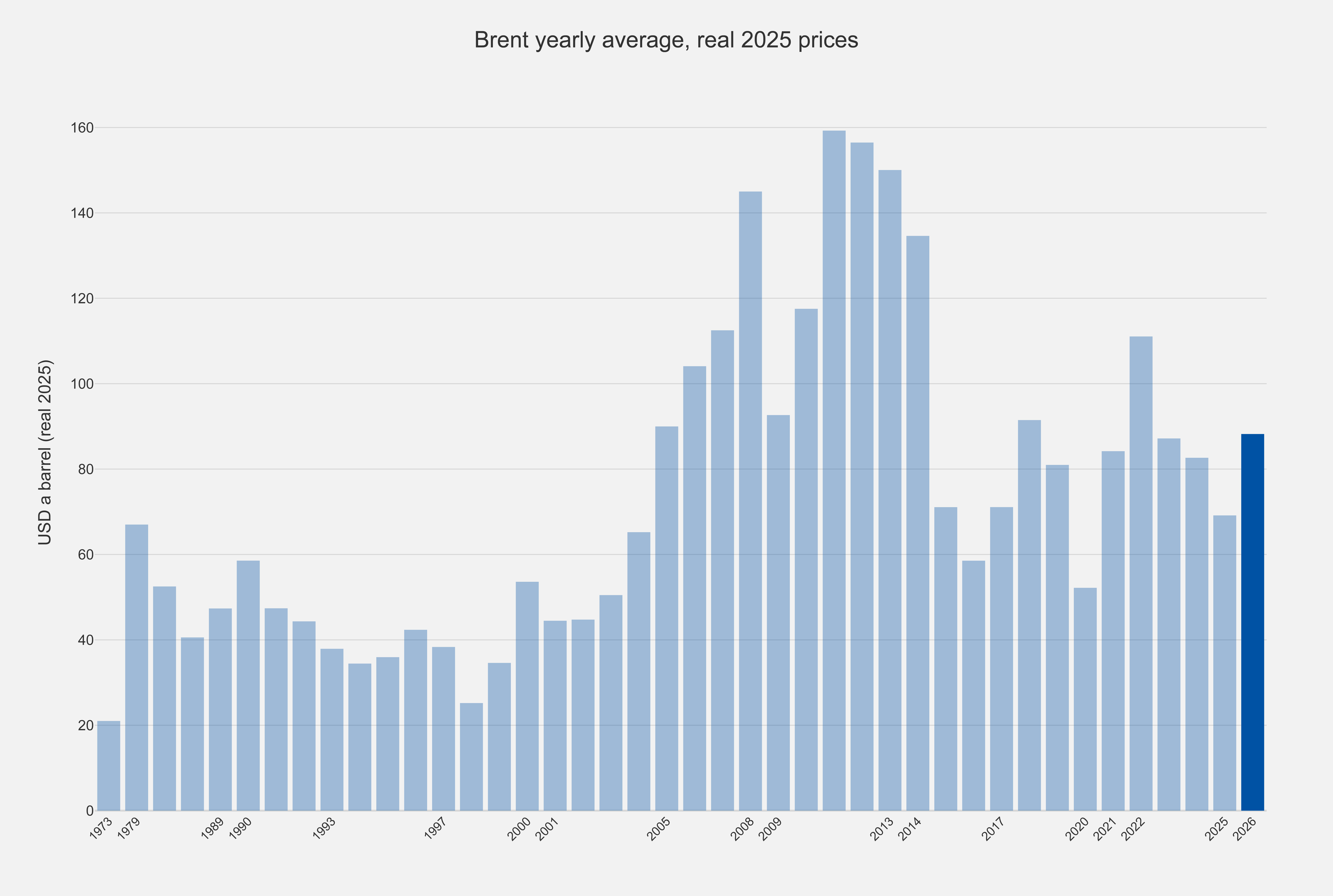

Brent is trading around USD 95 a barrel today, 31% higher than at the start of the conflict. When past Brent prices are converted into 2025 US dollar values, current levels remain below earlier peaks. This suggests that governments and industries have already managed higher energy prices in the past.

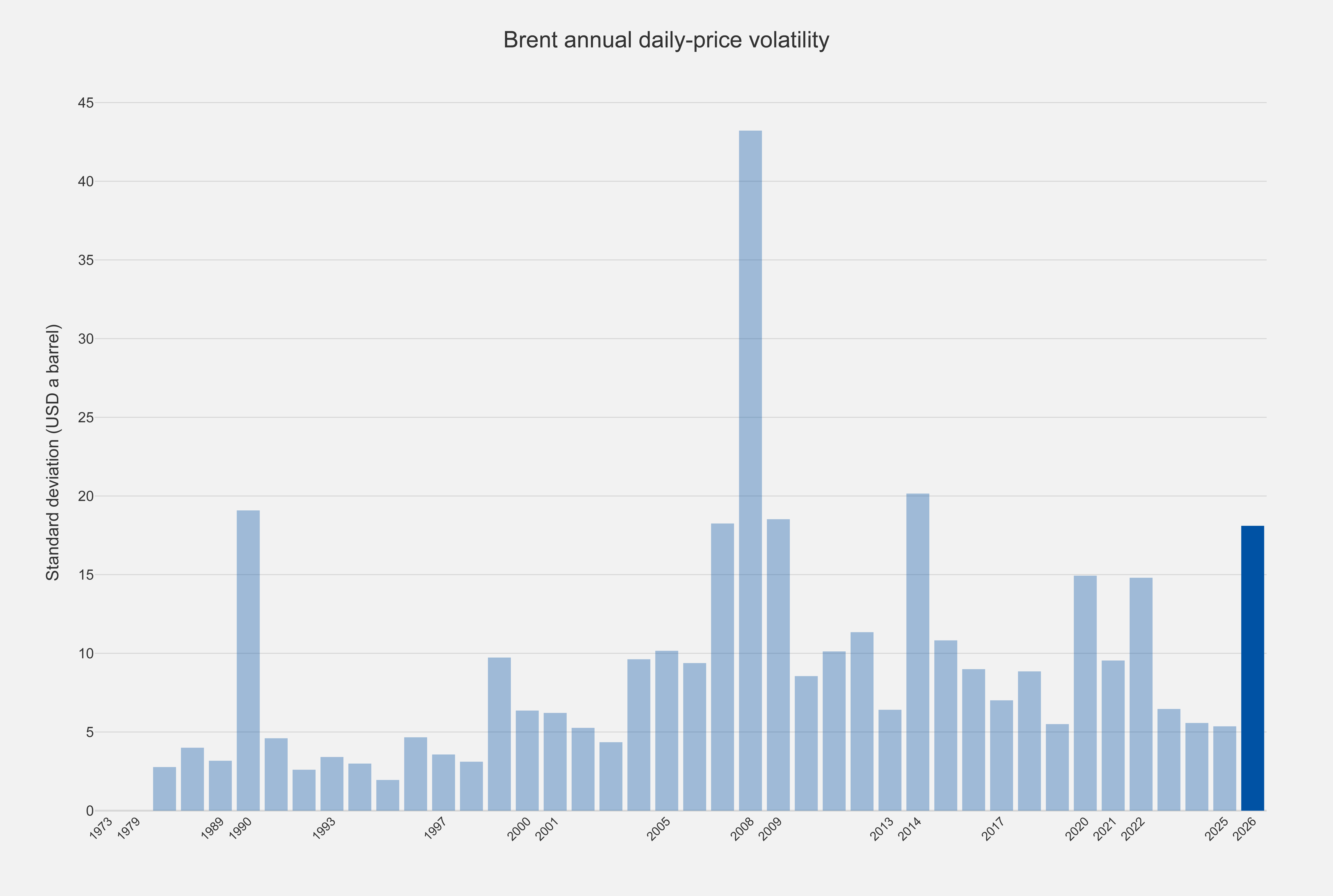

However, Brent prices have been highly volatile, which is widely seen as damaging to economies. The past week illustrates the point. Brent settled at USD 94 on 28 May, slid to an intraday low near USD 91 on 29 May – ending May down 19%, its worst month since March 2020 – then jumped back above USD 94 on 1 June. It reached almost USD 99 on 3 June, before easing to around USD 95 on 4 June.

This volatility is in crisis territory. The standard deviation of daily Brent closing prices in 2026 already stands at USD 18.1 – in the same band as the 1990 Gulf War (USD 19.1) and the 2014 supply shock (USD 20.2), higher than the 2020 pandemic and 2022 Ukraine-war years, and with only the 2008 spike (USD 43.2) clearly above it.

For road transport operators, this volatility matters more than the level itself. It is not the average price that breaks a transport business, but the gap between what is agreed in a contract and what is paid at the pump the following week. Markets currently imply a USD 92–98 range while the deal remains in the balance, a drop below USD 90 if it is signed, and a retest of USD 100 or more if the ceasefire collapses.

Two warnings argue against treating the USD 92–98 range as stability. The OECD reports that global oil stocks fell by more than 100 million barrels in both April and May, and the chief executives of Chevron and ExxonMobil told investors on 29 May that the buffers behind the spring’s relative calm (above-normal inventories, strategic releases, and redirected cargoes) are largely exhausted. With inventories “approaching unheard of” lows, they expect sharper price moves from June–July once the drawdown reaches minimum operating levels.

Both also argued that, even after a deal, prices will settle above the pre-war baseline as countries rebuild depleted reserves and the industry absorbs years of repair costs. Chevron described this as a “firmer and higher” floor, consistent with the IEA’s finding that oil majors now budget on prices above the pre-conflict baseline.

WTI, the US benchmark, reached USD 93, up 5% on the week and around 38% above baseline, while the S&P GSCI commodity index rose 2.2% to 710. Supply fundamentals remain tight: the IEA’s May report describes a market “severely undersupplied” through the end of the third quarter, and around 412 million barrels of the coordinated strategic stock release have already been mobilised – buffers that will take years to rebuild once the crisis ends.

Prices at pumps

US

US diesel reached USD 1.43 per litre, up 40.0% since 27 February – still the largest increase in the sample, but down from USD 1.47 on 22 May, the first material easing since the war began. The US remains more exposed to WTI – itself up around 38% – than the EU is to Brent, and US refiners continue to absorb a disproportionate share of Atlantic diesel demand.

EU

EU average diesel price reached EUR 1.863 per litre, down 1.9% on the week – a second consecutive weekly fall, confirmed by the European Commission’s Weekly Oil Bulletin, which recorded its first EU27 weekly decline since the crisis began (petrol –2.11%, diesel –2.62% on 1 June). The mean remains 14.0% above the 27 February baseline, and the cheapest-to-most-expensive spread narrows to EUR 0.98 per litre – still an unprecedented divergence in the single market.

The five most expensive markets are Denmark at EUR 2.189 per litre (+17.1%), the Netherlands at EUR 2.189 (+12.3%), Finland at EUR 2.080 (+18.7%), Belgium at EUR 2.060 (+20.9%) and France at EUR 2.033 (+18.9%).

At the other end, Malta’s subsidised price is unchanged at EUR 1.210, Poland stands at EUR 1.487 (+4.5%) and Czechia at EUR 1.586 (+14.7%).

Two readings stand out: Ireland, at EUR 1.998, is the first EU market back below its pre-war level (–0.3%), while Bulgaria, at EUR 1.694, now shows the steepest increase in the sample (+31.4%). Government measures are entering their exit phase.

Italy’s DL 89/2026 excise cut expires on 6 June and the government has signalled non-renewal, pivoting to a one-off EUR 100 bonus for low-income households; pumps would revert by around EUR 0.05 on petrol and EUR 0.10 on diesel, plus VAT, from 7 June.

Austria extended its Spritpreisbremse from 1 June only in weakened form – the EUR 0.025 margin cap lapsed on 31 May, leaving a EUR 0.017 cent excise cut.

Denmark has ruled out fuel-tax cuts, and Germany signals that the EUR 0.1404 per litre Tankrabatt will lapse on 30 June.

Latvia’s finance minister is publicly resisting an extension of the diesel excise cut beyond 30 June, and Lithuania’s relief expires on 15 June with extension amendments still pending in the Seimas. Relief remains in place elsewhere. Poland extended its package (8% VAT, EU-minimum excise and daily price caps) to 15 June, with caps now well below their launch level at PLN 5.94 per litre for petrol and PLN 6.40 for diesel.

Czechia’s June regulation keeps daily maximum prices and the diesel excise cut in force, with 5 June caps at CZK 41.98 and CZK 39.51 per litre.

Croatia’s new two-week cap cycle runs from 3 to 15 June at EUR 1.61 per litre for both fuels. Greece extended its EUR 0.15 per litre diesel subsidy into June, a third consecutive month. France’s TotalEnergies price cap (EUR 1.99 petrol, EUR 2.25 diesel) continues “as long as the crisis lasts”, alongside the doubled EUR 100 per month aid for heavy fuel users – operators must register by 15 June.

Hungary holds its 595/615 HUF caps to 30 June, with market prices now only 40–46 forints above the cap, and Spain’s VAT cut and EUR 0.20 per litre professional-diesel card run to 30 June. Sweden has formally tabled the bill deepening its fuel-tax cut by SEK 2.40 per litre from 1 July.

UK

UK diesel stands at GBP 1.82 per litre, up 29% since 27 February (around GBP 0.184, with petrol near GBP 0.159 on 1 June). The GBP 0.05 fuel-duty cut runs to 31 August 2026 with a phased restoration thereafter, and the reduced red-diesel rate takes effect on 15 June.

Türkiye

Diesel in Türkiye reached TRY 67.91 per litre, up 10% in local currency since 27 February.

The Eşel Mobil sliding-scale ÖTV mechanism continues to absorb roughly three-quarters of wholesale price moves, and pump prices eased over the week – benzin cut by TRY 1.38 and motorin by TRY 1.83 on 2 June, partly reversed the following day, leaving Istanbul prices near TRY 63.45 for benzin and TRY 66.30 for motorin.

China

Chinese diesel held at CNY 8.46 per litre, up 29% in local currency since the baseline. Beijing’s supply-side stance is unchanged: refined-product exports remain suspended and nitrogen-fertiliser export licensing continues to restrict urea flows – a structural squeeze on the European AdBlue chain.

India

Indian diesel held at INR 98.13 per litre, up 8% in local currency. The combination of a partial excise removal on transport-grade diesel and discounted Iranian barrels through the Chabahar corridor continues to shield Indian pumps, while refiners run near capacity and export diesel to East Africa and South-East Asia.

Brazil

Brazilian diesel reached BRL 6.89 per litre, up 14% in local currency since 27 February.

The transition between support schemes was executed on time: from 1 June, diesel sold to distributors fell from BRL 3.65 to BRL 3.30 per litre as the new BRL 0.3515 per litre subsidy replaced the expiring federal tax exemption, and a BRL 0.44 per litre gasoline subsidy offset most of Petrobras’s BRL 0.48 refinery-gate increase.

The gap to import parity remains wide – around 41% on gasoline and 31% on diesel – and importers, who supply a quarter to a third of Brazilian diesel, warn that subsidies unpaid since 12 March could break import finance from June. Punctual supply failures are reported in northern and north-eastern hubs.

Natural gas

The Dutch TTF gas benchmark reached EUR 48.75 per MWh on 4 June, up 3.9% on the week and 52.5% above the 27 February baseline – the only major energy benchmark to rise while crude eased, and now the most stretched of the liquid hydrocarbons relative to baseline.

The intra-week path tracked the same geopolitical whiplash as Brent: down to EUR 46.00 on 29 May, back up to EUR 49.09 on 1 June as the talks stalled.

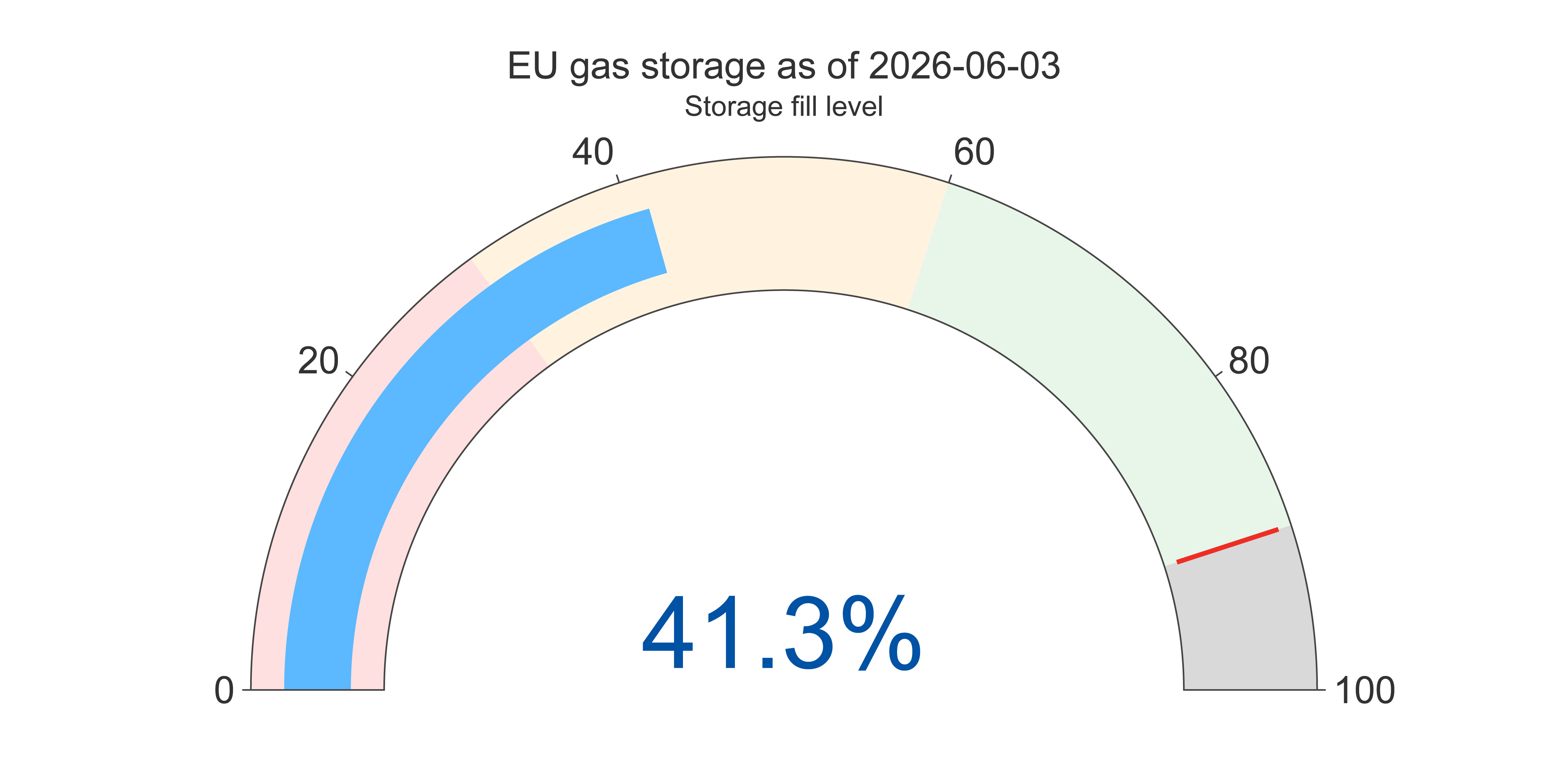

EU gas storage stands at 41.3% full (466.8 TWh, around 48 days of average demand), up from 38.8% a week earlier as the injection season progresses. The lowest-fill countries are Sweden at 9.9%, the Netherlands at 16.8%, Belgium at 21.9%, Bulgaria at 24.1% and Croatia at 32.1%.

The structural constraint is unchanged: the March strike on Qatar’s Ras Laffan complex removed 17% of Qatari export capacity for up to five years, leaving the bloc to inject through the summer with the smallest LNG cushion in years.

Road transport impact

For European road transport operators, the second consecutive weekly fall in diesel is welcome, but the centre of gravity of risk is shifting from the market to the policy calendar.

If announced messages expire as planned, pump prices will increase by around EUR 0.10 per litre on diesel in Italy from 7 June (plus VAT), and by EUR 0.14–0.20 per litre in Germany, Spain and Australia on 1 July – independent of anything Brent does. The 15 June cluster (Poland, Lithuania, North Macedonia, Croatia) will reveal how governments behave once prices ease: Latvia’s and Lithuania’s finance ministries are already arguing that falling prices no longer justify relief. The cost squeeze remains structural.

In the European E6 freight market, comprising Europe’s six biggest markets, contract rates have moved up around 3% and spot rates around 6% since the war began, while the total cost of operating a truck has risen much further – operators are absorbing the difference. This is where the volatility analysis above becomes operational: with Brent swinging USD 8 within a single week, fuel clauses negotiated quarterly cannot keep pace, and the gap between contracted rates and pump reality widens.

At EU level, operators have an instrument many have not yet used: the Middle East Crisis Temporary State Aid Framework (METSAF), adopted on 29 April, lets EU countries compensate road transport operators for up to 70% of additional fuel costs, or up to EUR 50,000 per beneficiary through a simplified route, until 31 December 2026 – with road transport explicitly included.

But METSAF is permission, not money: support depends entirely on national scheme design, and asymmetric implementation risks distorting the single market for cross-border hauliers. With the OECD now projecting inflation effects through 2027 even in its optimistic scenario, the framework’s 31 December 2026 expiry already looks short.

The demand side of the squeeze is also hardening. The OECD’s June outlook cuts global growth to 2.8% in 2026 (from 3.4% in 2025) and nearly halves eurozone growth to 0.8%, with G20 inflation at 4.0% this year and still 3.1% in 2027; Wood Mackenzie estimates the world slips into a shallow recession in the second half without a near-immediate reopening of the Strait.

The IMF’s framing is a warning to anyone relying on price hedges alone: “It’s not just a price shock, it’s explicit shortages.” In north-west Europe the physical signs are already visible – Middle East diesel deliveries collapsed from 1.59 million tonnes in March to 0.36 in April and just 0.1 in early May, EU and UK diesel arrivals are at a ten-year low, and ARA gasoil stocks are down 12% year on year.

AdBlue remains the silent watch item: more than a third of the world’s urea feedstock comes from the Middle East, and a urea interruption is a capacity problem, not a price problem – Euro VI trucks cannot legally run without it.

Outlook: what to watch

6 June 2026 – Italy’s taglio accise expires; decision on the replacement package and Unatras’s reaction; watch a weekend forecourt rush.

7 June 2026 – Serbia’s reduced excise rates expire, with a government decision imminent. Also the weekend window flagged by President Trump for Iran–US progress: markets price a USD 92–98 band while the deal hangs, below USD 90 on a signature, above USD 100 if the ceasefire collapses.

10 June 2026 – EC Weekly Oil Bulletin; will confirm whether the EU pump decline extends to a third week.

12 June 2026 – IEA June Oil Market Report; watch the October rebalancing call and second-half refinery throughput.

15 June 2026 – Five measures land at once: Poland’s cap package, Lithuania’s and North Macedonia’s excise reliefs and Croatia’s cap cycle expire, and the UK red-diesel change takes effect; also the French hauliers’ registration deadline for the doubled fuel aid.

30 June 2026 – The triple cliff: Germany’s Tankrabatt, Spain’s VAT cut and professional-diesel card and Australia’s excise cut all expire, alongside measures in Hungary, Czechia, Austria, Portugal, Romania, Bulgaria, Cyprus, Greece, Latvia and Serbia. Without extensions, EU pumps step up by EUR 0.14–0.20 per litre on 1 July even with crude unchanged.

1 July 2026 – Argentina’s full accumulated fuel-tax adjustment lands; the Netherlands zeroes truck road tax.

31 August 2026 – UK GBP 0.05 fuel-duty cut expires, with phased restoration through March 2027. 7 September 2026 – Canada’s federal fuel-excise suspension ends.

In the meantime, the road transport sector is asked to absorb a 14% EU and 40% US diesel cost shock with single-digit rate pass-through, a fragmenting fiscal safety net and crisis-grade price volatility.

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.

IRU members, strategic partners an Intelligence subscribers already have full access to the IRU fuel prices service.