As of 13 March 2026, global oil and fuel prices continue to rise. Here is the latest overview for the road transport sector.

Limited maritime movements around the Strait of Hormuz and the war in Iran are now impacting crude oil sites and refineries across the Middle East. The price of crude is on the rise, resulting in large increases at pumps globally.

This short, weekly analysis first looks at average prices at the pump, before turning to wholesale energy dynamics, including Brent and LNG trends.

Prices at the pumps

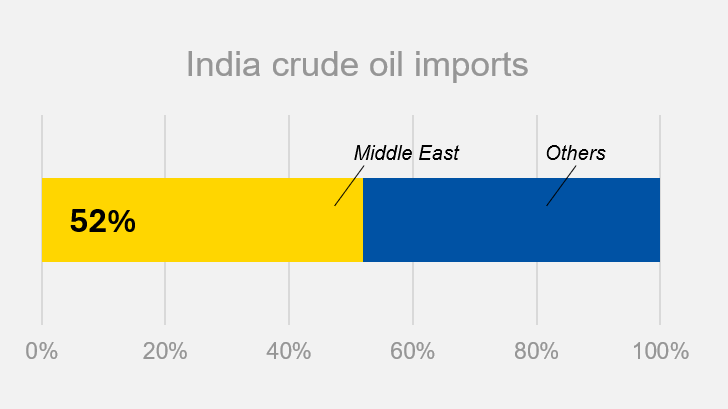

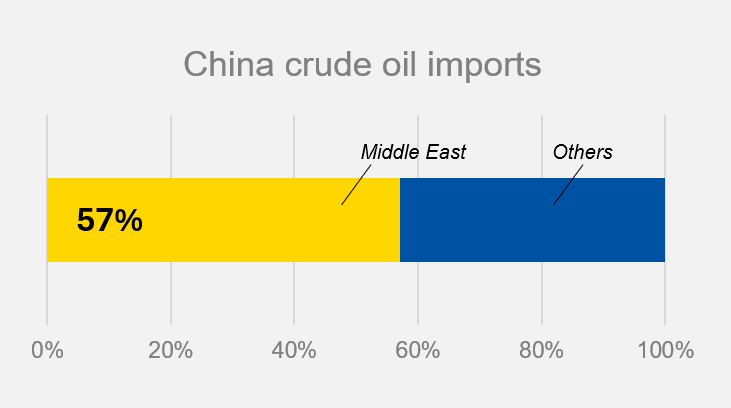

China and India rely the most on crude oil from the Middle East. But as the crude oil market is global, diesel prices are increasing everywhere, including in the US and EU.

The US has experienced the largest increase, with diesel prices rising by 25% since the beginning of the war. The WTI, used as reference for the region, is now aligned with Brent. It is normally much lower.

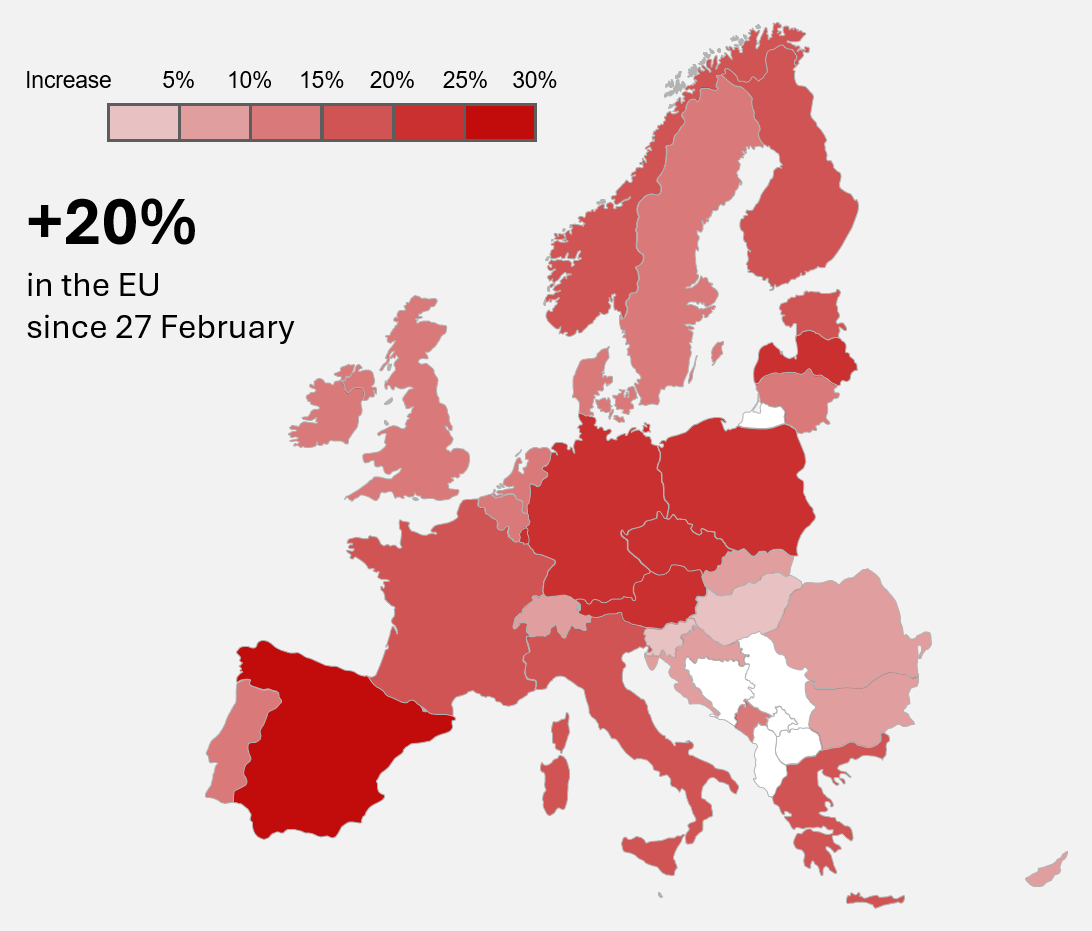

The EU is also seeing a significant price hike. The weighted average (based on trucks’ consumption) has surged by 20%. Diesel is now reaching EUR 2 per litre on average (taxes included). In the UK, diesel prices have risen by 13% at the pump.

The trend at European pumps since 27 February 2026 has been upwards, with the largest increase observed in Spain (27%, reaching EUR 1.79 per litre) and the highest price found in Ireland (EUR 2.3 per litre). Diesel has also exceeded EUR 2 per litre in Germany, Finland, France, Italy, and the Netherlands.

Early fuel price trends in Europe

Source: https://www.iru.org/intelligence/fuel-prices

In China, fuel prices are partly controlled by the government. This has limited the increase to 11% between the start of the war and 12 March. The same goes for India, with prices of diesel increasing by just 5%.

The EU, US and UK should be protected from any diesel shortages in the medium term, as they are less dependent on Middle East crude oil. However, China and India are more exposed.

China is actively trying to limit domestic pump price spikes:

- Authorities have asked major refineries to suspend diesel and gasoline exports to keep more fuel for the domestic market

- The government adjusts retail fuel prices in China based on international crude movements, rather than purely market pricing

This means that price increases at the pump happen gradually, rather than continuously like in Europe.

In China, fuel prices are partly controlled by the government, which limited the increase to 11% between the 12th of March and the start of the war. India is in the same case, with prices of diesel increasing by just 5%.

The EU, US and UK should be protected from any diesel shortages in the medium term, as they are less dependent on Middle East crude oil. However, China and India are more exposed. The situation needs to monitored closely in the coming weeks.

Brent price dynamics

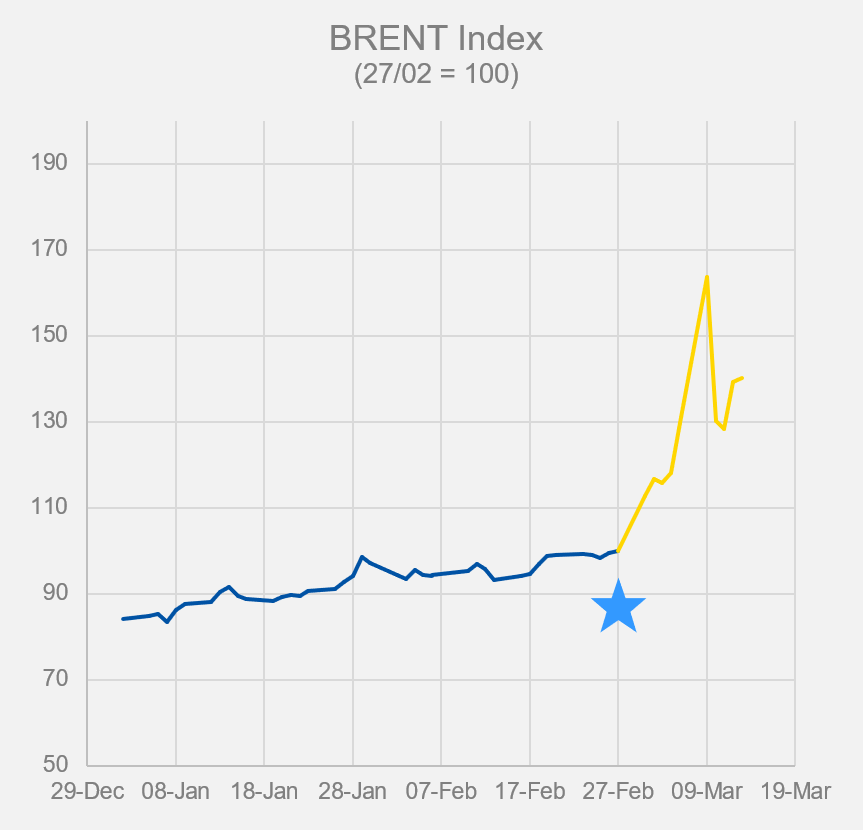

The conflict in the Middle East has pushed Brent from roughly USD 73 a barrel on 27 February to USD 120 on 9 March, a 65% increase.

Brent has been highly volatile this week. However, with attacks on refineries and storage facilities, and reduced output at some production sites, Brent is still close to USD 100, despite IEA members releasing 400 million barrels from stockpiles worldwide (over the 1,800 million barrels available). Analysts suggest this release could offset around 20 days of a Strait of Hormuz blockade. However, accessing and distributing this buffer is challenging.

Even if the war ends relatively soon, a return to normalcy will take weeks, and questions remain about sites that have reduced output, as shutting down and restarting can jeopardise efficiency.

Markets are pricing in the risk of supply disruptions in the Middle East, particularly through the Strait of Hormuz. The next move in oil prices will depend almost entirely on whether shipping through that corridor normalises or worsens. The US plans to secure the Strait of Hormuz to normalise maritime movements, but said it could take weeks for full implementation.

Some countries have already taken steps to lower fuel consumption and mitigate cost increases.

In Pakistan, schools are closed and government offices operate four days a week. South Korea has announced that it would cap pump prices for the first time in nearly 30 years. In France, IRU member TotalEnergies said on Thursday that it would cap gas and diesel prices until the end of the month.

European Commission President Ursula von der Leyen said on Wednesday that the Commission is “exploring subsidies or capping the gas price” and urged countries to lower electricity taxes.

The risk of inflation will increase if the war goes on for several months and Brent exceeds USD 150, putting the world in a situation close to the 1973 oil crisis, according to Economic Nobel Prize Winner Philippe Aghion.

As of 13 March 2026, Brent has risen by 13% since the war began, hitting USD 100 a barrel. If the situation does not move towards a resolution, Brent could reach USD 120 a barrel in the coming weeks.

Why Brent is rising

- Strait of Hormuz disruption

- Around 20% of global oil supply normally passes through this route

- Tanker attacks and shipping suspensions have stranded hundreds of vessels - Supply risks

- Potential loss of 20 million barrels a day from GCC exporters - Energy infrastructure

- Strikes on oil facilities and tankers have amplified market risks

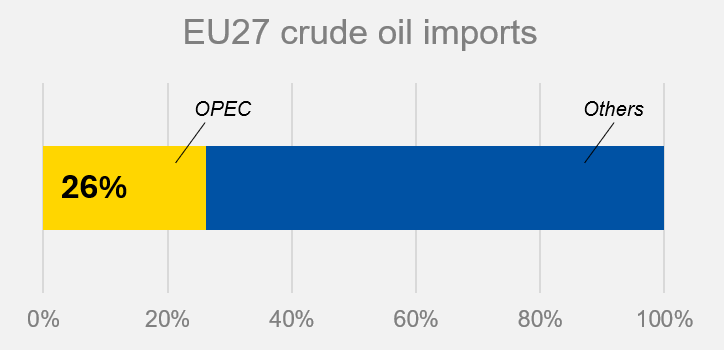

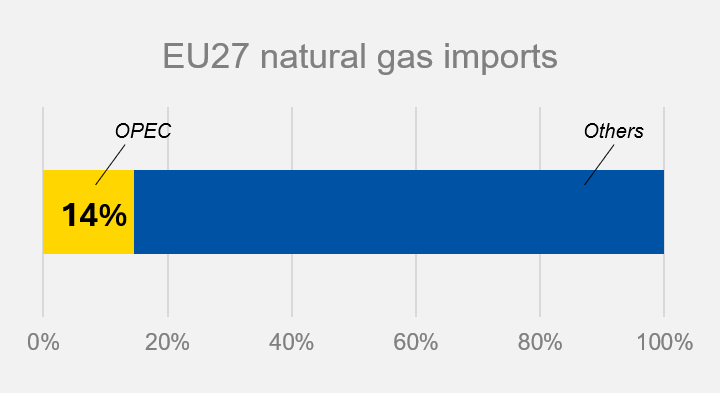

OPEC countries supply 26% of the crude oil consumed in the EU and 15% of its road diesel. Due to limitations along the Strait of Hormuz, most OPEC production cannot be exported, significantly affecting Asian countries and, to a lesser extent, the EU.

China is increasingly exposed to crude oil supply disruptions, as most of its imports come from the Middle East.

According to Bloomberg, officials from the National Development and Reform Commission have verbally urged refiners to temporarily suspend shipments of refined products with immediate effect.

Natural gas price dynamics

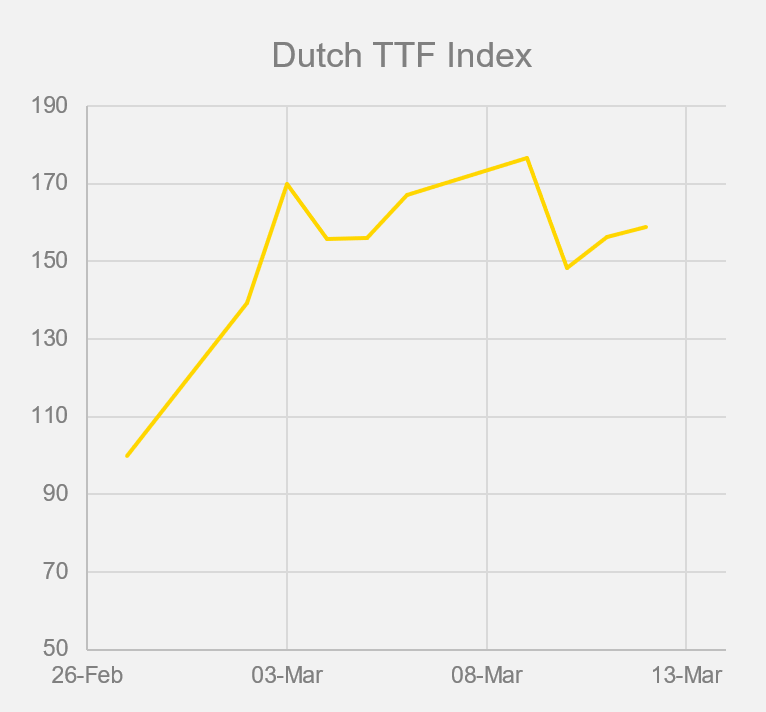

Dutch TTF Gas prices, Europe’s benchmark gas hub, have been strongly affected, mainly through LNG supply risk, shipping chokepoints, and storage dynamics. Below are the key market dynamics shaping Dutch TTF Gas prices.

Since 27 February, prices have increased by 57%, closing at EUR 50 per MWh.

LNG supply

- Around 20% of global LNG trade passes through the Strait of Hormuz

- Disruptions affecting Qatar’s LNG facilities and shipping routes have tightened global gas markets

- Qatar accounts for a major share of global LNG supply. Outages immediately reduce available cargoes

Qatar LNG disruption

A critical recent factor: QatarEnergy’s LNG facilities have halted production, which normally account for around 20% of global LNG output.

Implications for Europe

Qatar supplies a smaller share than the US but is still significant (around 8% of EU imports). OPEC countries, primarily Qatar, supply 14% of natural gas consumed in the EU.

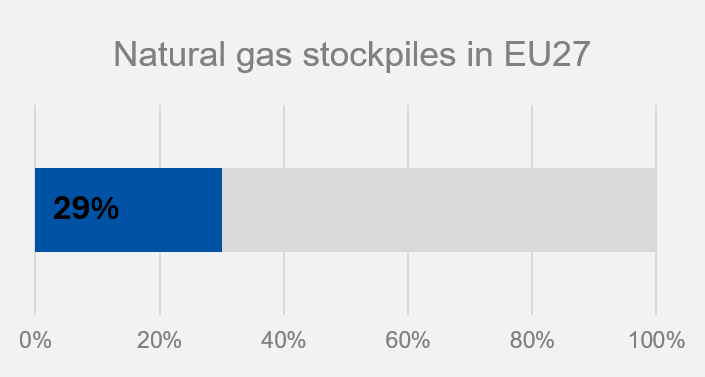

Stockpiles are lower than usual in the EU, averaging 29%, with the Netherlands falling below 10% this week and Germany climbing by 2 percentage points to 22%.

Stockpiles will need to be replenished at potentially higher prices, which could impact economic output and freight activity, as manufacturing will become more expensive in the EU.

If the situation does not move towards a resolution, Dutch TTF Gas can potentially rise to EUR 60 per MWh.

Brent price dynamics - summary

- Pre-conflict: around USD 70 per barrel

- Now (13 March 2026): around USD 100 per barrel

Gas price dynamics - summary

- Increase: Around 15–20% spike driven by supply risks and Hormuz disruptions Dutch TTF Gas

- Pre-conflict: Around EUR 30–32 per MWh

- Now (13 March 2026): EUR 50 per MWh

- Increase: Around 50–60% spike driven by LNG supply risk, potential Strait of Hormuz disruptions, and Qatar LNG outages, combined with low European storage levels and stronger competition with Asia for LNG cargoes

IRU fuel prices: Get daily updates for EU countries and weekly updates for 40+ countries, with a one-week forecast to help you plan confidently.